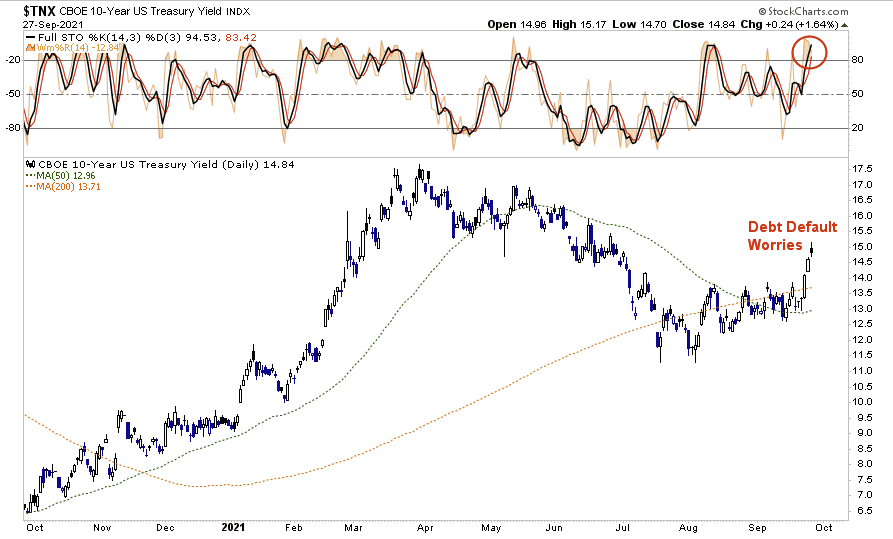

This morning market futures are lower, and yields spiking, after Republicans blocked the Democrats attempt to suspend the debt ceiling until after the mid-term elections. While the Democrats are trying to paint the Republicans as “economic destroyers,” the reality is that Democrats can pass a continuing resolution and lift the debt ceiling without any assistance. The Democrats can also pass the $3.5 trillion spending bill, hike taxes, and complete Biden’s agenda without Republican help. The problem for Democrats, is that they will “own it all” heading into the mid-terms, which is why they are pushing for bipartisan support.

However, the threat of a Government shutdown, and potential default, has sent interest rates spiking with the 10-year Treasury now pushing the highest level since June.

What To Watch Today

Economy

- 8:30 a.m. ET: Advance goods trade balance, August (-$87.3 billion expected, -$86.4 billion in July)

- 8:30 a.m. ET: Wholesale inventories, month-over-month, August preliminary (0.6% in July)

- 8:30 a.m. ET: Retail inventories, month-over-month, August (0.4% in July)

- 9:00 a.m. ET: FHFA House Price Index, month-over-month, July (1.5% expected, 1.6% in July)

- 9:00 a.m. ET: S&P CoreLogic Case-Shiller 20-City Composite Index, month-over-month, July (1.70% expected, 1.77% in June)

- 9:00 a.m. ET: S&P CoreLogic Case-Shiller 20-City Composite Index, month-over-month, July (20.0% expected, 19.08% in June)

- 10:00 a.m. ET: Conference Board Consumer Confidence Index, September (115.0 expected, 113.8 in August)

- 10:00 a.m. ET: Richmond Fed Manufacturing Index, September (10 expected, 9 in August)

Earnings

- 4:10 p.m. ET: Micron Technology (MU) is expected to report adjusted earnings of $2.34 per share on revenue of $8.23 billion

Politics

- U.S. Treasury Secretary Janet Yellen and Federal Reserve Chairman Jerome Powell will testify before the Senate at 10 a.m. ET. They will discuss nominal oversight of the CARES Act, but the debt ceiling and cryptocurrency are likely to come up.

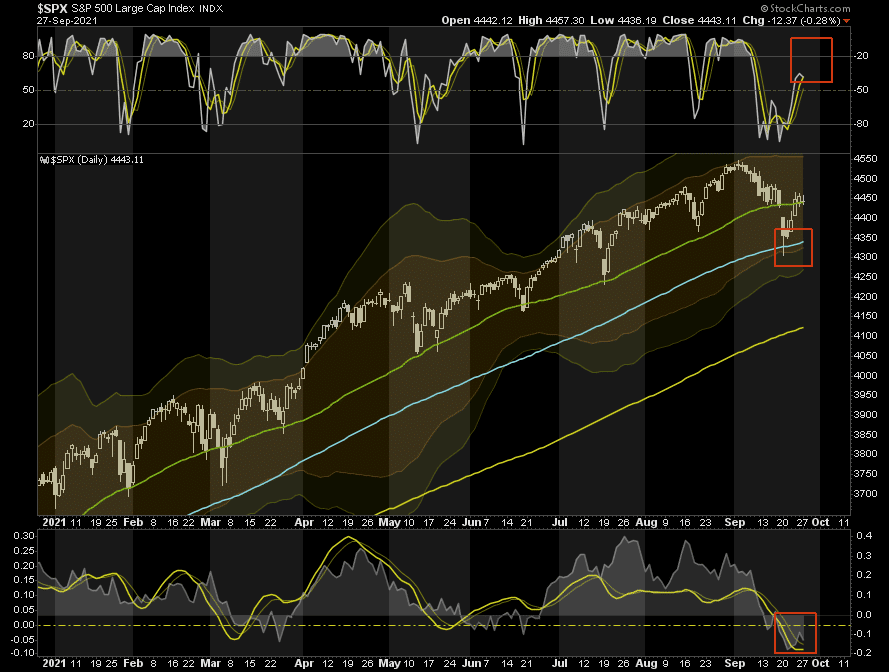

Stocks Hold Key Support

Stocks took a tumble out of the gate yesterday but held support at the 50-dma numerous times. While the 50dma was key support last week, all eyes should now focus on the 100dma. That level proved to be the key market support during the recent 5% rout from market highs.

Importantly, if the 50-dma fails to hold, the 100-dma (blue line) is now critical support between a bullish retest of recent lows or the start of a more bearish decline to the 200-dma. With markets still fairly oversold short-term, we suspect support will hold and a push higher is likely over the next few days as we wrap up Q3.

Today’s market action will give us more clues as to what happens next.

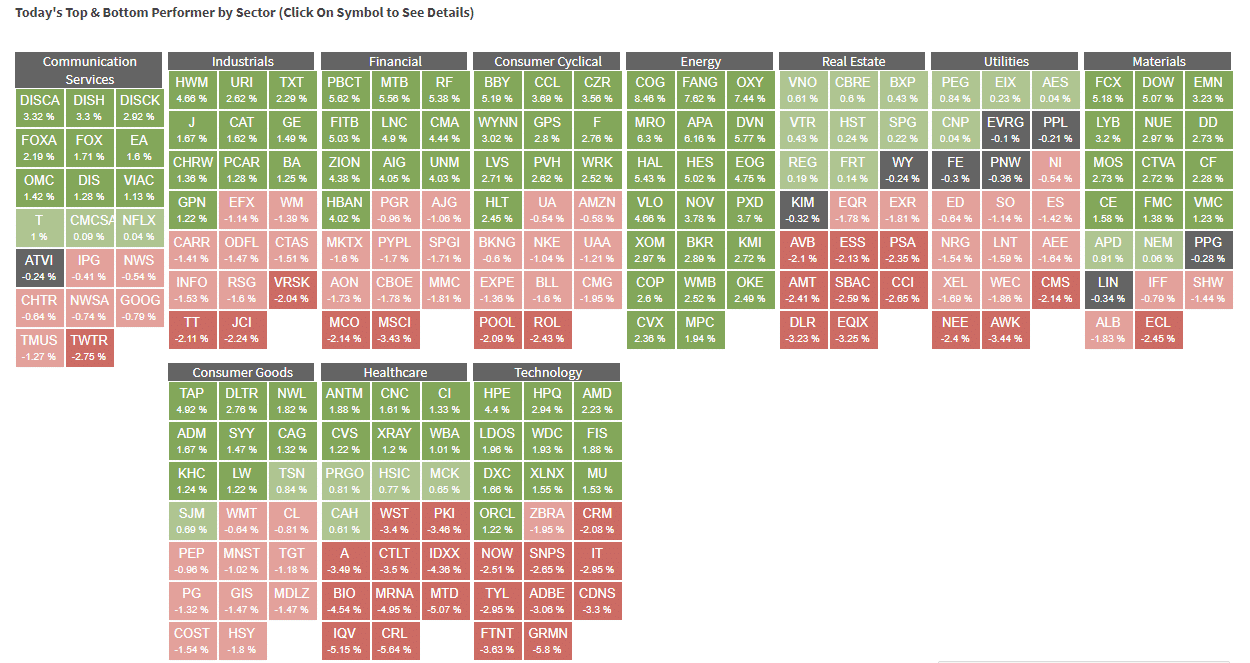

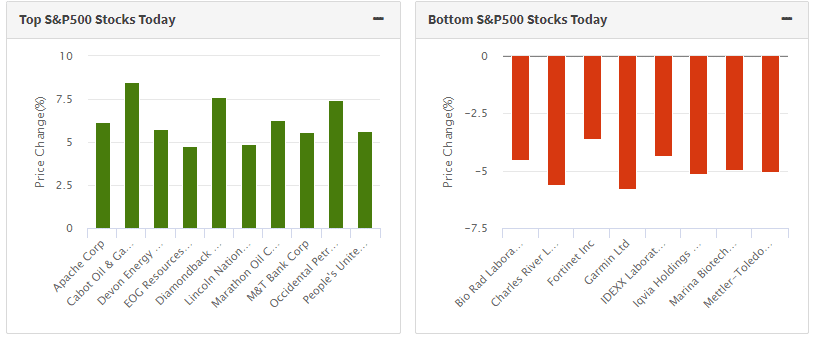

Breadth Remains Very Weak

Breadth continues to be a concern in the markets as of late. As shown below, the heatmap of the S&P 500 index was centered on financials and energy, with heavy weakness in technology.

We can also see it in the Top 10 and Bottom 10 stocks with the greatest relative change in price (Energy versus Biotech).

Overall, the vast majority of sectors and markets remain technically very weak which should raise some concerns for the bulls longer term. If the bull run is going to continue, overall breadth and strength must improve.

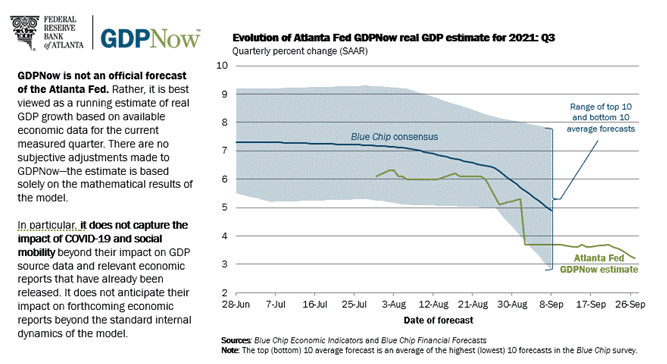

Atlanta Fed GDPNow

The Atlanta Fed GDPNow forecast for Q3 GDP continues to fall. It now stands at 3.2%, down from 3.7% a week ago, and is now almost half of what it was in mid-August. As shown, the delayed forecast from economists is at 5% but following the GDPNow trend lower.

Is Resistance Futile?

Higher Fuel Prices are a Vote Killer

Northwestern University quantifies the effect of higher oil prices on a President’s approval rating. Per the Financial Times: “A study by researchers at Northwestern University in 2016 found that for every 10-cent rise in petrol prices, the approval rating of the incumbent president dropped by 0.6 percentage points, after controlling for other factors.”

With the mid-term elections a year away and oil prices on the verge of a breakout higher we may start to see the administration pressuring Chairman Powell to better control inflation. Powell is up for renomination as his term expires in February. Will political expediency push the Fed to tighten more aggressively than they might have otherwise?

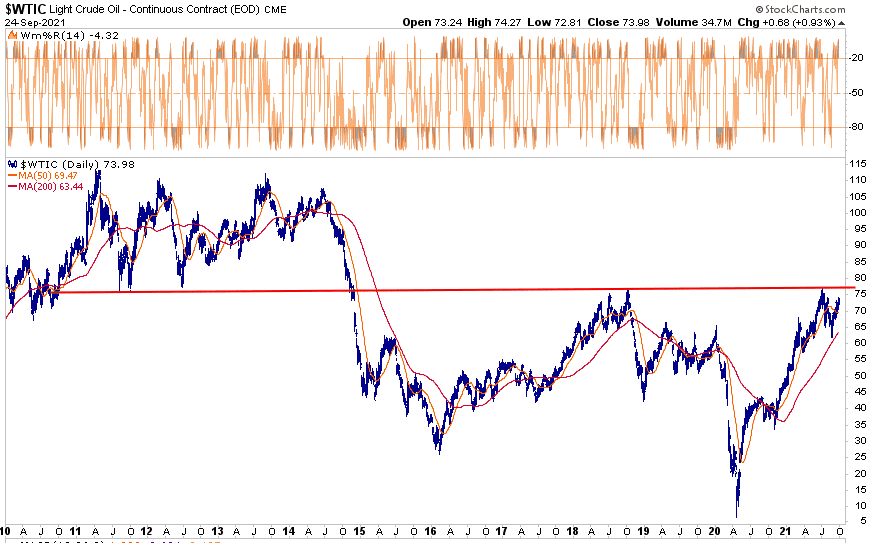

Critical Technical Resistance For Crude

As we show below, crude oil is sitting just under $77 a barrel. Over the last ten years, that price has marked significant support and more recently resistance. A decent break above $77 and there is little resistance before possibly seeing triple-digit prices. Shortages in Britain are providing a tailwind to the price. Goldman Sachs is optimistic, raising their price target on Brent Crude oil to $90 for year-end.

The Week Ahead

This week will mark a quarter-end so expect a little more volatility as traders do a little window dressing.

There are a decent number of economic data points this week. We lead off today with Durable Goods Orders and the Dallas Fed Manufacturing Index. Later this week the Richmond Fed, ISM, and Chicago PMI will provide more updates on the state of manufacturing. Given heightened concerns over inflation, the reports’ prices sub-index and related comments will be important. On that same thought, the PCE price index for August will be released on Friday. The Fed prefers PCE over CPI. Current expectations are for a gain of 0.3% versus 0.4% last month.

There will be plenty of Fed speakers this week. Many of them will further clarify their thoughts and outlooks for monetary policy going forward. Keep an ear out for any comments on Evergrande and China, and their implications for economic growth and ultimately policy.

Also Read