The late afternoon squeeze in the final minutes of trading on Thursday continues this morning with equity markets up slightly. The big news this morning will be the employment report due out at 8:30 am ET. Given the long weekend, and the likelihood of low volume, we suspect trading in the first hour or two will set the tone for the day. Good luck and have a great Labor Day.

Click HERE to receive our daily market commentary in your email every morning.

What You Need To Know

Economy

- 8:30 a.m. ET: Change in non-farm payrolls, August (725,000 expected, 943,000 in July)

- 8:30 a.m. ET: Unemployment rate, August (5.2% expected, 5.4% in July)

- 8:30 a.m. ET: Average hourly earnings, month-over-month, August (0.3% expected, 0.4% in July)

- 8:30 a.m. ET: Average hourly earnings, year-over-year, August (3.9% expected, 4.0% in July)

- 9:45 a.m. ET: Markit U.S. services PMI, August final (55.2 expected, 55.2 in prior print)

- 9:45 a.m. ET: Markit U.S. composite PMI, August final (55.4 in prior print)

- 10:00 a.m. ET: ISM Services Index, August (61.7 expected, 64.1 in July)

Earnings

- No notable reports scheduled for release

Politics

- President Biden will speak at 10 a.m. ET about the August jobs report. He often uses these speeches to sell his overall economic agenda, including the proposed $3.5 trillion Build Back Better Act currently being developed in Congress. In the afternoon, Biden is also scheduled to tour Louisiana to see damage from Hurricane Ida. In a speech at the White House yesterday, he said extreme storms made worse by climate change are “one of the great challenges of our time.”

- On Capitol Hill, both chambers are largely quiet today with only pro forma sessions planned. But senior lawmakers could be working furiously behind the scenes following an op-ed by Sen. Joe Manchin declaring Congress needs a “strategic pause” on some of Biden’s more expensive ideas.

High Bar For Employment Report

Just as you are receiving this commentary the BLS will be releasing its latest report on employment. Consensus estimates call for non-farm payroll growth of 725,000 during the month, with the unemployment rate expected to drop to a pandemic-era low of 5.2%.

The focus on Friday is on what this data will (or will not) mean for Federal Reserve monetary policy. And the question Friday’s report asks is simple: will this push the Fed to begin tapering its asset purchases?

The importance of this morning’s data in whether “substantial further progress” has been made on the labor market. As Fed Chair Jerome Powell has said he would need to see this bar met to feel comfortable slowing the central bank’s current pace of asset purchases.

But while Powell has been clear about being patient on changing policy stance, there may be a bigger factor at play.

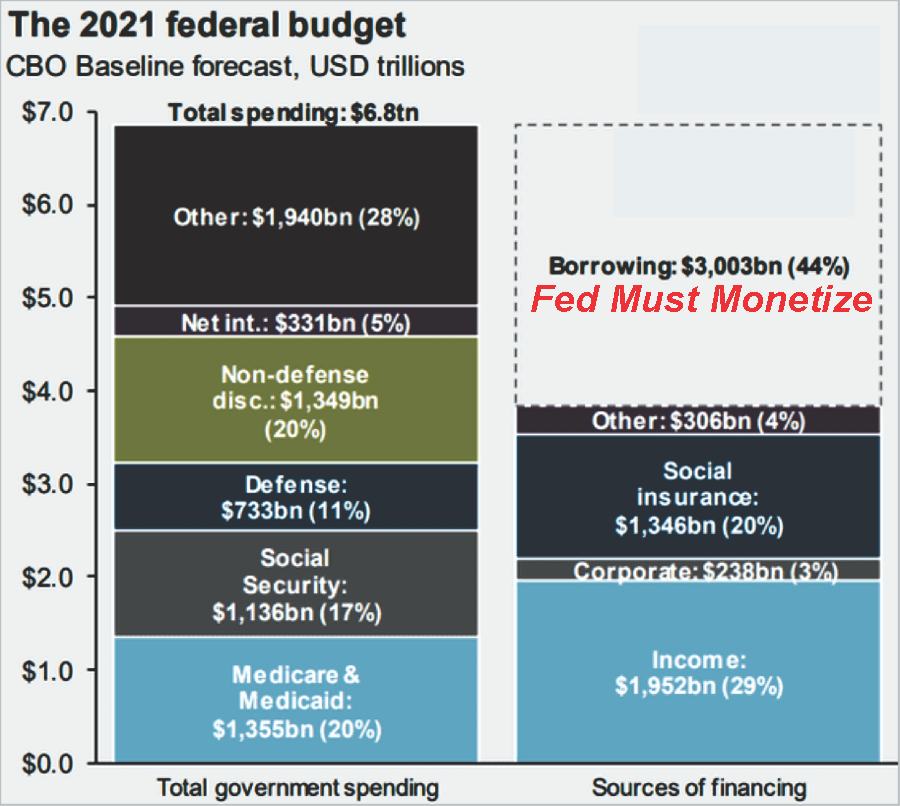

Who Is Going To Fund The Deficit

Mike and I discussed at length on Thursday that the current mandatory spending of the Government consumes more than 100% of current tax revenues. Therefore, all discretionary spending plus additional programs such as “infrastructure” and “human infrastructure” comes from debt issuance.

As shown, the 2021 budget will push the current deficit towards $4-Trillion requiring the Federal Reserve to monetize at least $1 Trillion of that issuance per our previous analysis.

The scale and scope of government spending expansion in the last year are unprecedented. Because Uncle Sam doesn’t have the money, lots of it went on the government’s credit card. The deficit and debt skyrocketed. But this is only the beginning. The Biden administration recently proposed a $6 trillion budget for fiscal 2022, two-thirds of which would be borrowed.” – Reason

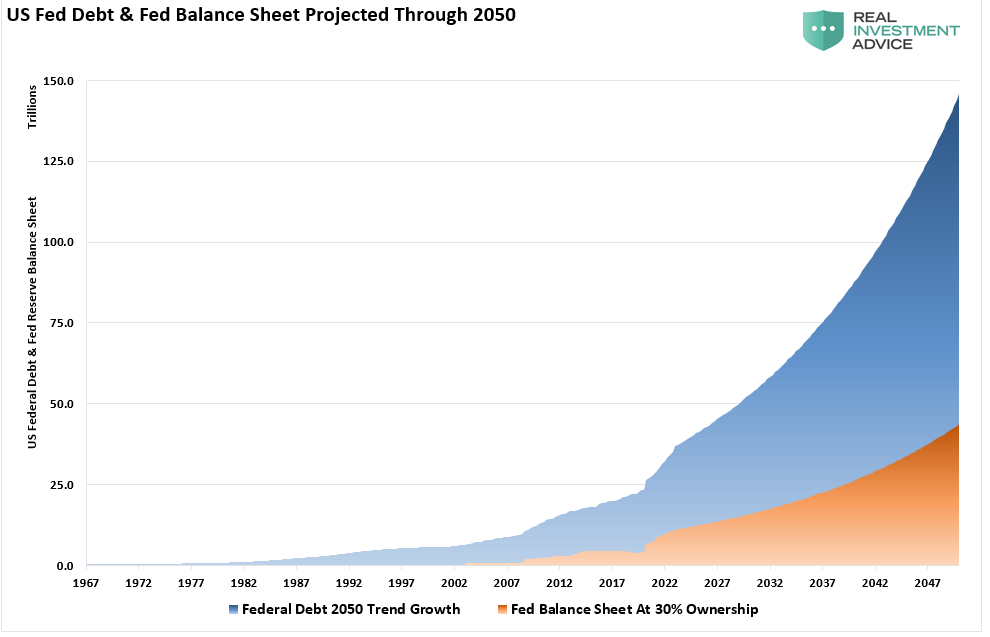

The CBO (Congressional Budget Office) recently produced its long-term debt projection through 2050, ensuring poor economic returns. I reconstructed a chart from Deutsche Bank showing the US Federal Debt and Federal Reserve balance sheet. The chart uses the CBO projections through 2050.

At the current growth rate, the Federal debt load will climb from $28 trillion to roughly $140 trillion by 2050.

The problem, of course, is that the Fed must continue monetizing 30% of debt issuance to keep interest rates from surging and wrecking the economy.

Let than sink in for a minute.

GDP Guesstimates Falling Rapidly

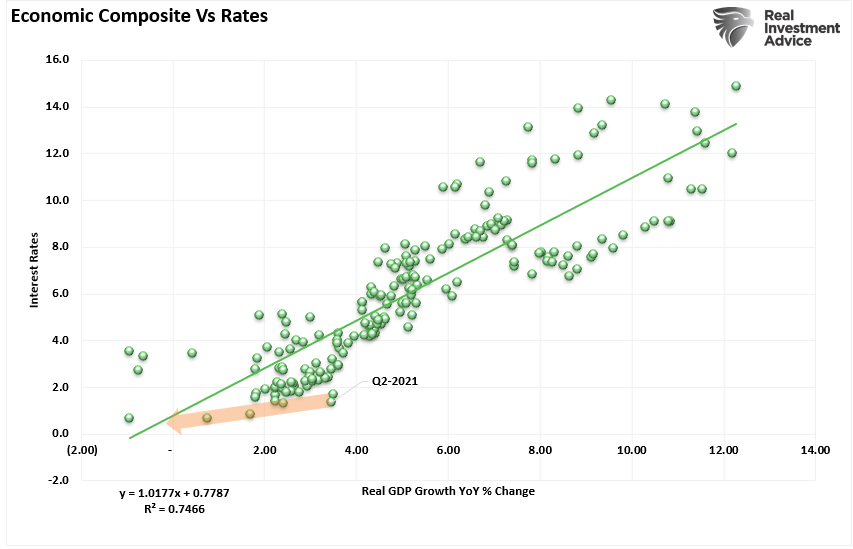

Since the beginning of this year, we have penned several articles stating that economic growth, when fueled by artificial stimulus, would ultimately disappoint. Specifically, we noted that “bonds were sending an economic warning.” To wit:

“As shown, the correlation between rates and the economic composite suggests that current expectations of sustained economic expansion and rising inflation are overly optimistic. At current rates, economic growth will likely very quickly rturn to sub-2% growth by 2022.”

The disappointment of economic growth is also a function of the surging debt and deficit levels, which as noted above, will have to be entirely funded by the Federal Reserve.

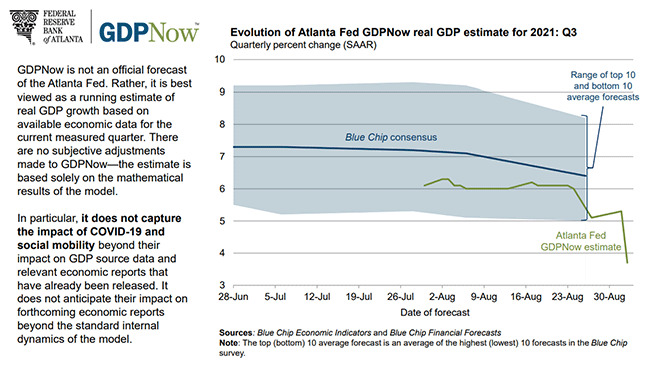

Well, on Thursday, the Atlanta Fed downgraded their estimate of third-quarter economic growth for the second time in a week. To blame were Factory Orders coming in at +0.4% versus +1.5% last month and a change in real net exports. As shown below, their estimate is now at 3.7%, down from over 6% about a week ago. The consensus remains at 6.5%.

It appears Morgan Stanley is in agreement with the Atlanta Fed. Per Zero Hedge: But if Goldman was a surprise, what Morgan Stanley did this morning – when the bank slashed its Q3 GDP from 6.5% to just 2.9% – was shocking.

Stocks On The Move

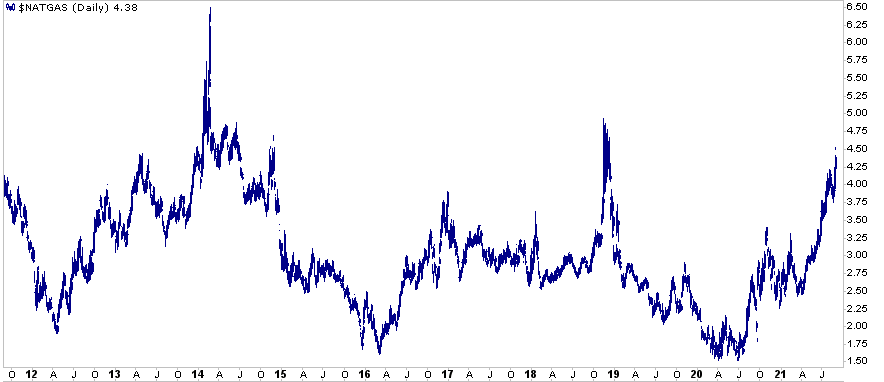

Natural Gas In Deficit

Commodity investors Goehring & Rozencwajg share their research on natural gas. Per North American Gas Markets Now in Deficit:

- “Tightness in the US natural gas market is beginning to manifest itself in low inventory levels. After having started the year at a 200 bcf surplus to the five-year seasonal average, US inventories now stand at nearly a 200 bcf deficit. Given the current trajectory, our models suggest we could end the injection season at 3.2 tcf of gas representing a 400 bcf deficit, or 700 bn cubic feet lower than the same time last year. If we are correct, inventories run the risk of starting the withdrawal season at the second-lowest level in fifteen years. At that point, any bout of cold weather this coming winter would likely lead to a price spike.”

As shown below, the price of Natural gas is up significantly in recent months. Assuming the deficit of gas persists, a colder winter might briefly push its price to the highs of 2019, 2014, or possibly higher. It’s worth noting the price of natural gas doesn’t always rise in the winter. Of the 10 years shown, over half saw stable or falling prices during the winter months.

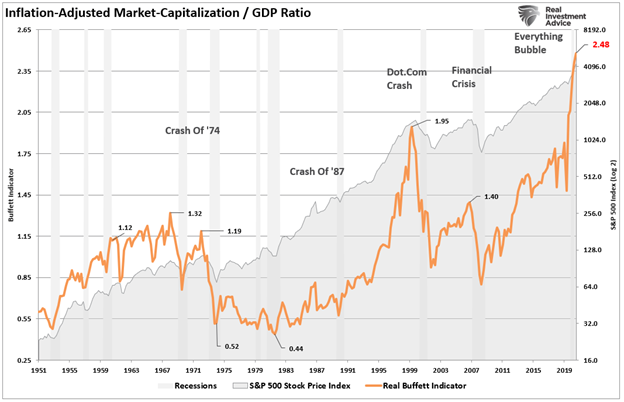

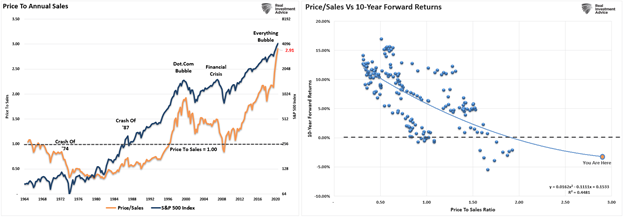

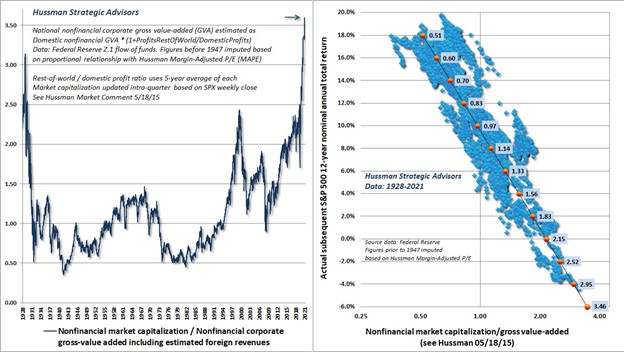

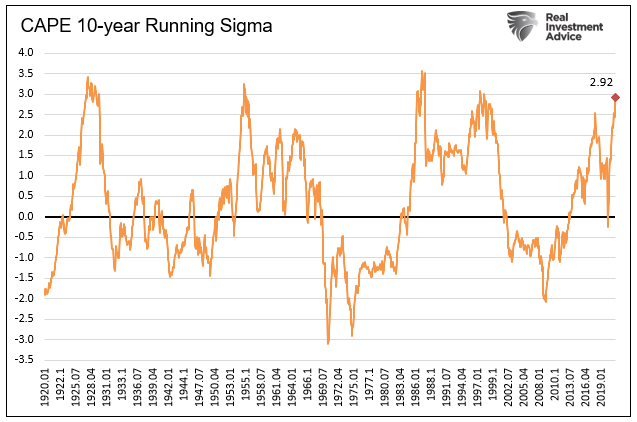

Valuation Re-examined

In Valuations Are Extreme Even With Rose Tinted Glasses, we take a new approach to calculating stock valuations. We forget history and assume “this time is different” has merit. Accordingly, we throw out scary graphs like the first three below which compare current valuations to past periods. Instead, we only compare valuations to valuations in the same ten-year period. The math is different, but the overvaluation story is not. The last graph shows that even with rose-tinted comparisons this time is not different. Valuations are extreme no matter your logic.

Also Read