The fleecing of retail investors continues as “payment for order flow” expands.

Payment for order flow (PFOF) is not new. Previously, in a less connected world of instantaneous data flows, PFOF was minimal and non-invasive. Today, with high-frequency trading, dark pools, and algorithms running amok, retail traders are fodder for Wall Street profits.

Some Background

In financial markets, PFOF refers to compensation a broker receives third parties to influence how the broker routes client orders for fulfillment.

Read that again.

For many years, paying for order flows allowed firms to centralize customers’ orders for another firm to execute. Such allowed smaller firms to use economies of scale of larger firms. By allowing small firms to combine orders with larger firms, it provided better execution quality.

Over the years, the decimalization of the trading securities diminished the profitability of trade execution. Such pushed Wall Street toward PFOF as a way to generate revenue and subsidize the move to zero-commissions.

The advances in technology and data analysis increased the speed with which information gets sent and received. Over the last decade, Wall Street spent billions to figure out ways to take advantage of the data and “game the system.”

Today, Robinhood, and others, generate the bulk of their revenues from selling order flows to the highest bidder.

Free Isn’t Necessarily “Free”

Think about this carefully. If a firm is selling order flow to the highest bidder, even though you are paying “zero commissions,” you are not necessarily getting the best execution.

In other words, “free” isn’t necessarily “free.”

Such was a point Doug Kass made recently:

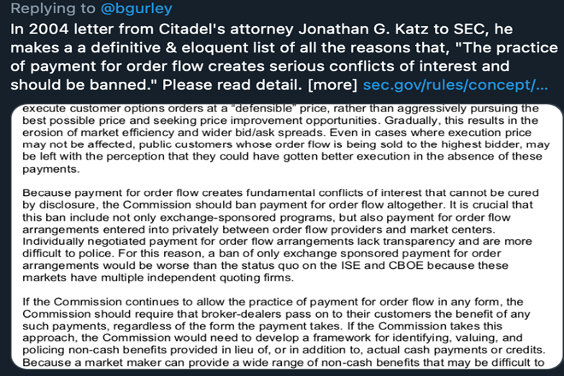

“In 2004, Citadel made the argument to the SEC the practice of selling order flow should be illegal.”

During the 90s, several firms offering “zero-commission trades” routed orders to market makers failing to execute in investors’ best interests.

Such was during the waning days of fractional pricing, and for most stocks, the smallest spread was ⅛ of a dollar, or $0.125. Spreads for options orders were considerably wider. Traders discovered their “free” trades cost them quite a bit since they didn’t get the best transaction price.

At that point, the SEC did step in to conduct a study. The result was a near ban on PFOF. The study found, among other things, the proliferation of options exchanges narrowed spreads due to the additional competition for order execution.

In the end, under pressure from Wall Street, the SEC acquiesced and allowed the practice to continue stating:

“While the fierce competition by increased multiple-listing produces immediate economic benefits to investors in the form of narrower quotes and effective spreads. By some measures these improvements get muted with the spread of payment for order flow and internalization.”

That decision opened “Pandora’s box.”

If You Can’t Beat’em

If you can’t beat em, join em, I guess!

“Citadel Securities trading operation, which is separate from Citadel’s hedge fund business, generated $3.84 billion of revenue. Net income was $2.36 billion in the first six months of 2020.“

Read that again.

“Net income normally means after tax. Such implies Citadel is making an 80%+ EBIT margin in a highly competitive business with tight spreads. This occurs with scale competitors that are also super smart.

It is akin to Amazon (AMZN) and Microsoft (MSFT) both selling cloud services. However, Amazon does for one penny what it costs Microsoft 10 pennies to do. Amazon is slightly better than Microsoft, but not 10x.” – Doug Kass

It Costs You More Than You Think

As I stated, there is no free lunch.

“A key to keep money flowing to brokers, and so-called market makers, is to ensure retail traders remain unaware.

Such in why Robinhood allegedly broke the law and paid a $65 million fine (without admitting to any wrong-doing) to settle an SEC action. The violation was for not telling its clients it was selling their orders and making a ton of money in payment for order flows.

The other key part of the scheme is the trumpeted misleading claim of ‘commission free trading,’ which too many hear as ‘free trading.'” – Better Markets

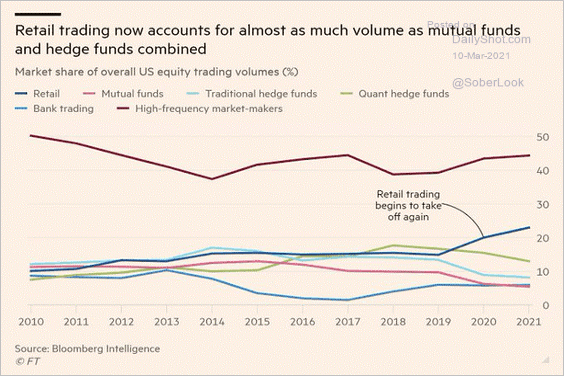

A well-known fact of behavioral science is that “free’ goods or services” (or those perceived to be “free”) get over consumed. Such is why retail trading skyrocketed since the industry started de facto selling “free trading.” As shown in the chart below, retail trading now comprises as much volume as professional managers.

Show Me The Money

As Better Markets goes on to discuss, the payment for order flow is “all about the money.”

“As is clear from the billions paid for, and made from, order flows, there is no such thing as ‘free trading.’

Thus, the claim of ‘commission-free trading’ is no more than a rhetorical ruse to attract new investors. Such distracts them from the billions of dollars in PFOF and other hidden costs that come out of retail investors’ pockets.

These intermediaries are often merely transferring the investors’ visible upfront commissions into invisible after-the-fact de facto commissions.

Such enables the complexity of the fragmented order processing system that one could argue is designed primarily to hide those payments.” – Better Markets

Such is why Wall Street lobbies the SEC heavily to look the other way. They also continue to obfuscate the “racket” under the guise of “creating market liquidity.”

Without PFOF, liquidity remains regardless as Wall Street would merely shift their focus back to market making.

The Pigeon At The Poker Table

If you don’t think this is a “big deal,” you are sorely misinformed.

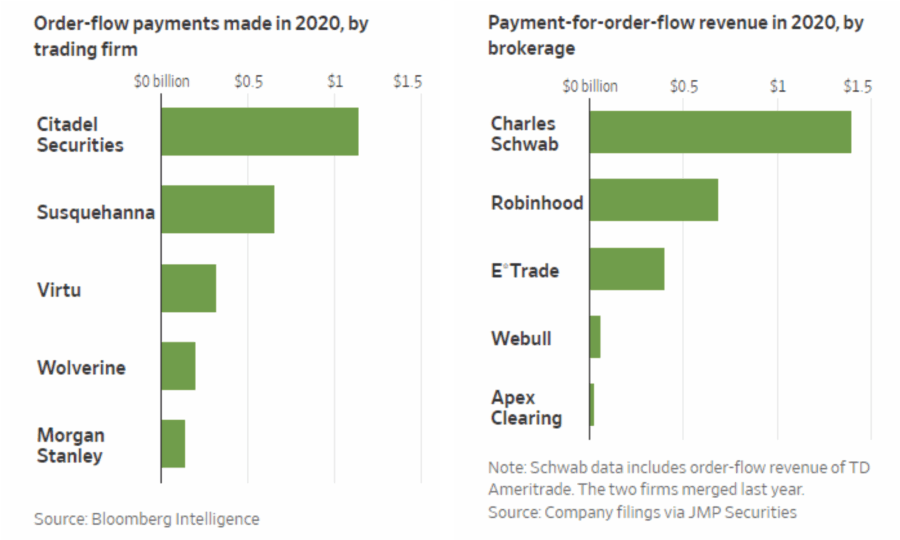

“Last year, brokerages such as Charles Schwab Corp., TD Ameritrade, Robinhood Markets Inc., and E*Trade collected nearly $2.6 billion in payments for stock and option orders. The biggest sources of the payments were electronic trading firms such as Citadel Securities, Susquehanna International Group LLP and Virtu Financial Inc.” – WSJ

“Such firms make money by selling shares for slightly more than they are willing to buy them, and pocketing the price difference.”

So, exactly why would firms pay for order flow?

They are willing to pay for order flow from online brokerages because they are less likely to lose money trading against individual investors than on an exchange, where traders tend to be larger and more sophisticated.” – WSJ

As the old saying goes, if you look around the poker table and can’t spot the “pigeon,” it’s probably you.

Market Manipulation

So, if you haven’t asked yourself the question yet, why would a firm like Citadel pay hundreds of millions to buy order flow?

The actual spreads due to decimalization are minimal, so what is the real value?

Citadel, as noted, has two components – an execution arm and a hedge-fund. If the hedge fund, which manages billions of dollars, can use high-frequency trading to place orders just ahead of the execution of order flows, the profitability is enormous.

“Payment for order flow, at the end of the day, is legalized bribery that appears to incentivize brokers to violate rules.” – WSJ

Of course, it isn’t just Citadel. It is all significant hedge funds that actively compete with one another. Due to massive computing power, servers’ co-location reduces latency between order executions, and the exchanges can arbitrage the trades. As such, hedge funds only need “nano-seconds” for their algorithms to analyze incoming orders and place trades accordingly.

Such is what the book “Flash Boys” by Michael Lewis ultimately revealed.

The ability to “front-run” investor orders is a highly profitable business practice, even if it is both illegal and unethical.

Conclusion

As is always the case, there is too much money and pressure from Wall Street on the SEC. As Better Markets concluded:

“There is no reason for the markets today to be so fragmented other than to serve as a wealth extraction mechanism that moves money from buy-side pockets to sell-side firms, intermediaries and their affiliates.

However, it isn’t just Robinhood and a couple of hedge funds, but rather a collaboration of every Wall Street player.

“Thus, while the direct and obvious participants in the market chaos like Robinhood, Reddit, Citadel, and the short-sellers must get intensely scrutinized, the many other financial firms, including the marquee Wall Street banks, driving, enabling, funding, and incentivizing these activities — and enriching themselves from them — must also get thoroughly reviewed.” – Better Markets

Yes, payment for order flow allows you the ability to trade with “zero commissions.” However, there are two costs:

- You probably aren’t getting the best execution; and

- You probably trade more actively, increasing risk in your portfolio.

Therefore, it is safe to assume that “free, really isn’t free.”

Maybe paying a small commission for “fair execution” wasn’t so bad after all.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read