- Market Believes It Has Immunity To Risk

- MacroView: Debt, Deficits & The Path To MMT

- Financial Planning Corner: Why Dave Ramsey Is Wrong About Life Insurance

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Catch Up On What You Missed Last Week

Market Believes It Has Immunity To Risks

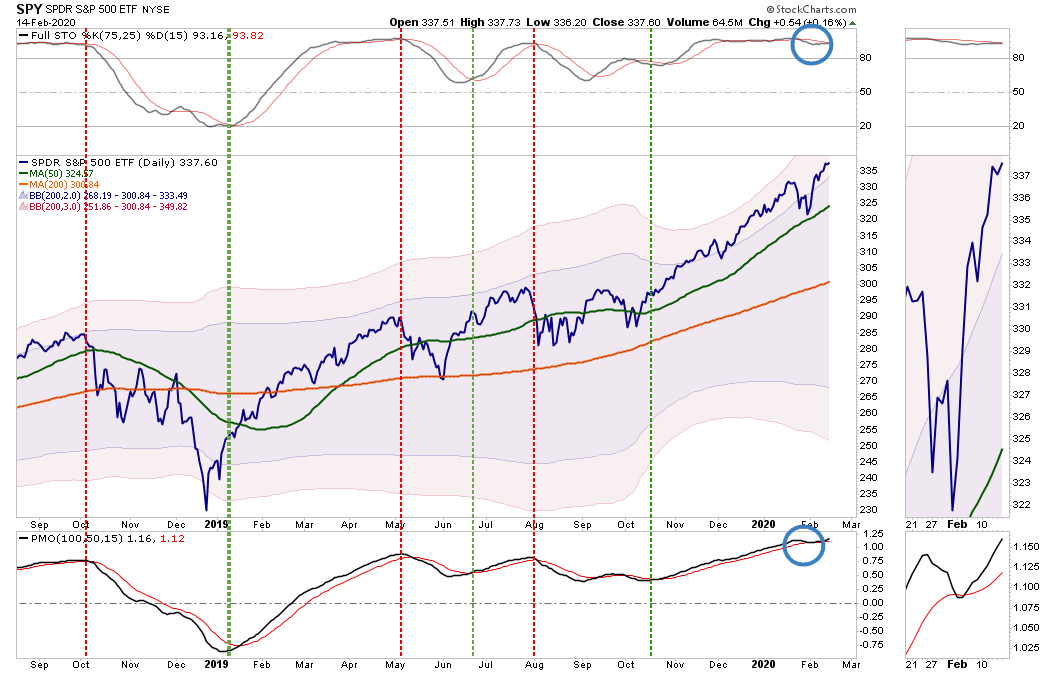

As noted last week, the spread of the coronavirus has had little impact on the markets so far.

“”The market bounced firmly off the 50-dma and rallied back to new highs on Thursday. While Friday saw a bit of retracement, which isn’t surprising given the torrid move early in the week, the ‘virus correction’ was recovered. Importantly, sharp early-week rally kept ‘sell’ signal from triggering,“

Chart Updated Through Friday

In review, we previously took some profits out of portfolios as we were expecting between a 3-5% correction to allow for a better entry point to add equity exposure. While the “virus correction” did encompass a correction of 3%, it was too shallow to reverse the rather extreme extension of the market.

The continued rally this past week has fully reversed the corrective process and returned the markets to 3-standard deviations above the 200-dma. Furthermore, all daily, weekly, and monthly conditions have returned to more extreme overbought levels as well.

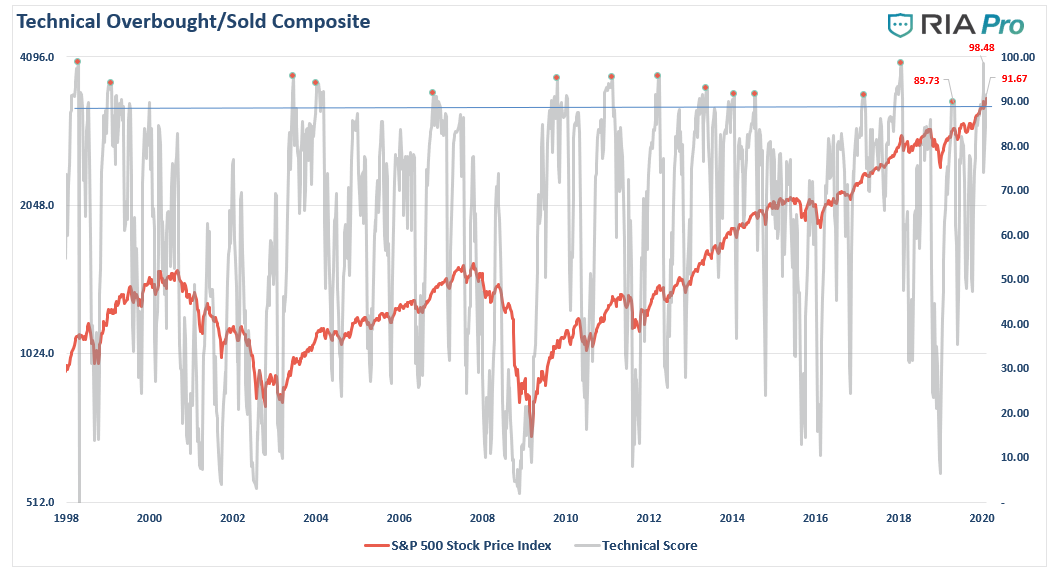

This was a point we discussed with our RIAPRO subscribers (Try for 30-days RISK FREE) in Thursday’s technical market update. To wit:

- On a weekly basis, the market backdrop remains bullish with a weekly buy signal still intact.

- However, that buy signal is extremely extended and has started to reverse with the market extremely overbought on a weekly basis.

- This is an ideal setup for a bigger correction so some caution is advised.

- With the market trading above 2-standard deviations, and testing the third, of the intermediate term moving average, some caution is suggested in adding additional exposure. A correction is likely over the next month which will provide a better opportunity. Remain patient for now.

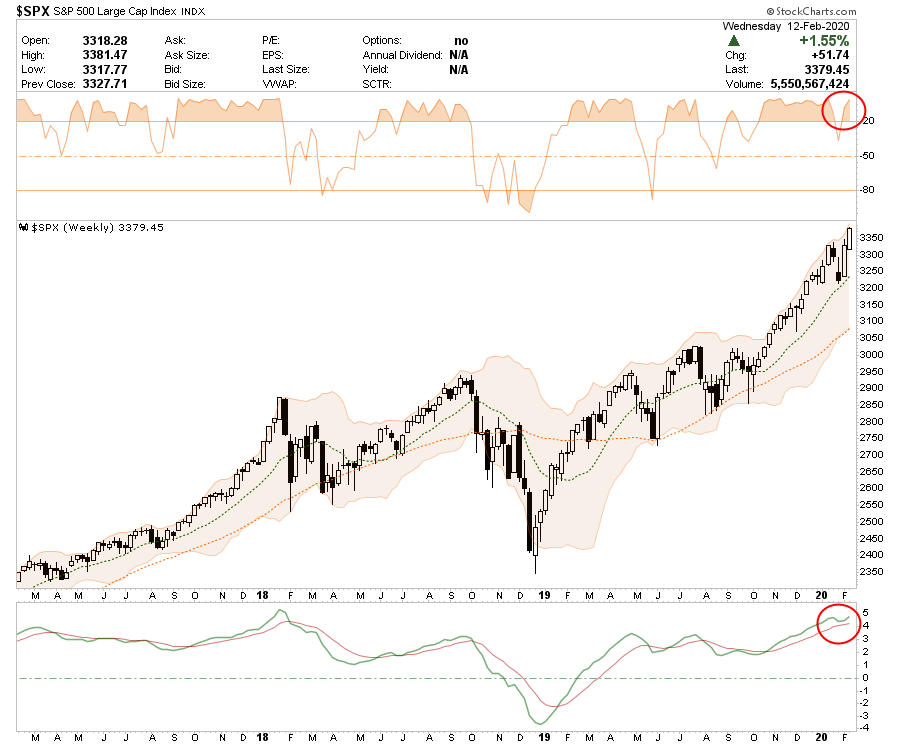

It is here that investors tend to go astray.

In the short-term, the market dynamics are indeed bullish which suggests that investors remain invested at the current time.

However, on a long-term basis, the picture becomes much more concerning.

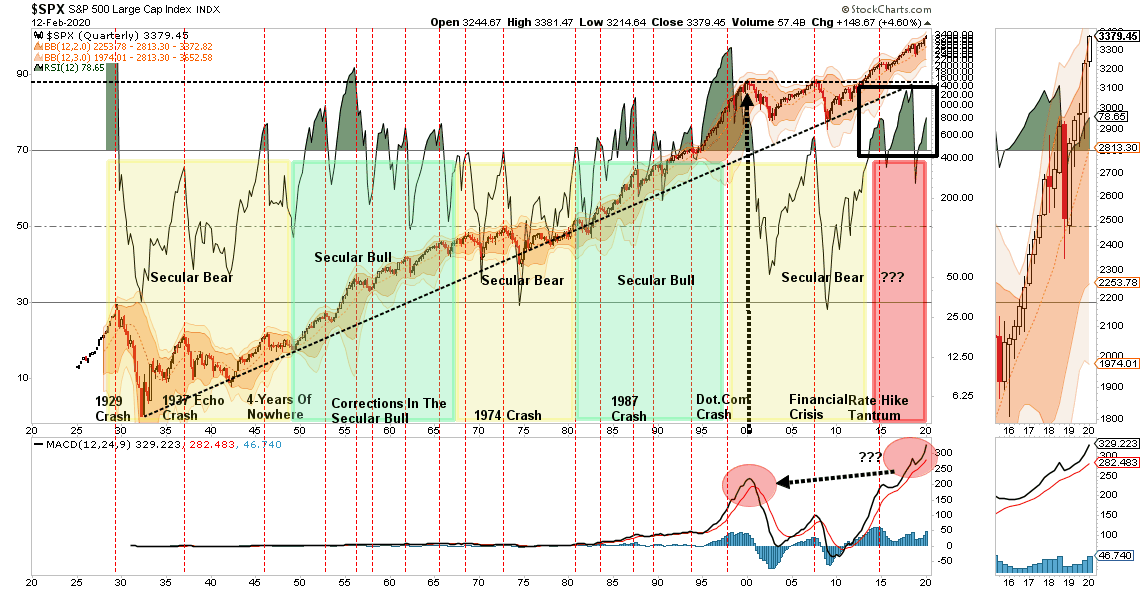

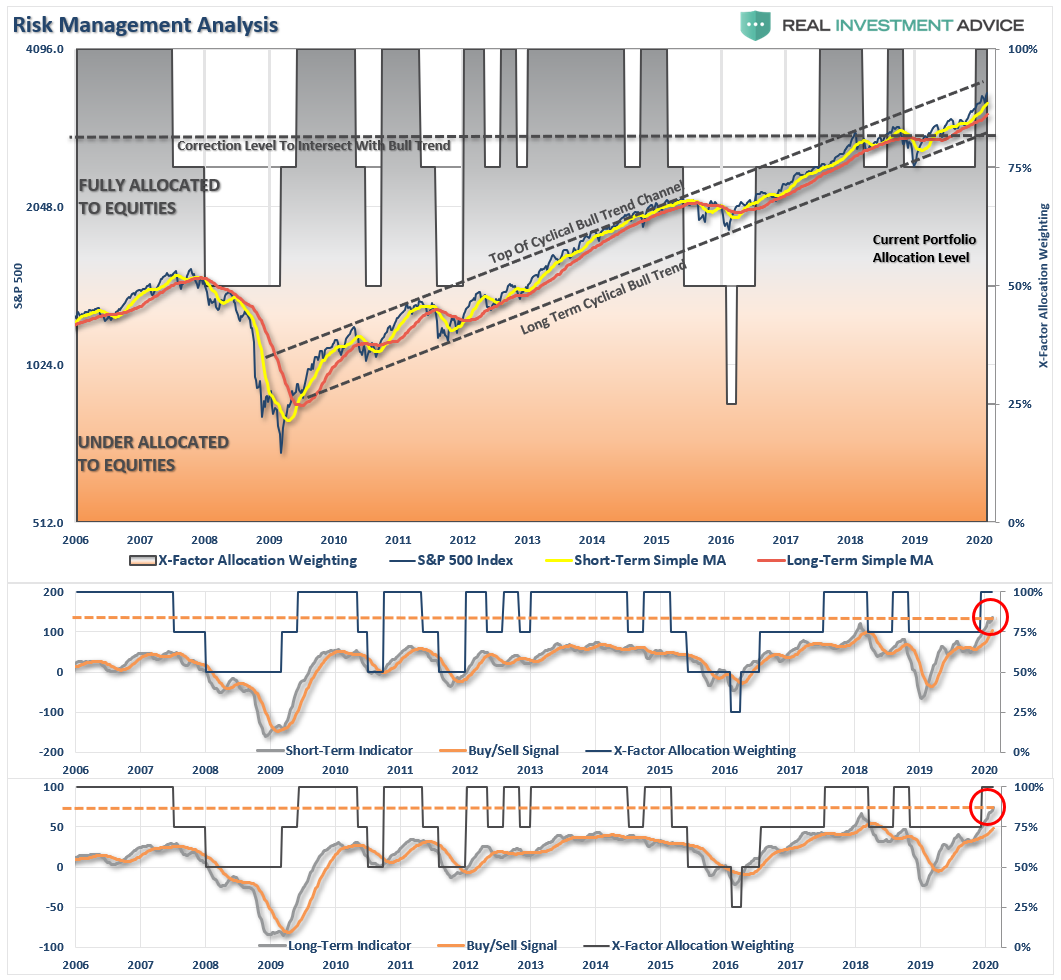

- As noted above, this chart is not about short-term trading but the long-term management of risks in portfolios. This is a quarterly chart of the market going back to 1920.

- Note the market has, only on a few rare occasions, been as overbought as it is currently. The recent advance has pushed the market into 3-standard deviations above the 3-year moving average. In every single case, the reversion was not kind to investors.

- Secondly, in the bottom panel, the market has never been this overbought and extended in history.

- As an investor it is important to keep some perspective about where we are in the current cycle, there is every bit of evidence that a major mean reverting event will occur. Timing is always the issue which is why use daily and weekly measures to manage risk.

- Don’t get lost in the mainstream media. This is a very important chart.

Nothing Out Of Kilter

This past week Ed Yardeni via Yardeni Research, made a good point:

“The markets must figure that the coronavirus outbreak will be contained soon and go into remission, as did SARS, MERS, and Ebola. If that doesn’t happen, then there will be a vaccine that will make us feel better. It won’t be a miracle cure coming from a drug company. Rather, it will be injections of more liquidity into the global financial markets by the major central banks.

On Tuesday, Fed Chair Jerome Powell implied that the Fed is on standby to do just that. In his testimony on monetary policy to Congress, he said, ‘Some of the uncertainties around trade have diminished recently, but risks to the outlook remain. In particular, we are closely monitoring the emergence of the coronavirus, which could lead to disruptions in China that spill over to the rest of the global economy.’”

Not surprisingly, the “ringing of Pavlov’s bell” once again sent investors scurrying to take on risk.

Interestingly, however, was that during Powell’s testimony to the Senate Banking Committee this past week, he said:

“There is nothing about this economy that is out of kilter or imbalanced.”

Okay, I’ll bite.

“Mr. Powell, if there is nothing out of kilter or imbalanced in the economy, then why are you flooding the system with a greater level of ’emergency’ measures than seen during the ‘financial crisis.'”

It is at this point that I feel like Mr. Lorensax from “Ferris Bueller’s Day Off.”

“Anyone…Anyone…”

- Side Note: The irony of that particular clip, is that Mr. Lorensax is asking his class about the “The Smoot-Hawley Act,” which was intended to raise revenue via tariffs and lift the U.S. out of the “Great Depression.” Just as with Trump’s recent “tariff” and “trade war,” neither worked as intended.

There is clearly something amiss within the financial complex. However, investors have been trained to disregard the “risk” under the assumption the Federal Reserve has everything under control.

Currently, it certainly seems to be the case as markets hover near all-time highs even as earnings, and corporate profit, growth has weakened. If the coronavirus impacts the global supply chain harder than is currently anticipated, which is likely, the deviation between prices and earnings will become tougher to justify.

Scott Minerd, the CIO of Guggenheim Investments, had a salient point:

“Yet as a major economic problem looms on the horizon, the cognitive disconnect between current asset prices and reality feels like the market equivalent of “peace for our time.” The average BBB bond yields just 2.9 percent. A recent 10-year BB-rated healthcare bond came to market at 3.5 percent and subsequently was increased in size from $1 billion to $1.7 billion due to excess demand.

For those investors who perceive the disconnect between risk assets which are priced for a rosy outcome and the reality of the looming risks to growth and earnings, any attempt to reduce risk leads to underperformance. It is a mind-numbing exercise for investors who see the cognitive dissonance. The frantic race to accumulate securities has cast price discovery to the side.

I have never in my career seen anything as crazy as what’s going on right now, this will eventually end badly.“

Of course, it will.

The only problem, as he notes, is that between now and then, there is a demand for performance regardless of the underlying risk. Or rather, there is a widely adopted belief the markets can never have a decline again as witnessed by an email I received last week:

“Why do you think there will ever be a correction when the central banks are never going to let credit contract. I see no corrections. Ever. When the US enters a recession, the reality is it will be the biggest buy signal yet. There is literally nowhere to go but up in this market.”

The lessons taught by previous bear markets are always forgotten during enduring bull markets which seem without end. The relearning of those lessons are always painful.

The Path Ahead

The path ahead for stocks is much less certain than in late 2018 when we were coming off deeply depressed sentiment levels, and the Fed was rapidly reversing monetary policy from “tightening” to “easing.”

With equities now more than 30% higher than they were then, the Fed mostly on hold in terms of rate cuts, and “repo” operations starting to slow, it certainly seems that expectations for substantially higher market values may be a bit optimistic.

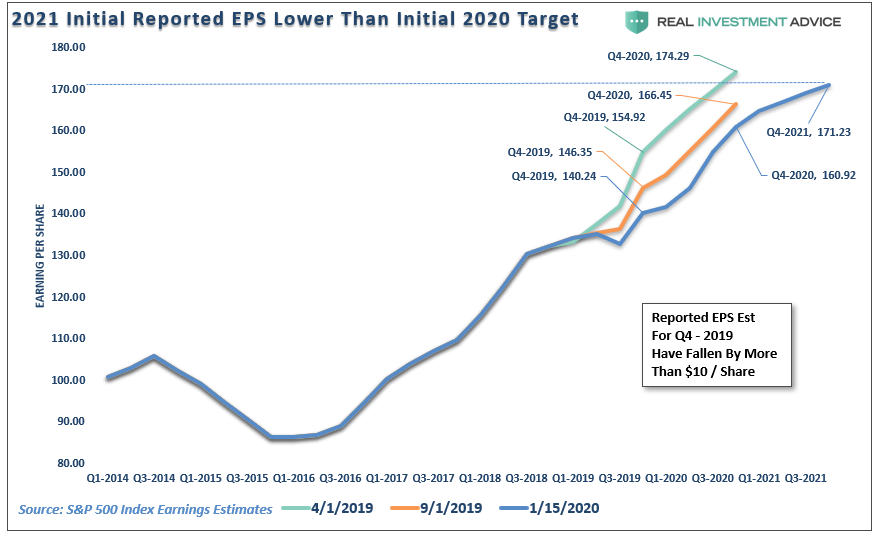

Furthermore, as noted above, earnings expectations declined for the entirety of 2019, as shown in the chart below. However, the impact of the “coronavirus” has not been adopted into these reduced estimates as of yet. These estimates WILL fall, and likely markedly so, which as stated above, is going to make justifying record asset prices more problematic.

Conversely, if by some miracle, the economy does show actual improvement, it could result in yields rising on the long-end of the curve, which would also make stocks less attractive.

This is the problem of overpaying for value. The current environment is so richly priced there is little opportunity for investors to extract additional gains from risk-based investments.

There is one true axiom of the market which is always forgotten.

“Investors buy the most at the top, and the least at the bottom.”

If you feel you must chase the markets currently, then at least do it with a set of guidelines to follow in case things turn against you. We printed these a couple of weeks ago but felt there are worth mentioning again.

- Move slowly. There is no rush in adding equity exposure to your portfolio. Use pullbacks to previous support levels to make adjustments.

- If you are heavily UNDER-weight equities, DO NOT try and fully adjust your portfolio to your target allocation in one move. This could be disastrous if the market reverses sharply in the short term. Again, move slowly.

- Begin by selling laggards and losers. These positions are dragging on performance as the market rises and tends to lead when markets fall. Like “weeds choking a garden,” pull them.

- Add to sectors, or positions, that are performing with, or outperforming the broader market.

- Move “stop-loss” levels up to current breakout levels for each position. Managing a portfolio without “stop-loss” levels is like driving with your eyes closed.

- While the technical trends are intact, risk considerably outweighs the reward. If you are not comfortable with potentially having to sell at a LOSS what you just bought, then wait for a larger correction to add exposure more safely. There is no harm in waiting for the “fat pitch” as the current market setup is not one.

- If none of this makes any sense to you – please consider hiring someone to manage your portfolio for you. It will be worth the additional expense over the long term.

While we remain optimistic about the markets currently, we are also taking precautionary steps of tightening up stops, adding non-correlated assets, raising some cash, and looking to hedge risk opportunistically.

Just because it isn’t raining right now, doesn’t mean it won’t. Nobody has ever gotten hurt by keeping an umbrella handy.

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Financial Planning Corner

- REGISTER NOW: RIGHT-LANE RETIREMENT WORKSHOP

- When: February 29th, 9-11 am (Social Security, Medicare, Income planning, Investing & More)

- Where: Courtyard Houston Katy Mills, 25402 Katy Mills Parkway, Katy, TX, 77494

You’ll be hearing more about more specific strategies to diversify soon, but don’t hesitate to give me any suggestions or questions.

by Danny Ratliff, CFP®

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

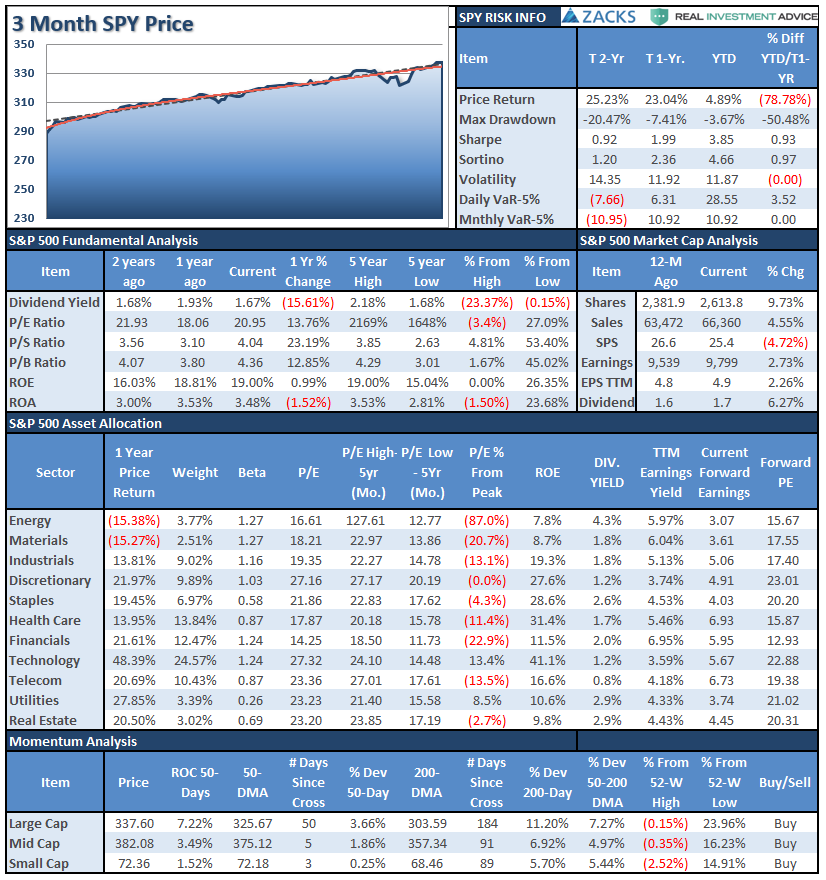

S&P 500 Tear Sheet

Performance Analysis

Technical Composite

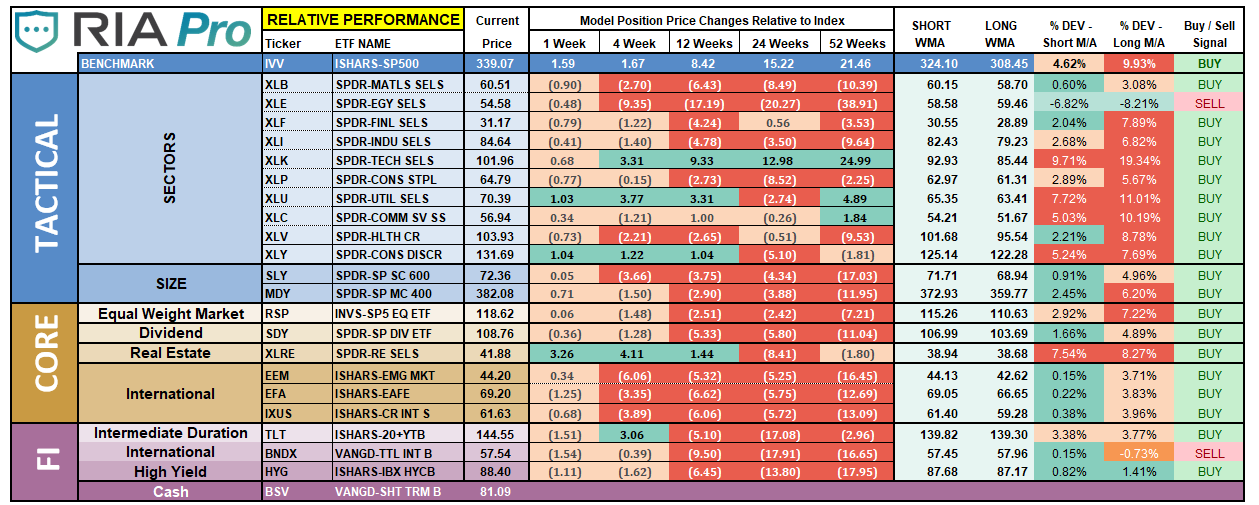

ETF Model Relative Performance Analysis

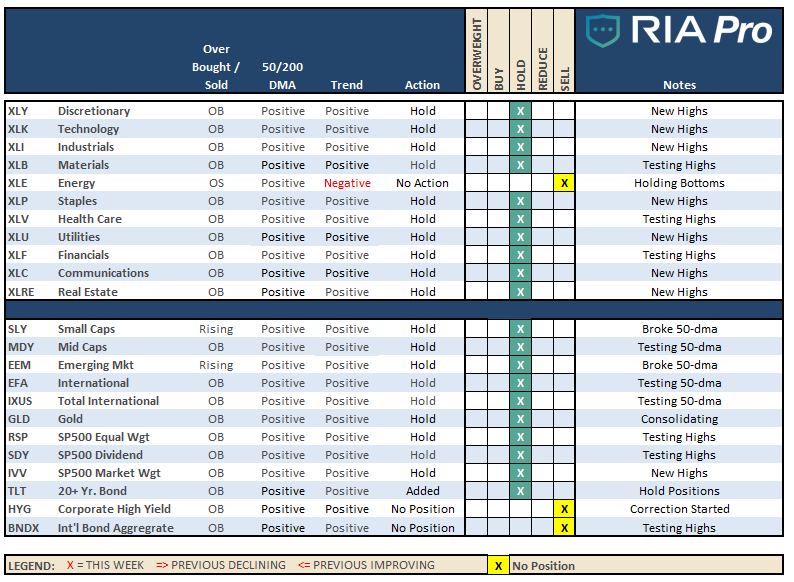

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

Sector-by-Sector

Improving – Discretionary (XLY) and Utilities (XLU)

As noted previously, we reduced exposure to Utilities and Discretionary due to their extreme overbought condition. Unfortunately, that overbought extension has not been alleviated enough at this time to add back to our holdings. We will likely see a correction in the next couple of weeks to re-evaluate our positioning.

Current Positions: Reduced XLY, XLU

Outperforming – Technology (XLK), Communications (XLC)

We previously recommended taking profits in Technology, which has not only been leading the market but has gotten extremely overbought. The rally in markets last week only further extended those overbought conditions in both Technology and Communications. Hold positions for now, and be patient for a correction to add additional exposure.

Current Positions: Target weight XLK, Reduced XLC

Weakening – Financials (XLF), Healthcare (XLV)

We noted previously added a position in Financials to our portfolios, which we will look to build into over the few weeks. We also had previously added to our healthcare slightly. Both positions ran back to overbought and need more of a correction before considering adding to them.

Current Position: 1/2 Weight (XLF), Target weight (XLV)

Lagging – Industrials (XLI), Real Estate (XLRE), Staples (XLP), Materials (XLB), and Energy (XLE)

With the Fed continuing to pump money into the financial markets, bond yields continue to drop which is supportive for interest rate sectors like Real Estate and Utilities. We previously reduced our holdings to these sectors and we need a correction to work off some of the excesses before adding back to our holdings. Both XLRE and XLU are EXTREMELY extended currently.

Industrials rallied back to new highs without working off the overbought condition. With industrials at 3-standard deviations above the long-term mean, be patient adding additional exposures.

Materials tested and failed previous highs and are testing those highs again. With the sector very overbought there is a risk of a reversal, particularly with the sector very close to registering a “sell signal.”

Energy is deeply oversold and due for a rally. We added to our position of AMLP previously, however, we are maintaining tight stops.

Staples remains in a strong uptrend and has not provided an entry point to add exposure safely.

Current Position: Reduced weight XLY, XLP, XLRE, Full weight AMLP, 1/2 weight XLB and XLI

Market By Market

Small-Cap (SLY) and Mid Cap (MDY) – Despite the rally in the broader markets, Small- and Mid-caps continue to underperform currently. Both markets rallied last week but have failed to set new highs. Small caps did recover their 50-dma, while mid-caps are currently testing previous highs. Overbought conditions are rather extreme in both.

Current Position: KGGIX, SLYV

Emerging, International (EEM) & Total International Markets (EFA)

Emerging and International Markets, look a lot like small-caps above. Both had gotten extremely overbought and needed to correct. That correction broke supports and the subsequent rally failed to set new highs. Both markets have climbed back above their respective 50-dma, but are testing that support line. We remain long our holdings currently, but are closely evaluating our positioning.

Current Position: EFV, DEM

Dividends (VYM), Market (IVV), and Equal Weight (RSP) – These positions are our long-term “core” positions for the portfolio given that over the long-term markets do rise with economic growth and inflation. We are currently maintaining our core positions unhedged for now. If we see deterioration in the broader markets, we will begin to add short-positions to hedge our long-term core holdings.

Current Position: RSP, VYM, IVV

Gold (GLD) – Over the last few weeks, gold has been consolidating near recent highs. Gold remains overbought but continues to hold important support. We are at full weight in the positions, however, if this consolidation continues, supports hold, and the overbought condition recedes, we will consider over-weighting our holdings.

Current Position: GDX (Gold Miners), IAU (GOLD)

Bonds (TLT) –

Bonds rallied back towards previous highs on Friday as money rotated into bonds for “safety” as the market weakened. After previously recommending adding to bonds, hold current positions for now and take profits next week to rebalance risks accordingly. Bonds are extremely overbought now, so be cautious, we added a small portion of TLT to portfolios last week to extend our current duration.

Current Positions: DBLTX, SHY, IEF, Added TLT

Sector / Market Recommendations

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

The market rallied this past week on continued expectations that the Fed will intervene sooner, or later, with liquidity to offset the risk of the coronavirus. As such, investors don’t want to “miss out” on the liquidity party when it happens, so they are front-running the event.

This past week, we made a couple of very minor changes to the portfolio which change very little in terms of the overall make up.

Importantly, this rebalancing of risk did not dramatically increase equity exposure. This is because, as noted above, the longer-term technical outlook remains “cautious.”

Yes, we realize we are very late-cycle, we also know that with the Fed, and global Central Banks, still intervening, we must give deference to the “bullish bias.” At the moment, that bias clearly remains, and functioned as we discussed last week.

If you have any questions, please don’t hesitate to email me.

There we no additional portfolio actions this past week.

- New clients: Slowing adding exposure as needed.

- Dynamic Model: Added LVS, and a Short-S&P 500 hedge to balance risk while trying to build out the overall model.

- Equity Model: Sold SLYV to make room to add LVS. Also added TLT to our bond portfolio to lengthen duration a little bit. Given the portfolio is fully allocated to the market positions now have to be shifted to make changes.

- ETF Model: Add a starting position of TLT to our bond portfolio to lengthen the duration of our current bond mix.

Note for new clients:

It is important to understand that when we add to our equity allocations, ALL purchases are initially “trades” that can, and will, be closed out quickly if they fail to work as anticipated. This is why we “step” into positions initially. Once a “trade” begins to work as anticipated, it is then brought to the appropriate portfolio weight and becomes a long-term investment. We will unwind these actions either by reducing, selling, or hedging if the market environment changes for the worse.

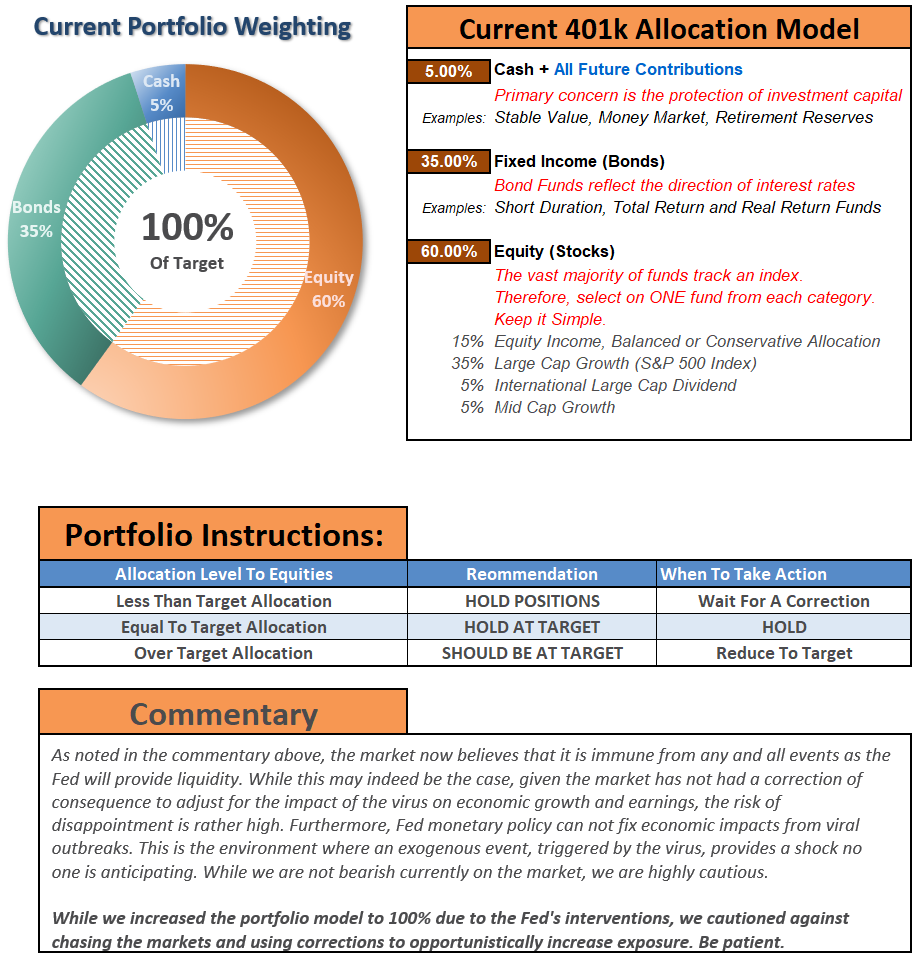

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation simplified, it allows for better control of the allocation, and closer tracking to the benchmark objective over time. (If you want to make it more complicated, you can, however, statistics show simply adding more funds does not increase performance to any significant degree.)

If you need help after reading the alert; do not hesitate to contact me.

Click Here For The “LIVE” Version Of The 401k Plan Manager

See below for an example of a comparative model.

Model performance is based on a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. This is strictly for informational and educational purposes only and should not be relied upon for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber (You get your first 30-days free) you have access to our live 401k p

The code will give you access to the entire site during the 401k-BETA testing process, so not only will you get to help us work out the bugs on the 401k plan manager, you can submit your comments about the rest of the site as well.

We are building models specific to company plans. So, if you would like to see your company plan included specifically, send me the following:

- Name of the company

- Plan Sponsor

- A print out of your plan choices. (Fund Symbol and Fund Name)

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read