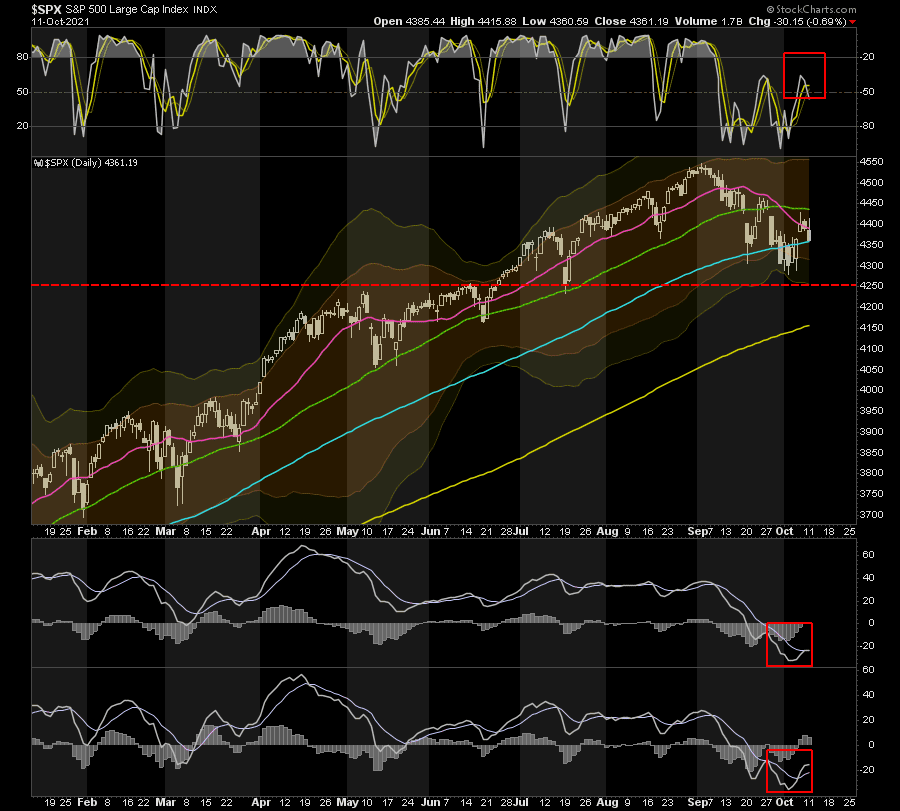

The market’s sell-off yesterday sets up a critical test of support at the 100-dma. Last week, the market was able to regain the 100-dma as stocks rallied off lower support. The decline yesterday left stocks touching the running moving average. It is a critical technical juncture for stocks. If stocks can hold the 100-dma, it will provide a support level stocks can build off of for a push higher to the 50-dma. A failure of that support will lead to a retest of recent lows or potentially more. With a lot of economic news and earnings releases this week, it is hard to guess where markets will head to next.

What To Watch Today

Economy

- 6:00 a.m. ET: NFIB Small Business Optimism, September (99.5 expected, 100.1 during prior month)

- 10:00 a.m. ET: JOLTS Job Openings, August (10.954 million expected, 10.934 million during prior month)

Earnings

- No notable reports scheduled for release

Politics

- The International Monetary Fund (IMF) will release its World Economic Outlook at 9 a.m. ET. The IMF will also release the Global Financial Stability Report at 10:30 a.m. ET.

Courtesy of Yahoo

Pain In The Supply Chain

(By @marketoonist)

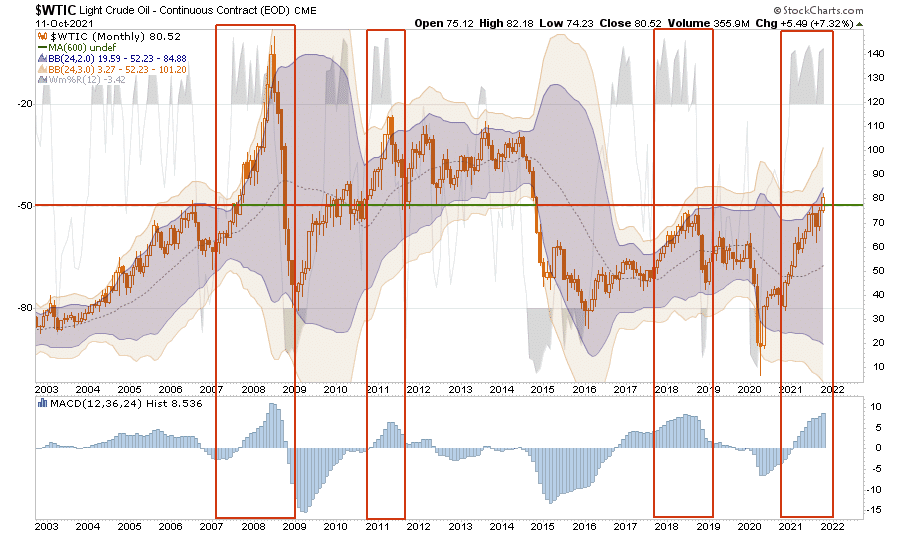

Oil Prices May Peak Here Soon

Crude oil has gotten a lot more interesting as of late. After a brutal 2020, the price of oil futures going negative at one point, oil is now pushing above $80/bbl. Given current views of “inflation” from the massive liquidity infusions and supply chain disruptions, the focus on speculative positioning is not surprising.

As shown in the monthly chart below, the price advance in crude oil is now back to historical extremes that have previously denoted tops in oil prices. The current extreme overbought, extended, and deviated positioning in crude will likely lead to a rather sharp correction. (The boxes denote previous periods of exceptional deviations from long-term trends.)

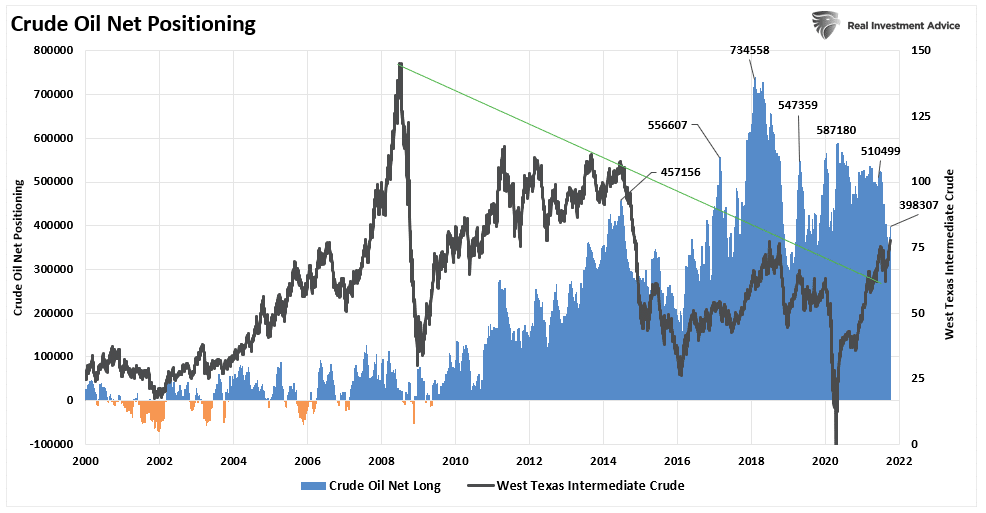

The speculative long-positioning is driving the dichotomy in crude oil by NCTs. While levels fell from previous 2018 highs during a series of oil price crashes, they remain elevated at 398,307 net-long contracts and rising quickly.

The good news is that oil did finally break above the long-term downtrend. However, it is too soon to know if these prices will “stick,” or as the economy decelerates towards the end of the year, oil prices will decline.

Furthermore, the deflationary push and the dollar rally will likely derail oil prices if it continues.

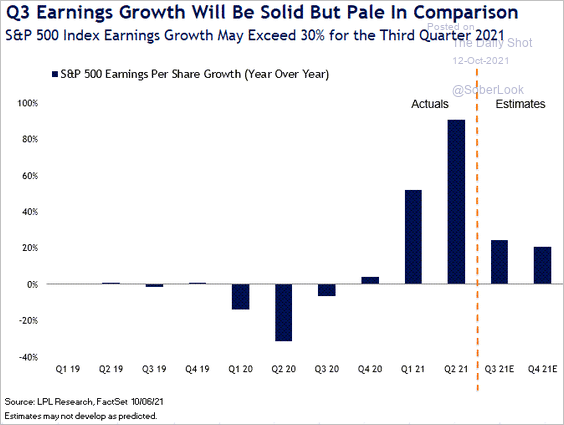

Earnings Will Begin To Slow

As we kick off the Q3 earnings season, expectations are still for a very robust earnings season. However, given much tougher year-over-year comparisons, rising inflationary pressures, ongoing supply chain disruptions, and declining consumer confidence, there is risk to those outlooks. We expect forward estimates will start to ratchet down sharply over the next couple of quarters as slower economic growth drags on margins.

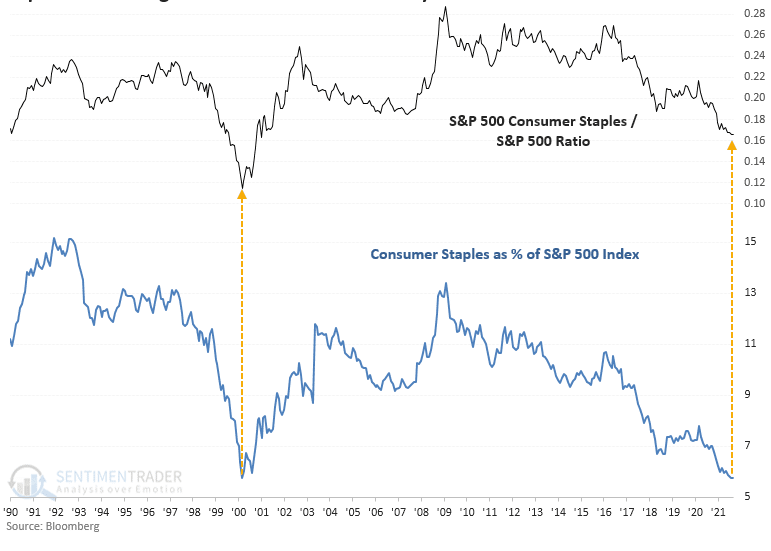

Staples Getting Historically Cheap

In last Friday’s Technical Value Scorecard in RIA Pro we discussed how cheap the consumer staples sector was getting. To wit: “However, staples are nearly three standard deviations below its 50dma, arguing for a bounce in the coming days.“

SentimentTrader follows up our work with a much longer-term view. As shown below, staples, at about 6% of the S&P 500, have the lowest weighting in the S&P 500 since the tech boom in late 1999. In the year 2000 when that bubble popped, staples (XLP) ended the year up 42%. The S&P was down 10% and the technology sector (XLK) was down over 40%.

The Real Impact of $80 Oil

A Big Week Ahead

Buckle up! This is a big week for key economic data. The JOLTs report on Tuesday will provide more color on the labor market and specifically if job openings continue to at record levels. Wednesday features CPI and the Fed minutes from their September meeting. Given the importance of inflation to the Fed, CPI will help them further hone in on how to taper QE, in regards to amounts and timing. More inflation data follows Thursday with PPI. Retail Sales and the University of Michigan Consumer Sentiment Survey come out on Friday.

Also on tap are the 10 and 30-year Treasury auctions on Tuesday and Wednesday respectively. It will be interesting to see if demand is strong given the recent backup in yields.

If you crave more information, have no fear, earnings for the major banks start on Wednesday with JPM. Many of the largest banks follow them on Thursday. Most other companies will release earnings over the coming six weeks. Beyond earnings and revenues, investors will be paying close attention to forward guidance, in particular how inflation is affecting their bottom line.

Dividends Over Oil Production

Last Friday we wrote how oil rig counts were rising slower than is typical considering the current price of oil. Another consideration is the transition to cleaner forms of energy. As Reuters writes below, companies like Occidental are not clamoring to increase production.

(Reuters) – U.S. oil and gas producer Occidental (OXY.N) wants to raise margins and re-establish dividend payments for its shareholders rather than focus on growing its production volumes, Chief Executive Vicki A. Hollub said on Thursday.

Oil companies can best contribute to the energy transition by producing just enough oil to meet demand in a way that is more efficient and produces fewer emissions, the CEO said.

“We don’t see that in 2022 and beyond that we need to grow significantly,” Hollub said at an online event by the Energy Intelligence Forum.

“Our growth in the period, and maybe over the next ten years, will more be to reestablish dividend and grow that dividend”.

Also Read