In this edition of the Value Seeker Report, we analyze an investment opportunity in Dick’s Sporting Goods (NYSE: DKS) using fundamental and technical analysis.

Overview

- It’s no secret that people are spending more time outdoors as a result of the pandemic. For some, the shock to their daily routine caused by countrywide lockdowns has begun to feel like a prison. What can one do when they work from home and going to the gym, restaurants, sporting events, and concerts are all off the table?

- Dick’s Sporting Goods (NYSE: DKS) is a sporting goods retailer in the United States. The Company belongs to the Consumer Discretionary sector and currently has a market cap of $5.2B.

- DKS’s stock is currently trading at $60.26 per share. Using our forecasts, we arrive at an intrinsic value of $68.76 per share. This implies an upside of roughly 14% on the investment.

Pros

- DKS is adapting well to the challenges currently facing traditional brick-and-mortar retailers. DKS is leveraging its retail stores as distribution centers to offer consumers competitive shipping as well as same-day store pickup. Since lockdowns began, the firm’s e-commerce sales have skyrocketed.

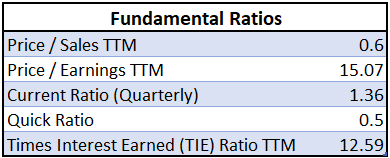

- DKS is currently trading above its pre-pandemic range. However, due to earnings tailwinds, DKS has an attractive P/E ratio relative to the broad market.

- The stock trades at a Price to Earnings (P/E) ratio of 15.1. The chart below illustrates how DKS’ P/E ratio has evolved since 2002.

- DKS has paid a quarterly dividend since 2015. Shareholders have received $0.3125 per share through the first three quarters of fiscal 2021, which is an improvement from $0.275 per share in fiscal 2020. The stock’s current dividend yield is 2.09%.

- As shown below, our forecasts indicate that DKS has nothing to worry about concerning its dividend payments. Further, we estimate that DKS currently holds excess cash with a balance of roughly $350M. This could be used to repurchase shares if Management chooses to do so.

Cons

- Consumer spending will suffer if congress does not provide citizens with more stimulus soon, and discretionary items will feel the majority of this impact. DKS could see its bolstered demand fade as a result.

- AMZN poses a substantial threat to sporting goods retailers of all shapes and sizes. It’s worth noting that DKS is attempting to minimize this threat by taking a value added approach to the market. Beyond offering a wider selection of sporting goods products, DKS trains specialist employees in all departments. They are designated to assist customers in selecting the product that best fits their needs, even in very specific applications.

Key Assumptions

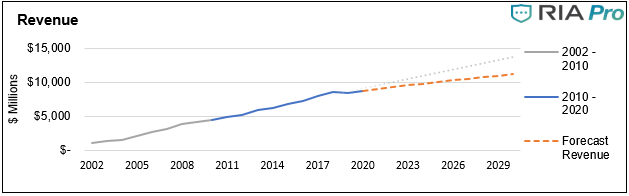

- Revenue will grow in fiscal 2021 as a result of demand tailwinds caused by lockdowns and social distancing. We assume DKS will be successful in defying the infamous ”retail apocalypse”, and see strong growth in fiscal 2022 and beyond. The chart below illustrates our forecasts in relation to historical revenue.

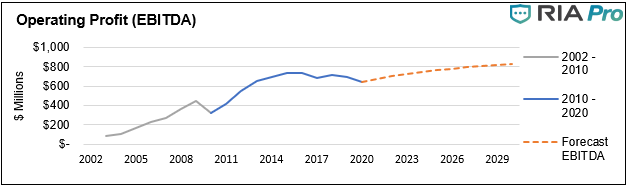

- Although DKS has seen margin deterioration in recent years, lockdown-induced demand has boosted margins year to date. We forecast EBITDA margin to increase slightly from last year and remain relatively steady thereafter.

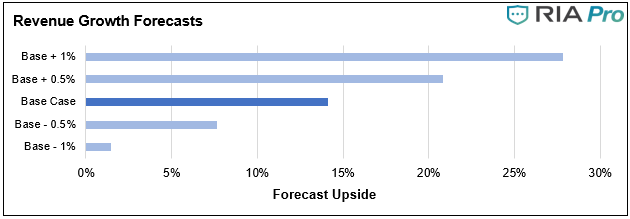

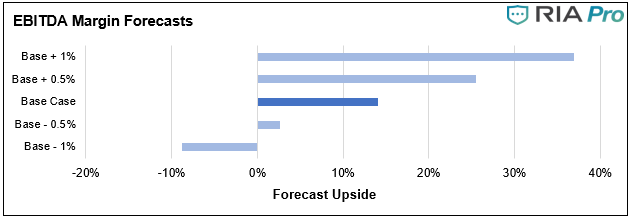

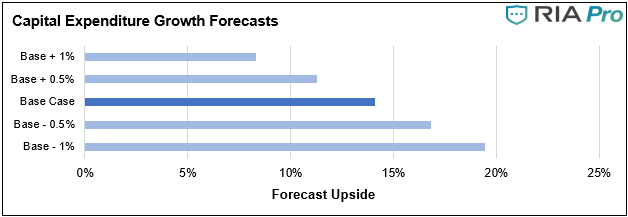

Sensitivity Analysis

- A brief note on why we present sensitivity analysis can be found here.

- Our analysis points to the importance of our profit margin forecasts to DKS’ intrinsic value. Given that DKS has seen declining margins over the past few years, it appears that competition with AMZN is the main risk to be aware of.

Technical Snapshot

- DKS remains in a bullish trading channel which began in May. The stock is currently testing short-term resistance at $59 per share with room to run above there.

- Investors should look for relatively strong support around $53, with the 50-day moving average just below that.

Value Seeker Report Conclusion On DKS

- DKS is handling the pandemic well, and the firm’s second quarter results reflect that sentiment. Management has a strategy in place for DKS to compete in the current environment and post-pandemic, which will likely pay off for investors.

- Based on our forecasts, DKS has 14.1% of upside remaining before reaching its intrinsic value.

For the Value Seeker Report, we utilize RIA Advisors’ Discounted Cash Flow (DCF) valuation model to evaluate the investment merits of selected stocks. Our model is based on our forecasts of free cash flow over the next ten years.

Nick Lane

Nick Lane Investment Analyst

A native of Kingwood, Texas Nick attended college at the University of Houston. He completed a BBA in Accounting and Finance and 2018 and then a Masters of Science in Finance in 2020. Outside of work, Nick enjoys both saltwater and freshwater fishing as well as following various professional sports leagues.

2020/10/02

Also Read