As we get ready to wind up the week, we wanted to share with you a few thoughts about our outlook going forward along with our favorite 5-positions that align with these ideas.

There is a lot of “hope” currently that the Fed’s monetary policies are going to drive asset prices higher. While we are certainly not discounting that possibility, there are also some major headwinds for the markets in this regard.

- A major support of asset prices over the last decade, stock buybacks, are gone.

- Jobless claims hitting levels never seen in history

- Unemployment that will hit 15% or more, and will be a long-time in recovering.

- Dramatic declines in both consumer and investor confidence.

- A loss of many small businesses which make up 45% of GDP and 70% of employment.

- A draining of corporate coffers.

- Lack of access to capital or credit markets outside those loans guaranteed by the Fed.

- Surging mortgage forbearance.

- Rising consumer credit card and auto-defaults

- A dollar funding shortage

- A sharp decline in retail sales and personal consumption expenditures.

I could go on, but you get the idea.

It ain’t good.

Importantly, this will all translate into the most important thing for the markets – earnings.

As I noted Tuesday in “The Reward Doesn’t Justify The Risk:”

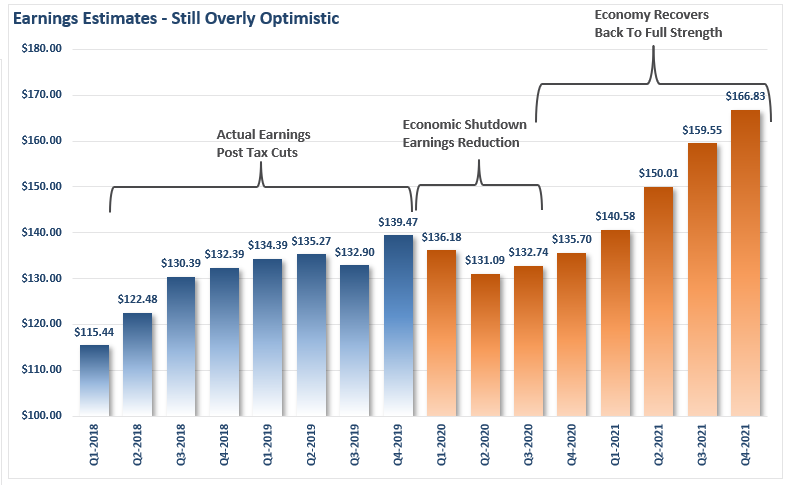

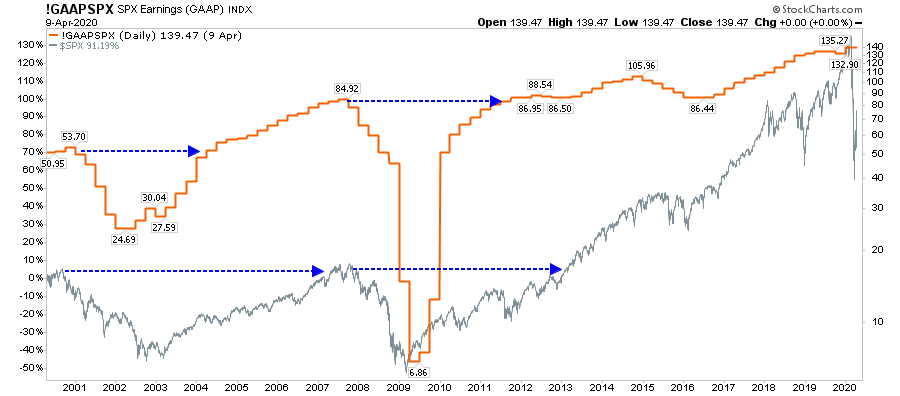

“The chart below shows the most current estimates as of April 2020. As you can see, earnings are expected to decline from Q4-2019 levels of $139.47 to $136.18 and $131.09, respectively in Q1 and Q2 of 2020. That is a decline of -2.3% in Q1 and a total decline of -6% in Q2.”

“So, with the entire U.S. economy effectively shut down, 15-20% unemployment, and -20% GDP, earnings are only expected to take a 6% hit?

- In 2008, without an economic shutdown, S&P 500 earnings fell from $84.92 to $6.86. That is a decline of 92% from the peak, and earnings did not fully recover until 3-years later in Q3-2011.

- Or in 2000, during the “dot.com crash,” earnings fell from $53.70 to $24.69, or a decline of 54%. Earnings did not fully recover until 4-years later in Q2-2004.”

With that analysis, and a bit of an understanding of our expectations of the economy, and markets, going forward, here are the 5-stocks we like the best in our portfolios currently.

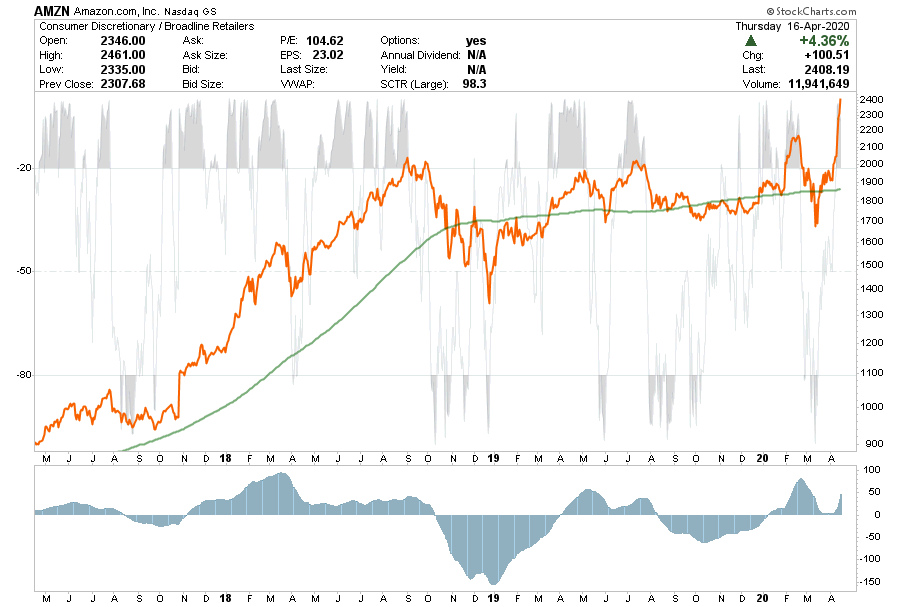

AMZN

With everyone locked down at home, Amazon recently had to start hiring 75,000 workers to meet demand. While discretionary spending is being crushed for many retailers, as noted in the recent retail sales report, the beneficiaries are companies like AMZN, WMT and COST.

We bought AMZN last October in anticipation of a pickup for the holiday shopping season, but with the economic shutdown, it has pushed many buyers onto their platform. With AMZN now getting extremely overbought, most of the “value” has been built into the price. Hold off adding new positions for now and look for a pullback to the previous breakout level to add exposure.

Earnings are likely to weaken as the economic situation worsens, so be patient and pick your spots longer term.

- Target Price: 2700

- Stop Loss: 1900 (No good stop loss point currently until a pullback occurs.)

ABT

There is a common theme between our Equity and ETF portfolio: “Long Staples, Healthcare & Technology, and out of most everything else.” The reason is that these sectors continue to outperform the S&P overall, and have a bit of “virus” protection to them.

On the healthcare front, we are very happy with Abbott Laboratories. ABT reported good earnings yesterday and are on the forefront of getting “COVID-19 testing kits” to the market very quickly.

Currently, ABT is very overbought, but we will look for any weakness that holds breakout level to increase our position size. (We also like our holdings in JNJ, ABBV, and CVS for many of the same reasons.)

- Target Price: $105

- Stop: $82.50

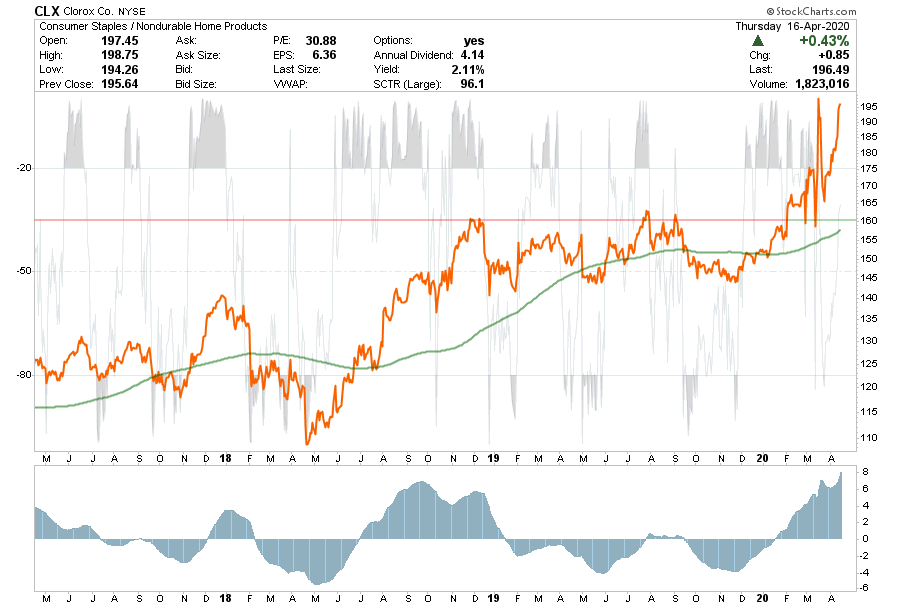

CLX

We have a lot of favorites in our STAPLES cart: PG, COST, CAG and others, but our favorite right now is CLX.

Clorox is obviously a “virus” pick as the need for disinfecting everything continues to rise. As the virus peaks, and begins to pass, and life returns to normal we will likely reduce our holdings and take profits.

However, overall, STAPLES are an important category to our portfolio makeup currently as a defensive measure against recession. Regardless of job losses, unemployment, etc., people still have to buy toilet paper (in more normal amounts), toothpaste, shampoo, etc. They also have to manage their overall HEALTHCARE particularly as baby boomers are “moved out to pasture.”

Like many things in our portfolio, CLX is overbought short-term. Look for pullbacks to support to add exposure carefully, and take profits when the virus begins to fade.

- Target Price: $215

- Stop: $165

IAU

There are three reasons we own gold.

- The Fed

- The Fed

- The Fed

While monetary stimulus has not been proven to be inflationary in the past, as it is an asset swap, this time may be different because of the economic shut down.

With massive amounts of liquidity sloshing around the market, when the economy re-opens, eventually, there could well be an inflationary impulse that gets ahead of the Fed. If inflation heats up this will be good for gold. In such a case, the Fed would need to reverse the monetary jets to avoid inflation. Given it took 7 years after the financial crisis to even begin QT, we find it probable the Fed will be even slower this time.

Also, as noted below, we own gold to offset the risk of a global dollar shortage which is becoming a serious problem currently in the global markets.

Lastly, gold tends to act as a “hedge” against market volatility which reduces our overall portfolio risk if something happens to break.

- Target Price: $20.00

- Stop: $14.75

UUP

Lastly, our long dollar position is very important to us.

“The Federal Reserve has identified the Achilles heel of the world economy: the enormous global shortage of dollars. The global dollar shortage is estimated to be $13 trillion now, if we deduct dollar-based liabilities from money supply including reserves.

How did we reach such a dollar shortage? The reason is simple, domestic and international investors do not accept local currency risk in large quantities knowing that, in an event like what we are currently experiencing, many countries will decide to make huge devaluations and destroy their bondholders.

According to the Bank of International Settlements, the outstanding amount of dollar-denominated bonds issued by emerging and European countries in addition to China has doubled from $30 to $60 trillion between 2008 and 2019. Those countries now face more than $2 trillion of dollar-denominated maturities in the next two years and, in addition, the fall in exports, GDP and the price of commodities has generated a massive hole in dollar revenues for most economies.

If we take the US dollar reserves of the most indebted countries and deduct the outstanding liabilities with the estimated foreign exchange revenues in this crisis … The global dollar shortage may rise from 13 trillions of dollars in March 2020 to $ 20 trillion in December … And that is if we do not estimate a lasting global recession.” – Mises Institute.

This is why we are long the dollar now, and will likely increase it to as much as 10% of our portfolio in the future.

The Federal Reserve can not “fix” this problem. It is too big and it is growing. The rest of the world needs at least $20 trillion by the end of the year. Even if the Fed increases their balance sheet to $10 trillion, the US dollar shortage would remain.

“In the current circumstances, and with a global crisis on the horizon, global demand for bonds from emerging countries in local currency will likely collapse, far below their financing needs. Dependence on the US dollar will then increase. Why? When hundreds of countries try to copy the Federal Reserve printing and cutting rates without having the legal, investment and financial security of the United States, they fall into a trap of ignoring the demand of their own currency.” – Mises

Two things:

- The dollar is going to rise and likely by a lot as the global recession intensifies.

- A strong dollar is not good for the stock market.

Have a great weekend.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read