The Relative Value Report provides guidance on which sectors, factors, indexes, and bond classes are likely to outperform or underperform its appropriate benchmark.

Click on the Users Guide for details on the model’s relative value calculations as well as guidance on how to read the graphs.

This report is just one of many tools that we use to assess our holdings and decide on potential trades. Just because this report may send a strong buy or sell signal, we may not take any action if it is not affirmed in the other research and models we use.

Commentary

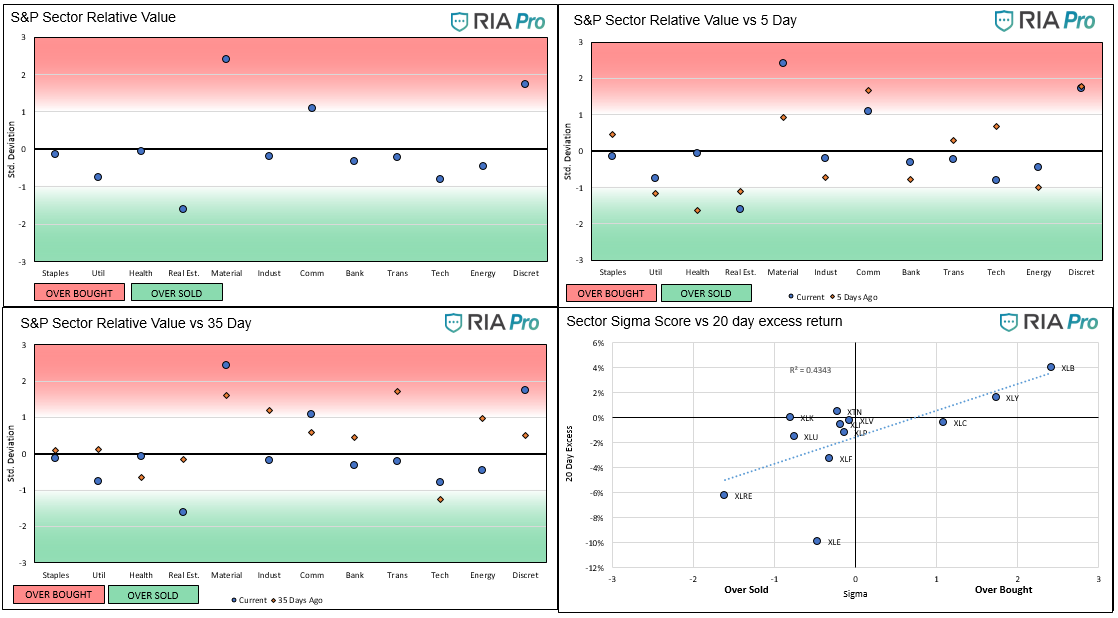

- Materials are grossly overbought versus the S&P 500 at nearly 2.5 standard deviations above fair value. Communications and Discretionary remain overbought, but not to the same degree.

- Healthcare moved back to fair value. The only cheap sector versus the S&P 500 is Real estate. We exited real estate recently as we are very uncomfortable with the fundamental underpinnings of the sector.

- Most sectors are close to fair value.

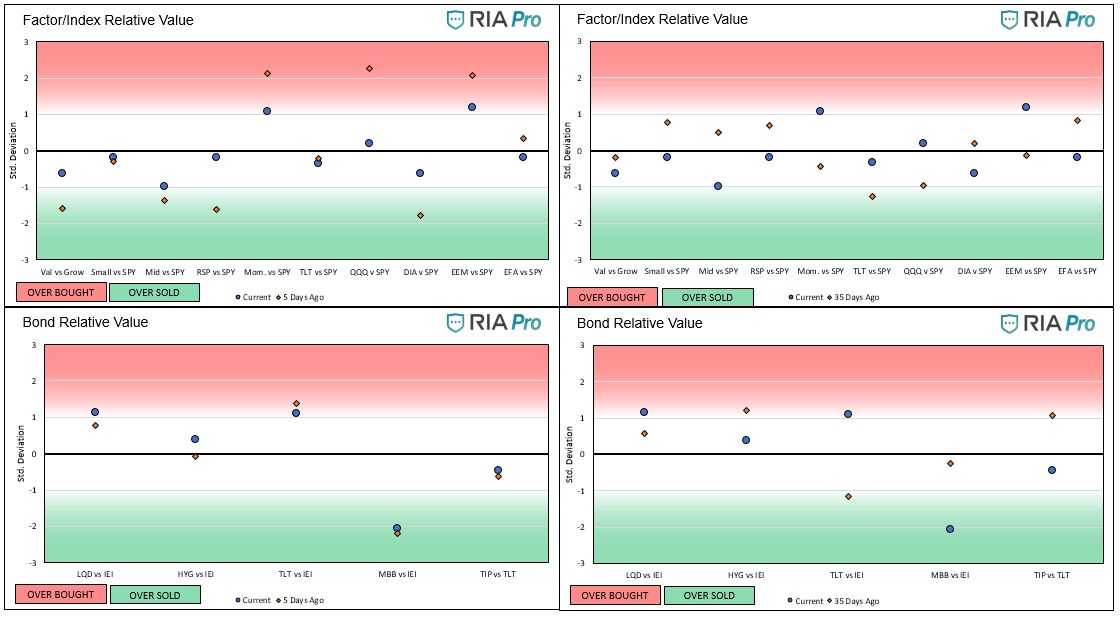

- In the Factor/Index (renamed) analysis, the laggards are finally catching up. For instance, Value versus Growth finally moved higher. Equal weighted and Mid-caps also moved back towards fair value. Conversely, the “go-go” sectors moved down toward fair value. These include Momentum, NASDAQ, and Emerging Markets.

- Like the sectors, most factors and indexes are bunched around fair value.

- Quite frankly, with bond yields barely moving, the fixed income analysis is boring. Note that little changed versus last week. Mortgages remain oversold.

- The R-squared on the sigma/20 day excess return (Sectors) scatter plot is .43. XLE is significantly reducing the correlation as its score is not reflective of recent performance versus the S&P 500. We ran the graph without XLE, and the correlation rose to nearly .70.

Graphs (Click on the graphs to expand)

The ETFs used in the model are as follows:

- Staples XLP

- Utilities XLU

- Health Care XLV

- Real Estate XLRE

- Materials XLB

- Industrials XLI

- Communications XLC

- Banking XLF

- Transportation XTN

- Energy XLE

- Discretionary XLY

- S&P 500 SPY

- Value IVE

- Growth IVW

- Small Cap SLY

- Mid Cap MDY

- Momentum MTUM

- Equal Weighted S&P 500 RSP

- NASDAQ QQQ

- Dow Jones DIA

- Emerg. Markets EEM

- Foreign Markets EFA

- IG Corp Bonds LQD

- High Yield Bonds HYG

- Long Tsy Bonds TLT

- Med Term Tsy IEI

- Mortgages MBB

- Inflation TIP

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read