In this edition of the Value Seeker Report, we analyze an investment opportunity in CVS Health (NYSE: CVS) using fundamental and technical analysis.

Overview

- CVS is a provider of health care services to corporations and individuals in the US and Puerto Rico. The Company has a market cap of $75.9B and is in the Health Care sector.

- CVS has four operating segments: Pharmacy Services, Retail/Long-Term Care, Health Care Benefits, and Corporate/Other.

- CVS stock is currently trading at $58.00 per share. Using our forecasts, we arrive at an intrinsic value of $85.35 per share. This implies an upside of 47.1% on the investment.

Pros

- Although the Health Care sector has clawed its way back to just 5.2% below its 52-week high, CVS still lingers almost 25% below its 52-week high. This is quite puzzling, as the pandemic’s impact on CVS does not warrant the market’s reaction.

- CVS has paid a quarterly dividend of $0.50 per share in each of the last three years and there is little doubt CVS will be able to maintain the dividend. The stock’s current dividend yield is 3.45%.

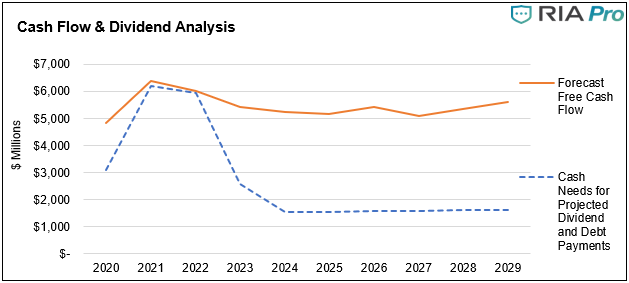

- Our forecasts (as shown below) indicate that CVS will produce the free cash flow required to maintain its dividend and repay some debt over the forecast period.

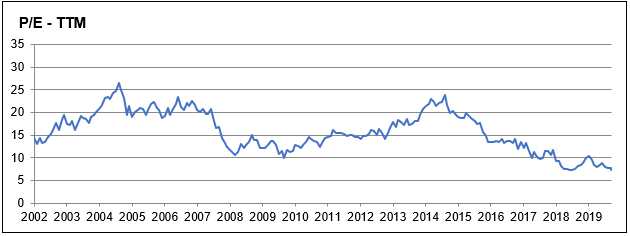

- The stock trades at a Price to Earnings (P/E) ratio of 7.3. The chart below illustrates the significant discount CVS investors are receiving from a P/E standpoint.

Cons

- With Amazon’s (NYSE: AMZN) entry into the health care sector, competition has intensified as CVS and its peers race for better positioning. Although AMZN still faces some regulatory barriers, the e-commerce giant’s resources pose a threat to CVS’ margins.

- One of the more apparent risks to an investment in CVS is that the stock price simply fails to move it intrinsic value in a timely manner. Just as we see no reason for the stock’s underperformance thus far, we cannot pinpoint a catalyst for the stock’s move to intrinsic value.

Key Assumptions

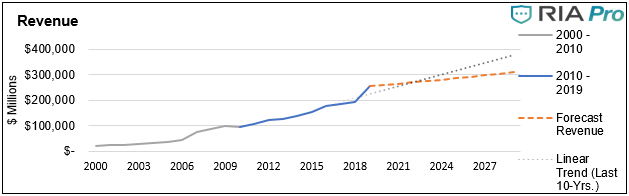

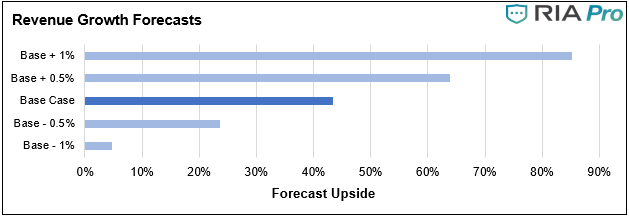

- Revenue growth for 2020 is based on results from the first half of the year as well as Management’s comments and outlook. We assume growth in 2021 and beyond will remain muted, as CVS is a mature firm with revenue growth supported by acquisitions.

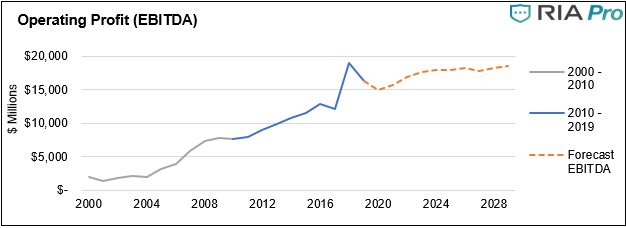

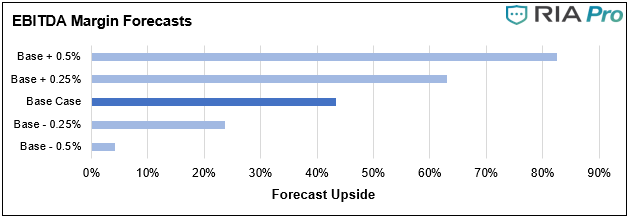

- We forecast CVS operating margins to begin slightly below their 2019 level as CVS faces incremental expenses related to the pandemic. By 2023, margins will return to pre-pandemic levels then slowly fade to the long-term forecast as competition heats up.

- Management has mentioned debt repayment as being a priority through 2022. Accordingly, we forecast debt to decrease as a portion of assets, and included the effects in the free cash flow and dividend analysis.

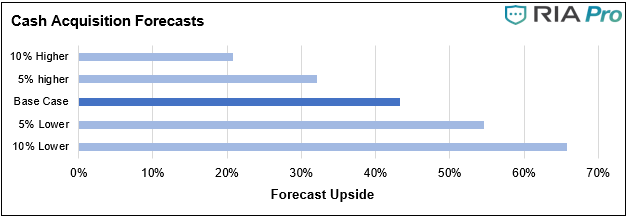

- CVS will continue to increase its scale through acquisitions. Acquisition activity will remain relatively weak at first, as Management improves the balance sheet. Beyond 2022, cash acquisitions will move toward CVS’ 5-year historical average, although they will not quite reach that level.

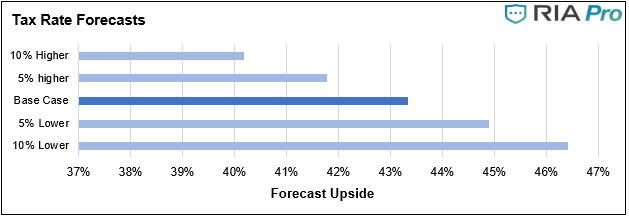

Sensitivity Analysis

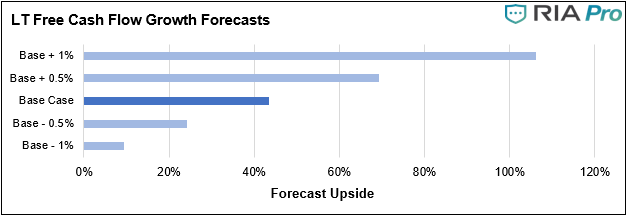

- A brief note on why we present sensitivity analysis can be found here.

- The analysis helps us understand that the level of acquisitions needed for CVS to achieve the forecast revenue growth will be critical to the stock’s intrinsic value. Fortunately, in the least favorable of the outcomes explored, CVS still offers attractive upside.

- Realized EBITDA margins also will be critical to CVS’ intrinsic value. If AMZN intensifies competition and lowers industry margins as a whole, CVS’ investors could see little upside.

Technical Snapshot

- After receiving a pummeling, which began in mid-August, the stock is approaching critical support at $58 per share. At the same time, CVS is approaching its most oversold level since the beginning of 2020. There will be a good buying opportunity if the stock can bounce off that support.

- If CVS holds support at $58, it will face a few instances of minor resistance in the near term. However, the real test will be whether the stock can break above its 200-day moving average. It has failed to do so in its last three attempts.

Value Seeker Report Conclusion On CVS

- CVS is currently priced at a deep discount to its intrinsic value. We forecast that roughly 47.1% of upside remains on the stock.

- We cannot find justification for its lagging performance, and thus cannot pinpoint a catalyst that will move the stock to its intrinsic value. However, even considering the possibility that the stock continues to lag before moving to intrinsic value, the deep discount makes the investment worthwhile. In the meantime, investors will receive a dividend yield of 3.45%.

For the Value Seeker Report, we utilize RIA Advisors’ Discounted Cash Flow (DCF) valuation model to evaluate the investment merits of selected stocks. Our model is based on our forecasts of free cash flow over the next ten years.

Nick Lane

Nick Lane Investment Analyst

A native of Kingwood, Texas Nick attended college at the University of Houston. He completed a BBA in Accounting and Finance and 2018 and then a Masters of Science in Finance in 2020. Outside of work, Nick enjoys both saltwater and freshwater fishing as well as following various professional sports leagues.

2020/09/11

Also Read