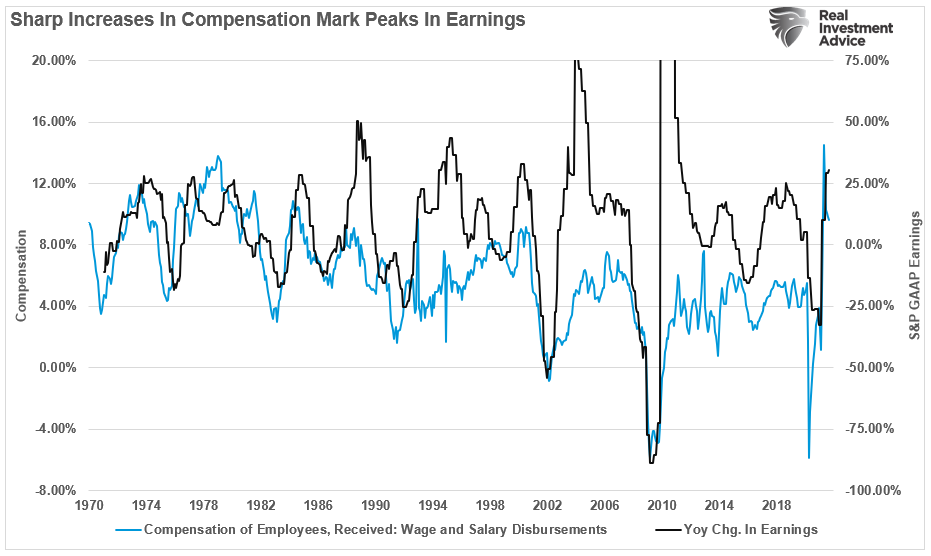

One of the biggest risks to the bull market currently is rising wages which are a threat to corporate earnings.

As shown in the chart below, courtesy of @themarketear, inflows into U.S. equities have been the strongest ever witnessed on record, Given the $120 billion a month being poured into the financial system by the Fed, that liquidity had to go somewhere.

Of course, the flood of capital into equities is not surprising; given that stocks are tracking the surging growth in earnings expectations from analysts.

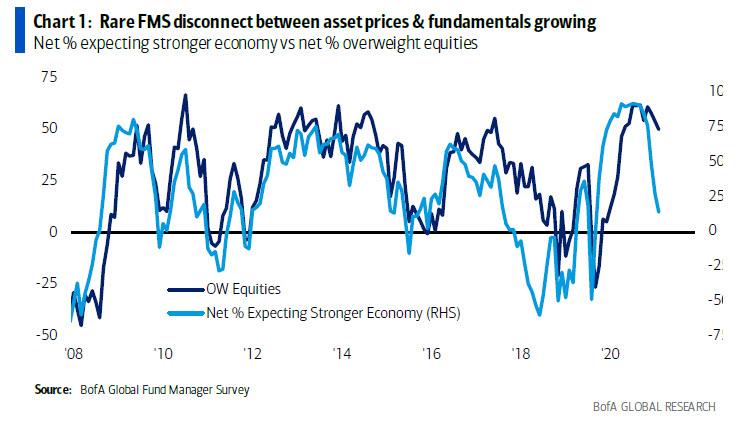

However, therein likes the biggest risk to the market and investors. Beyond the “tapering” of the Fed’s balance sheet, there is a rising disconnect between the market and underlying fundamentals. As noted by Zerohedge recently:

“Chief Investment Strategist Michael Hartnett who notes that a “rare FMS disconnect between asset prices & fundamentals growing” whereby a net 50% long stocks vs 20-year average of 29%; while net 69% short bonds (vs 43% avg) even as global growth expectations have continued to plunge, and in September, economic growth expectations are now just net 13%, the lowest since April 20 and down from the 91% peak in March 21. This is notable because as Hartnett points out, “global growth expectations have historically led FMS investor equity allocation but equity allocation has lagged this cycle.” In other words, any last connection between stocks and the underlying economy has now been irrevocably torn.”

Most importantly, however, given the earnings expansion is the primary justification for over-valuation. Those margins are set to shrink markedly in the months ahead.

Interestingly, the very thing people want more of is one of the drivers of collapsing margins.

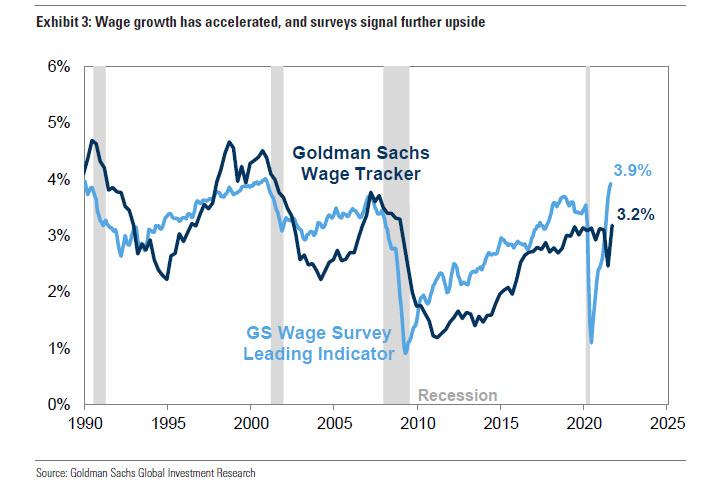

Surging Wages A Threat To Corporate Profits

As Goldman Sachs recently noted:

“Strong recent wage growth affirms the message from management commentary, and forward-looking survey data suggest wage growth will continue to accelerate in coming months.””

Rising wages are a “double-edged sword.” For workers, rising wages mean more income to spend. For employers, labor is the single largest expense for any business. Therefore, when wages increase, corporate profit margins will contract unless product demand increases.

In an environment where economic growth is accelerating and driven by increasing consumption rates, higher wages can be offset by higher revenue. However, when wages are rising at a slower rate than the rate of inflation, consumption is curtailed. This leads to weaker economic growth and collapsing margins. Such is the case we are witnessing currently.

As noted in our “Daily Market Commentary” (subscribe for free email delivery):

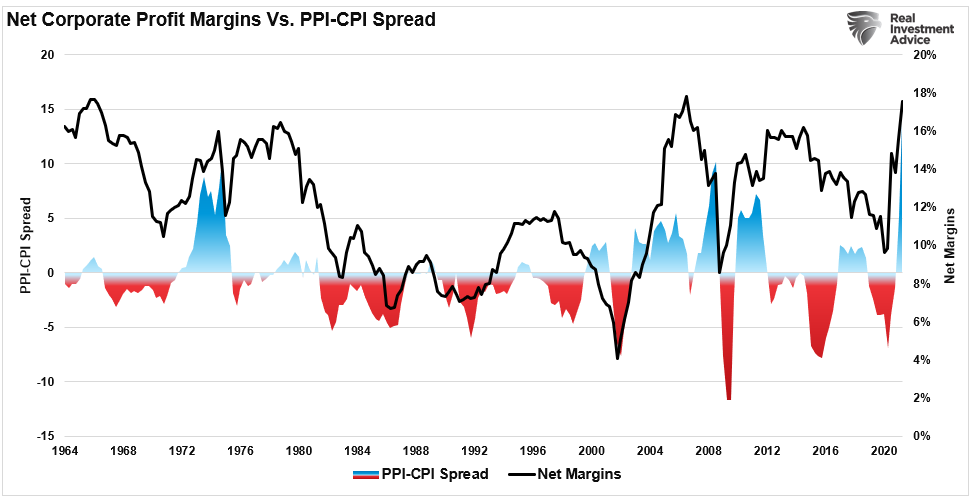

“Inflation is becoming problematic for the Fed mainly if these pressures are not as ‘transient’ as hoped. Higher wages are corrosive to both earnings and margins. As shown below, strongly rising producer prices are initially good for profit margins until inflation can not get passed along to consumers. Such is the case currently, with the most significant historical spread between PPI and CPI.“

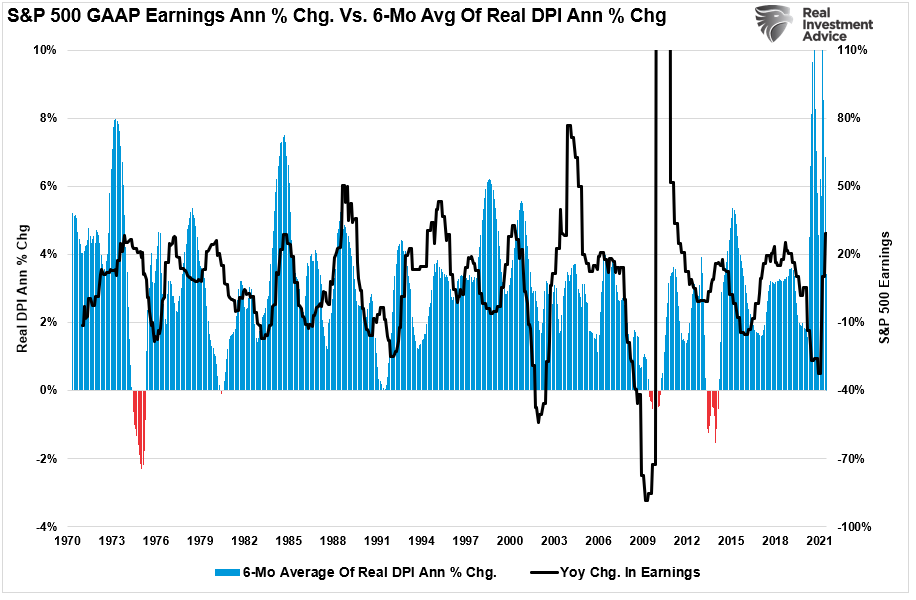

It is worth noting that when wages rise to a certain level, becoming corrosive to margins, such normally precedes a reversion in corporate earnings.

If we are currently witnessing a “peak” in corporate earnings, due to slower economic growth and inflation, investors are at risk of a reversion in overly valued markets.

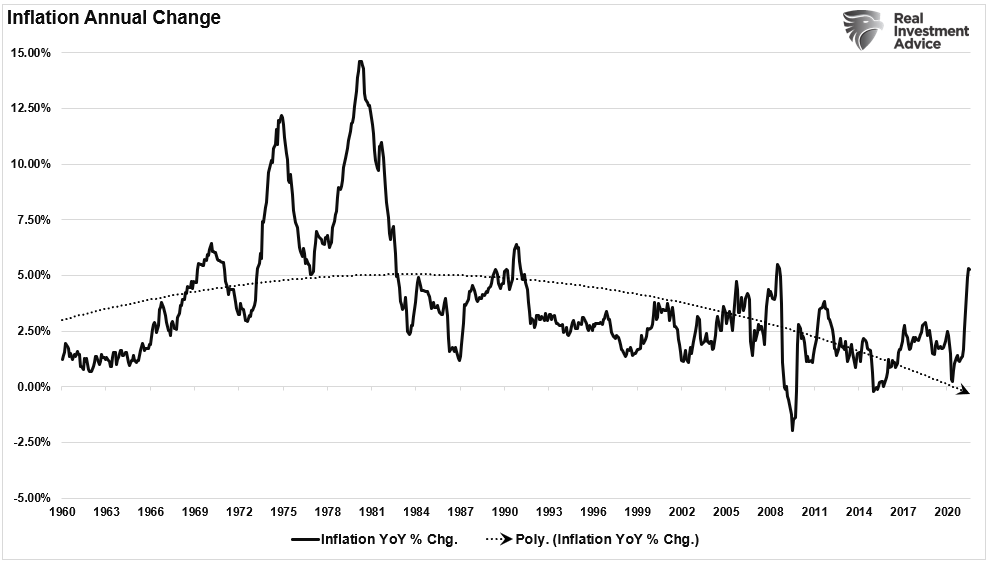

Inflation Makes The Difference

As noted, the key issue for consumers is inflation. If wages are rising commensurate with inflation, then economic growth can be sustained. (Remember 70% of GDP is based solely on consumption.) However, if inflation is rising faster than wages, then consumption will decline; as consumers have less money to spend in the economy. Currently, inflation, for consumers is problematic.

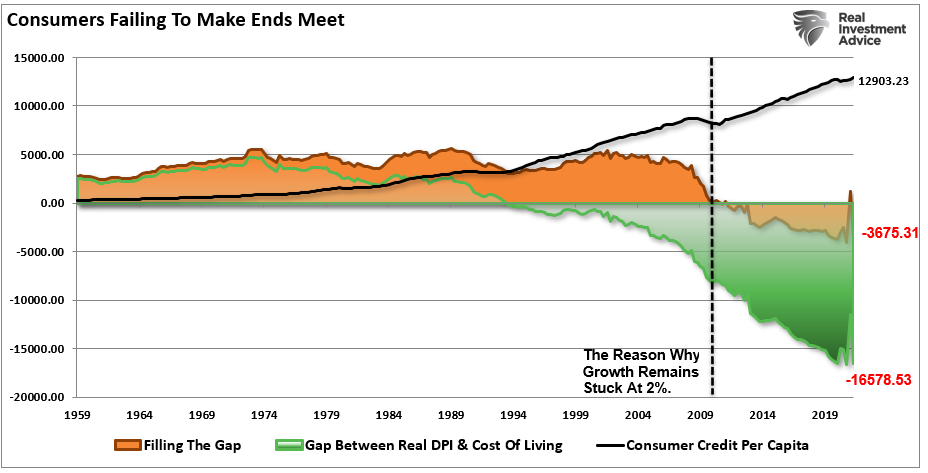

Such is why, despite the headlines of rising wages, the gap between spending and incomes continues to require debt. That debt need is not for the expansion of the living standard, but just to maintain it.

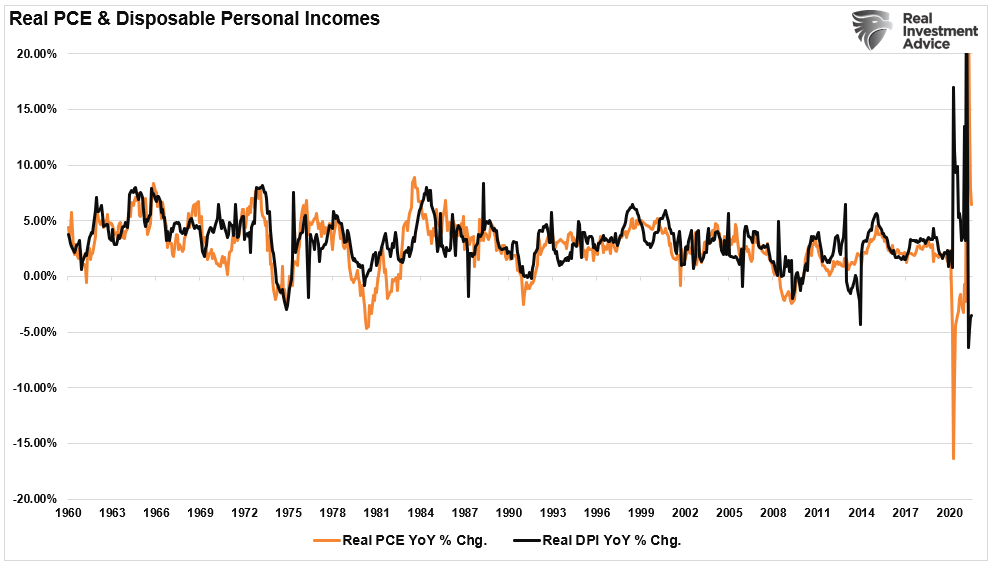

Wages, Disposable Incomes, & Inflation

Not surprisingly, there is a correlation between inflation-adjusted wages and disposable incomes (DPI). As shown, while the annual rate of change in wages recently peaked and started to decline, disposable incomes collapsed into negative territory as previous stimulus payments evaporate.

Logically, if inflation is rising faster than wages, and the artificial support of stimulus payments continues to fade, the decline in DPI will lead to a decline in personal consumption expenditures (PCE)

Therefore, the same relationship exists between inflation-adjusted wages and PCE.

As noted, the biggest risk to investors is that inflation is not transient. Such would erode both consumption and corporate margins leaving already overvalued assets even more overvalued.

Earnings At Risk Of Markdowns

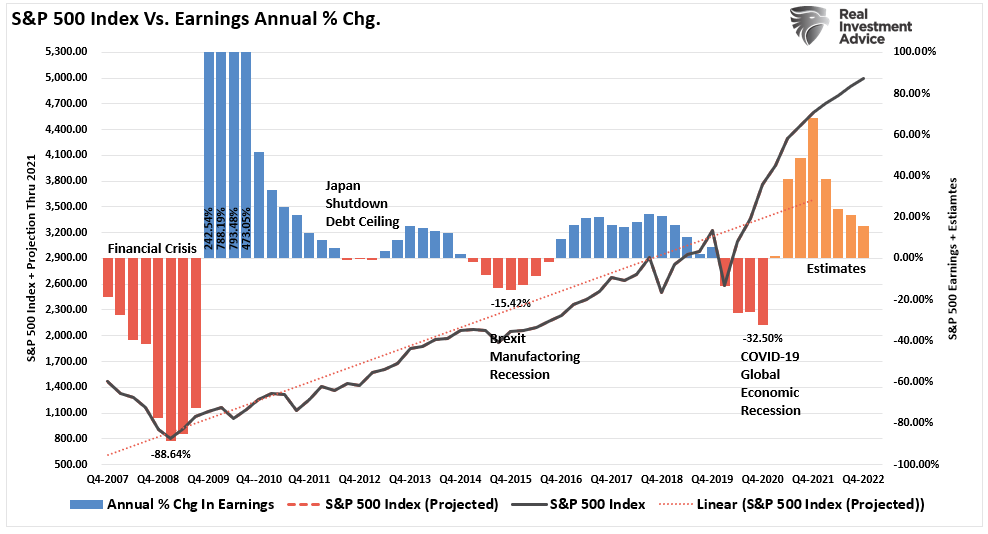

Given that corporate earnings and profits are derived ultimately from economic activity (personal consumption and business investment), it is unlikely the currently lofty expectations will get met.

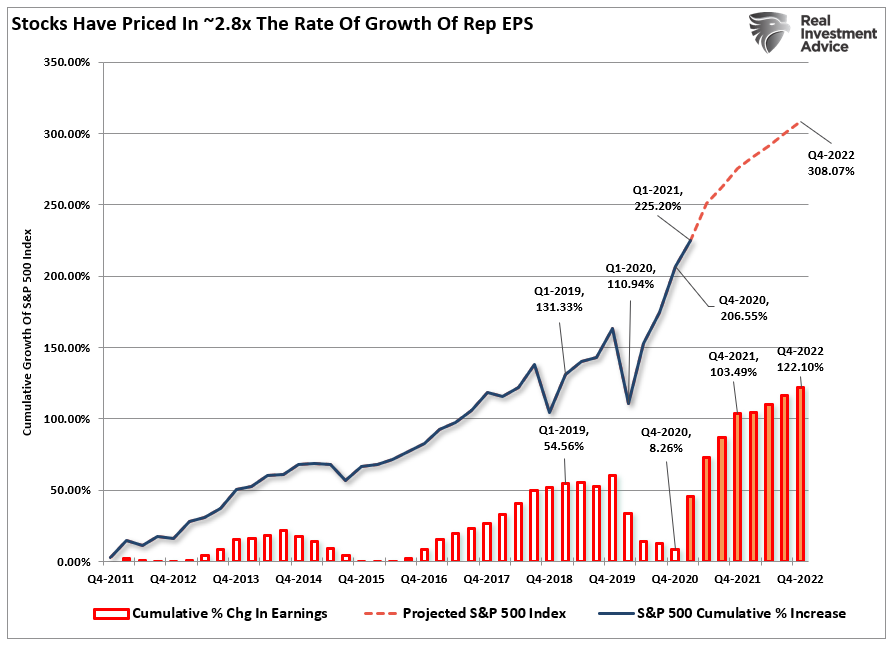

The problem for investors currently. Analysts’ assumptions are always high, and markets are trading at more extreme valuations, which leaves much room for disappointment. Using analyst’s price target assumptions of 4700 for 2020 and current earnings expectations, the S&P is trading 2.6x earnings growth.

That also puts the S&P 500 grossly above its linear trend line as earnings growth begins to revert.

Given that disposable personal incomes are declining, there is more than a reasonable expectation that revenues (the top line) will weaken. This will ultimately impact earnings (the bottom line).

While accounting gimmicks, share repurchases, and labor suppression (read: automation) can increase earnings per share in the short-term, eventually weaker revenue growth will matter.

Through the end of this year and into 2022, companies will guide down earnings estimates for a variety of reasons:

- Economic growth won’t be as robust as anticipated.

- Potentially higher corporate tax rates could reduce earnings.

- The increased input costs due to the supply-chain disruptions can’t get passed on to consumers.

- Higher interest rates increasing borrowing costs which impact earnings.

- A weaker consumer than currently expected due to wages not keeping up with inflation.

- Global demand weakens due to a stronger dollar impacting exports.

Any of these issues will result in investors once again “overpaying” for earnings growth that fails to materialize.

Of course, valuations become even more problematic if the Fed does begin to “taper” their balance sheet.

After a very long stretch of a “low volatility” market advance, investors should brace for a period of “high volatility.” A disappointment in earnings growth and profit margins will likely do the trick.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read