A March stock market rally is likely, but does that mean the risk of a bear market is over?

So far, 2022 has been challenging for investors who got lulled into complacency since the March 2020 lows. The massive deluge of liquidity flooded financial markets, providing an effortless trading environment for inexperienced investors.

In “Retail Investors Are Long On Confidence,” we quoted Jason Zweig:

“As surely as the sun rises in the east, promoters will be touting these returns. A small-stock fund manager who’s up 40% over the past year can hype that gain in ads and on social media; 40% is a big, beautiful number! Only by reading the fine print would you be reminded that a 40% return underperformed the average by more than 10 percentage points.

You knew I would tell you this but I’m saying it anyway. These returns won’t last indefinitely. Enjoy them while they last, but you’d be crazy to count on such giant gains becoming common.

At times like these, grounding yourself in realistic expectations is more important than ever. Working in the garden also reminds me that market cycles, like nature’s seasons, can be extended — but not rescinded.”

The biggest problem for most young investors is the lack of research on the stocks they buy. They are only buying them “because they were going up.”

However, as Jason notes, when the “season does change,” the “fundamentals” will matter, and they tend to matter a lot. Such is something that most won’t learn from “social media” influencers.

As of late, with stimulus checks gone and many of the high flying stocks of the last two years decimated, the “season has certainly seemed to change.”

But after two months of bearish action, could a March stock market rally be in the offing?

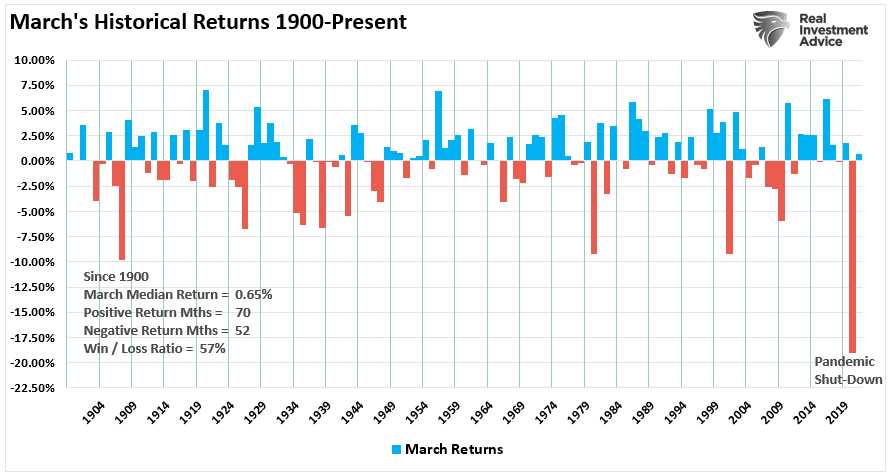

March Stock Markets Tend To Be Positve

This past weekend’s newsletter noted that the market had become oversold and well extended below the 50-dma.

“With the market closing firmly higher on Friday, a short-term buy signal, and not overbought yet, there are three rally targets for the market currently:”

- The 200-dma (red line)

- The current downtrend line; and,

- The 50-dma (black line)

Furthermore, along with a conducive technical backdrop, the historical March stock market tendencies are also supportive. As shown, the month of March, which falls within the “seasonally strong” period of the year, has a win rate of 57%.

While not the strongest month of the seasonally strong period, after two months of selling, the odds increase for a more positive month heading into the Federal Reserve’s FOMC meeting on March 15-16th.

If the Fed is more “doveish” in its positioning, the markets are likely to respond positively, given the recent increase in geopolitical risk.

Furthermore, the selloff since January was institutional positioning ahead of a potentially more aggressive Federal Reserve. Those actions created a buildup of negative positioning in the financial markets that could provide the “fuel” for a reasonably sharp rebound.

Hedging For A Crash That Didn’t Come

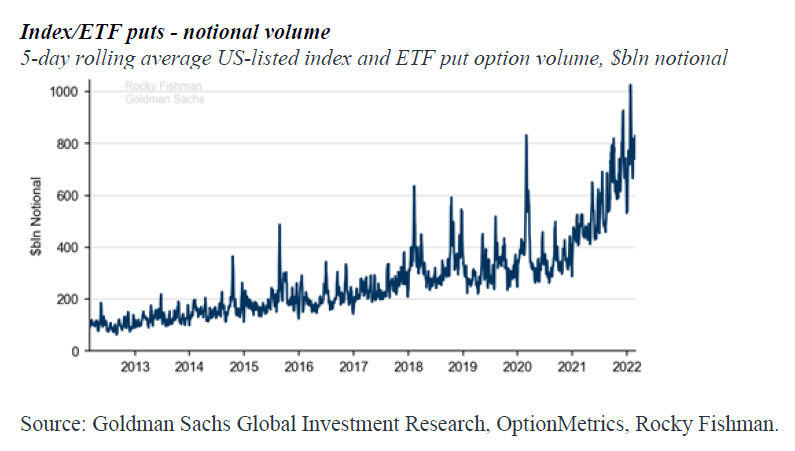

In the latest “tactical flow-of-funds” report from Goldman Sachs, several graphs show this buildup of negative positioning.

Put Monetization (large unwinds) which created net delta to buy and rich volatility fade strategies. I do not say this often. I think that investors were properly hedged up this time around for a market correction. The “event” was clearing in the sense that it catalyzed unwinds of hedges. We have been averaging $1 Trillion worth of puts per day, the largest notional on record.

We were very close to a “Markets in Turmoil” program on CNBC.

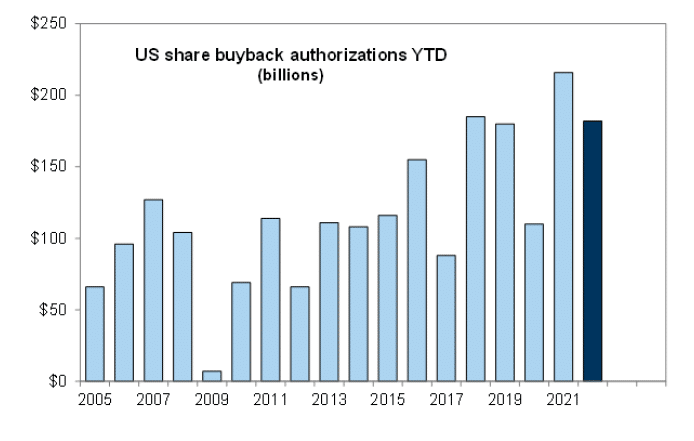

A historically significant amount of puts outstanding provides fuel for a March stock rally as positioning gets reversed. Furthermore, one of the primary supports of the market since 2011, and accounting for 40% of the rally since then, remains corporate share buybacks.

“Corporates have dry powder. 80% of the corporate window is open. Color from our buybacks desk is the number of active programs is currently 2x what we normally see. We anticipate activity increasing 15-20% in the next couple of weeks. Repurchase authorizations have moved ahead of last year’s pace. $230bln vs. $218bln YoY. Furthermore, 2021 was the most active year in history with $1.2tln in authorizations.” – GS Securities Division, Neil Kearns.

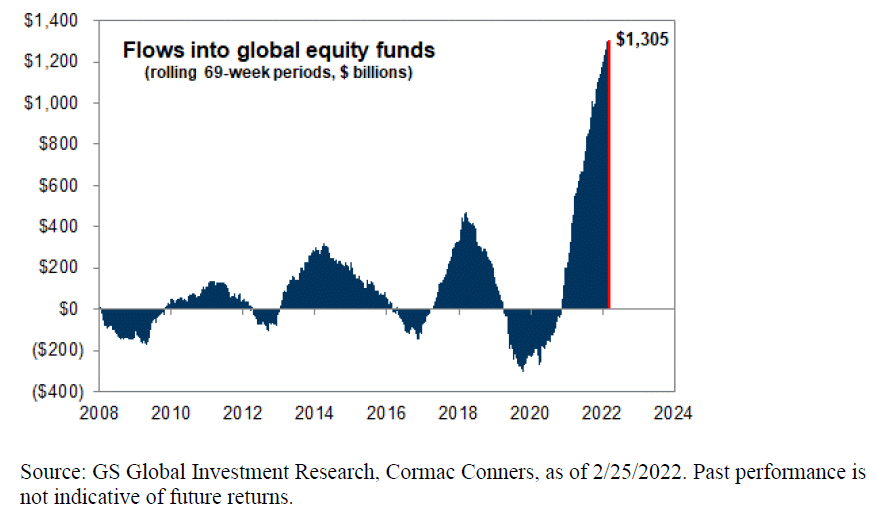

Despite the recent negative headlines, net global inflows continue to remain strong. Such a surge is unprecedented, and the eventual reversal will be problematic.

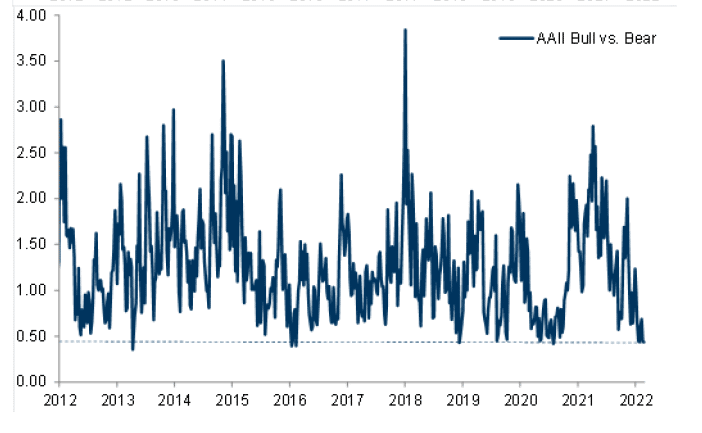

However, one of the best indicators for a rally is negative investor sentiment which is at the lowest levels since the markets wrestled with Brexit in 2016.

Does the current backdrop of a technically oversold market and highly negative sentiment and positioning mean the risk of a “bear market” is gone?

The Risk Of A Bear Market Remains

As noted, the data suggests that we could see a reasonably strong rally over the next few weeks, the risk of a more protected corrective cycle remains. Such is due to the many headwinds still facing a market that remains overvalued by many measures.

- Geopolitical risk from Russia and Ukraine

- Rising interest rates

- Surging inflationary pressures

- Economic growth slowing

- Profit margins under pressure

- A disappointment in earnings growth

- Reversal of monetary liqudity

- Surging oil prices; and, of course,

- The Fed

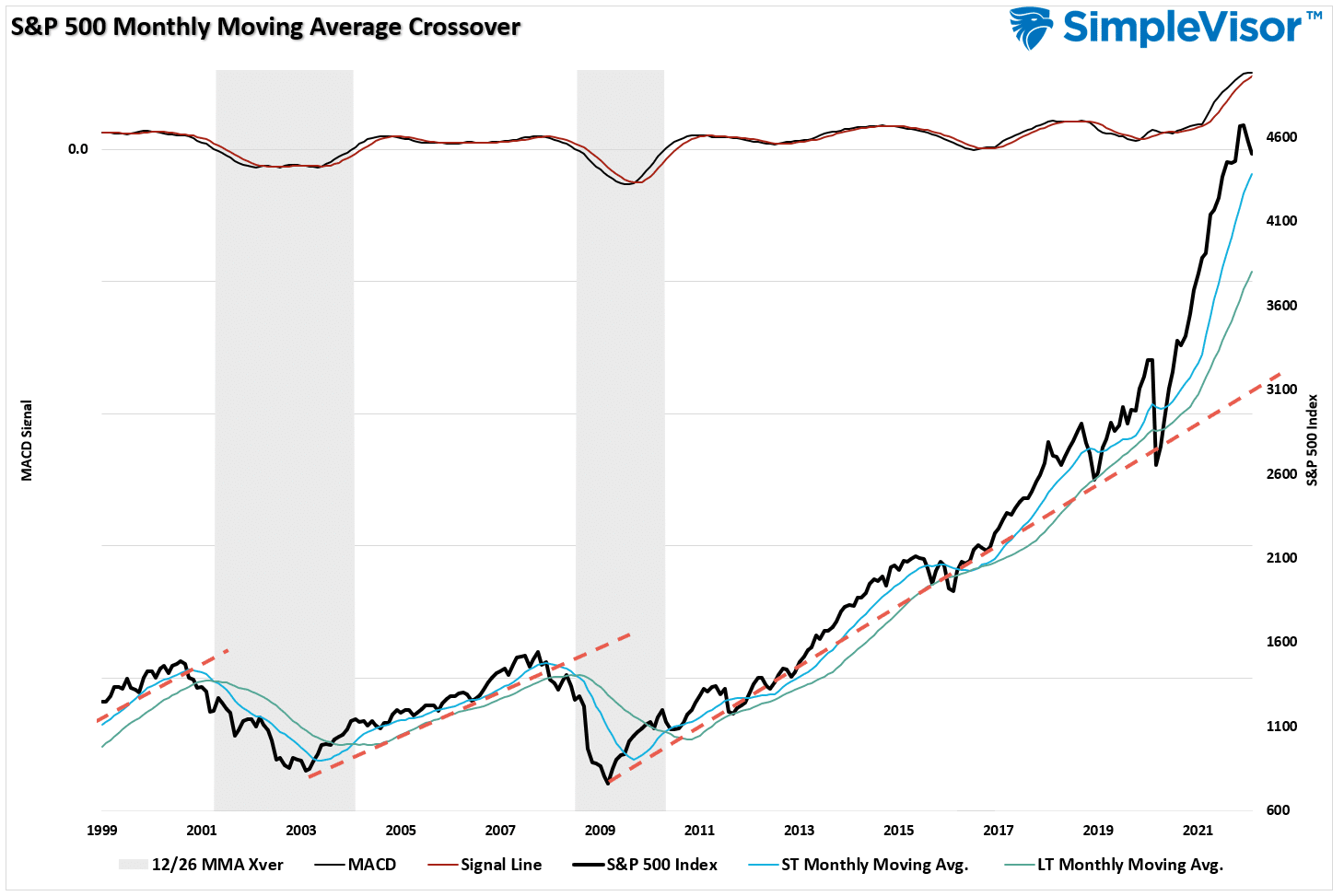

Notably, the many tailwinds that supported the rapid rise in the markets from 2020 to the present are reversing. As shown, the roughly 120% advance from the March lows should not be surprising given the massive liquidity surge from the Government.

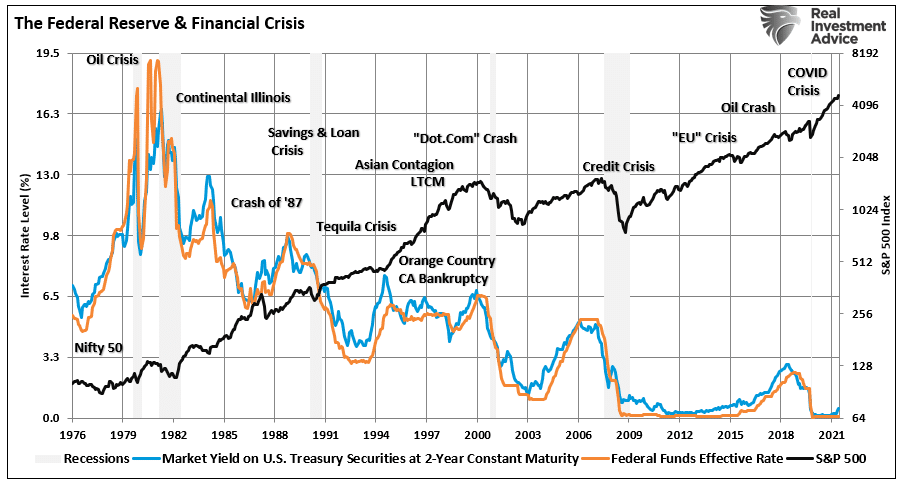

However, the most considerable risk to the markets remains the Fed.

Despite the recent correction, the markets remain convinced the Fed will hike a minimum of four times in 2022 and further in 2023. At the same time, the liquidity support from ongoing “Quantitative Easing” programs will reverse.

While investors hope the Fed will create a “soft landing” in the economy and markets, history clearly shows a track record of poor outcomes.

Every Bear Market Is The Same

The first few rate hikes typically do not disrupt markets. Such is because it takes roughly 9-months for changes to monetary policy to filter into the economy.

The mistake that investors make is assuming that since the first couple of rate hikes didn’t crash the market, “this time is different.”

As noted, with the markets negatively positioned, the markets may seem to “ignore” initial rate hikes. However, they likely won’t ignore tighter policy for very long.

Every bear market in history has an initial decline, a reflexive rally, then a protracted decline which reverts market excesses. Investors never know where they are in the process until the rally’s completion from the initial fall.

The deviation of the market due to Fed stimulus was so extended above long-term trends in March 2020 the depth of that “correction” was not surprising.

Given that the current deviation dwarfs all others, the following “bear market” will likely be equally deep.

As we concluded this past weekend’s newsletter:

“If you didn’t like the decline in the market in January and February, we suggest using any rally [in March] towards the 200- and 50-day moving averages to further reduce risk and rebalance allocations.”

The financial markets will do one of two things to your future financial security:

- If you treat the financial markets as a tool to adjust your current savings for inflation over time, the markets will KEEP you wealthy.

- However, if you try and use the markets to MAKE you wealthy, your capital will shift to those in the first category.

Ample warning signs suggest the risks of having excessive equity exposure to the market outweigh the potential for reward.

At least for now.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read