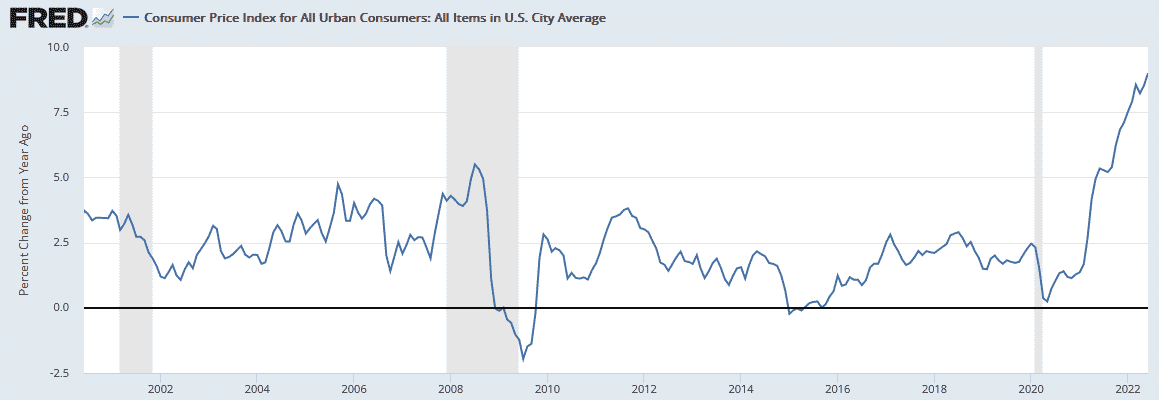

Fed pivot? Zero Hedge shared a Bloomberg article yesterday titled “If The Fed Pivots Sooner Than Most Think, The Second Half Of 2022 Risk Rally Will Be Enormous.” Forecasting a Fed pivot brings back FOMO emotions in investors. It reminds them of the amazing buy-the-dip opportunities over the last 20 years. All of which were ignited by a dovish Fed. It’s possible a Fed pivot could again drive an “enormous” rally in stocks, but would it be sustainable?

Over the last 30 years, the Fed had carte blanche to support asset prices and juice the economy at will. Simply inflation was not a concern. Therefore the consequences of running very easy monetary policy and making the “buy the dip” mentality dependable were negligible. Today inflation is the Fed’s overwhelming concern. If the Fed pivots before inflation is tamed, bond, commodity, and currency markets may likely revolt. If the Fed pivots too soon, yields may surge higher, resulting in sharp monetary tightening of the markets and economy. Further, commodity markets may regain their speculative enthusiasm, and the dollar could dump. A Fed pivot and rally may occur, but can it sustain itself with higher interest rates and commodity prices alongside lacking investor confidence? This time is different.

What To Watch Today

Economy

- 8:30 a.m. ET: Philadelphia Fed Business Outlook Index, July (-1.0 expected, -3.3 prior)

- 8:30 a.m. ET: Initial jobless claims, week ended July 16 (240,000 expected, 244,000 prior)

- 8:30 a.m. ET: Continuing claims, week ended July 9 (1.345 million expected, 1.331 prior)

- 10:00 a.m. ET: Leading Index, June (-0.5% expected, -0.4% prior)

Earnings

Pre-market

- AT&T (T), Travelers (TRV), D.R. Horton (DHI), Blackstone (BX), Union Pacific (UNP), American Airlines (AAL), Dow (DOW), Nokia (NOK), Danaher (DHR), Fifth Third Bancorp (FITB), Tractor Supply (TSCO), Marsh McLennan (MMC), Interpublic (IPG)

Post-market

- Snap (SNAP), Mattel (MAT), PPG Industries (PPG), Domino’s (DPZ), Tenet Healthcare (THC), Boston Beer (SAM)

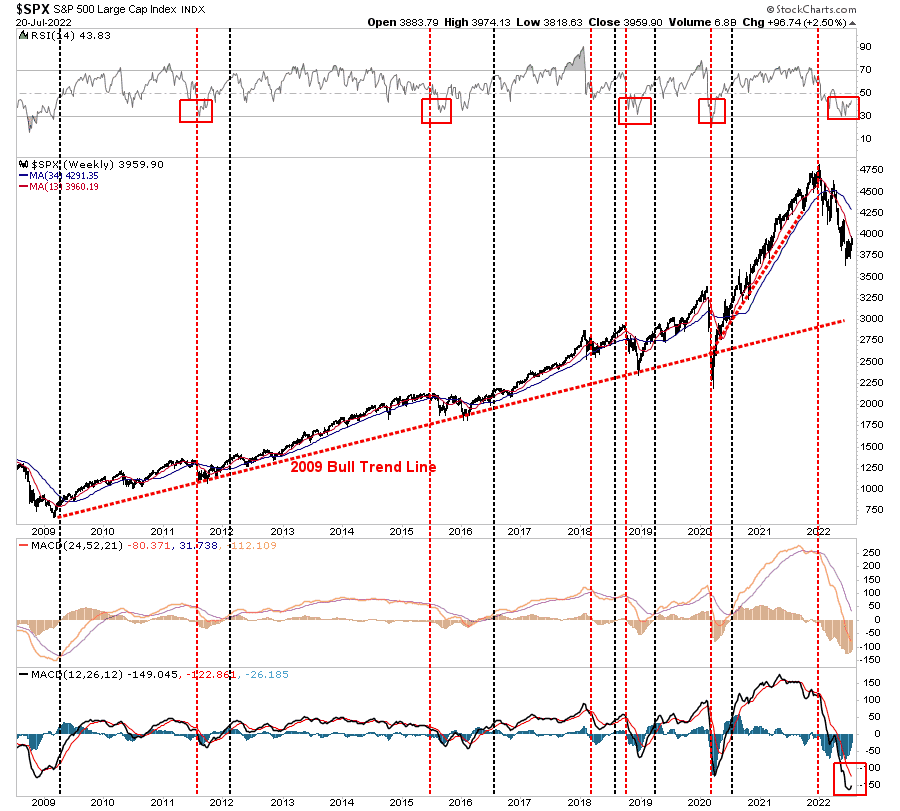

Market Trading Update – Rally Continues

The market continued its rally on Tuesday, clearing the 50-dma for now. Some of that rally is short-covering. The other part is the hope of a Fed pivot sooner than later. With negative sentiment high, there is plenty of fuel for a further rally. Furthermore, as we discussed in yesterday’s 3-minutes video, we are very close to triggering a longer-term MACD buy signal on a weekly basis, as shown below.

This time, the difference is that previous bottoms of the market didn’t coincide with nearly 9% inflation. There is a risk the Fed pivot may not come, and there is more downside risk. We continue to suggest trading cautiously, but the bulls do seem to have the upper hand at the moment.

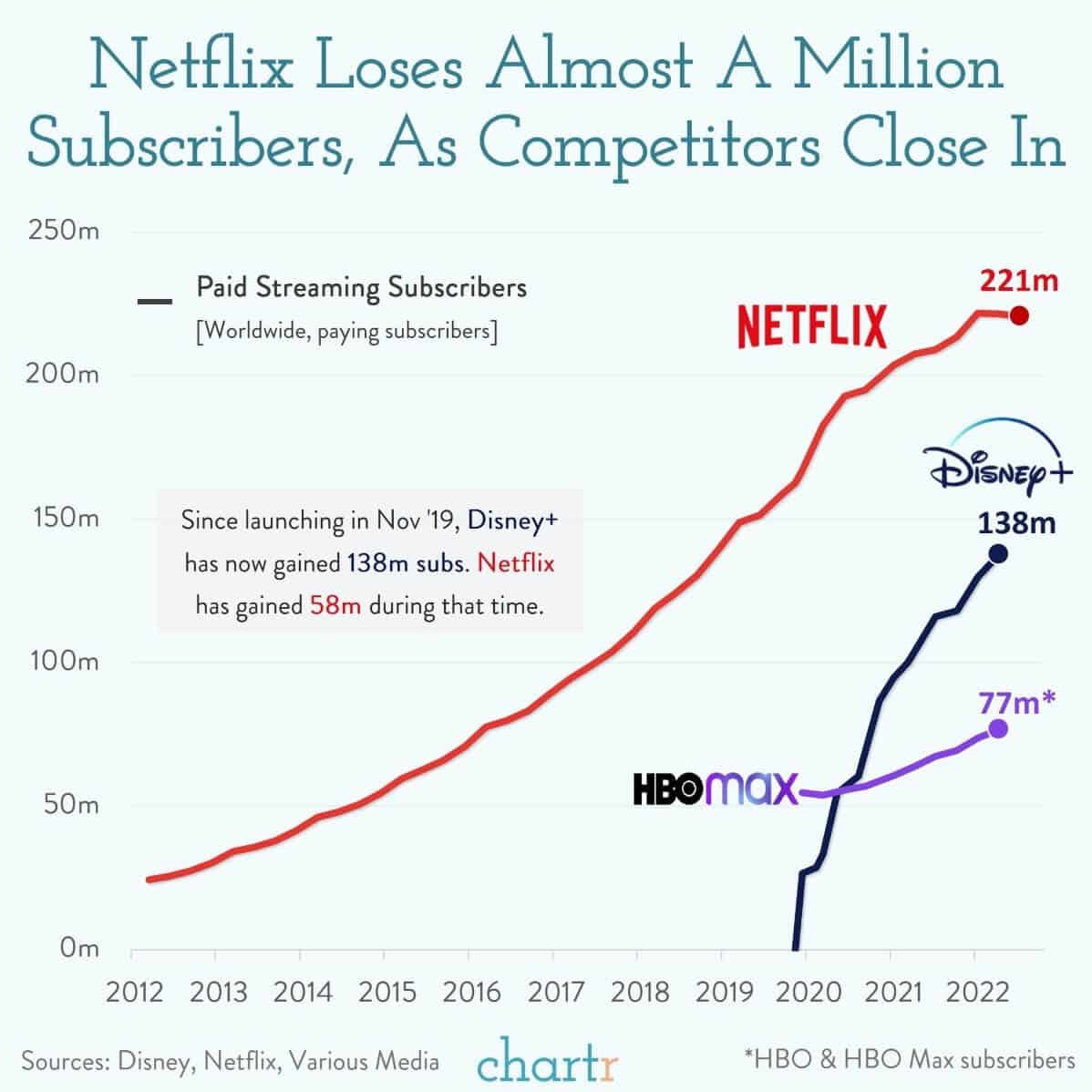

Netflix Loses Almost A Million Subscribers

“Almost a million people decided that their lives, and their wallets, would be better off without a Netflix subscription in the last 3 months, as the streaming service reported a second consecutive quarter of falling subscriber numbers.

Losing 970,000 subscribers was hardly a success for Netflix, but it was better than the 2 million that they’d expected to lose — which is why the company’s share price gained almost 6% yesterday amidst a broader stock market rise. CEO Reed Hastings lauded the performance of the global smash hit Stranger Things as a particular bright spot, and the company anticipates a turnaround in Q3, with expectations for a gain of 1 million subscribers.

The news means that Disney, which will give us an update on its Disney+ numbers in around 3 weeks, is likely to continue gaining on Netflix’s early streaming lead. Netflix’s hopes to stay out in front of its competition are mainly pinned to the success of its new ad-supported tier, developed in partnership with Microsoft, which is expected to launch in early 2023. The other lever that the company has pulled is its ongoing crackdown on password sharing — this week, they announced that an “extra home” fee would be added to some customer accounts in certain countries. Netflix and not so chill.” – Chartr

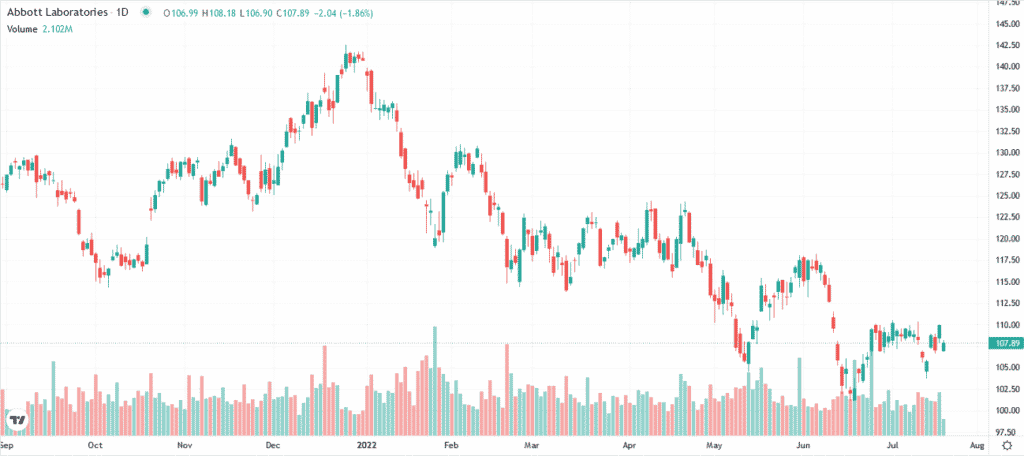

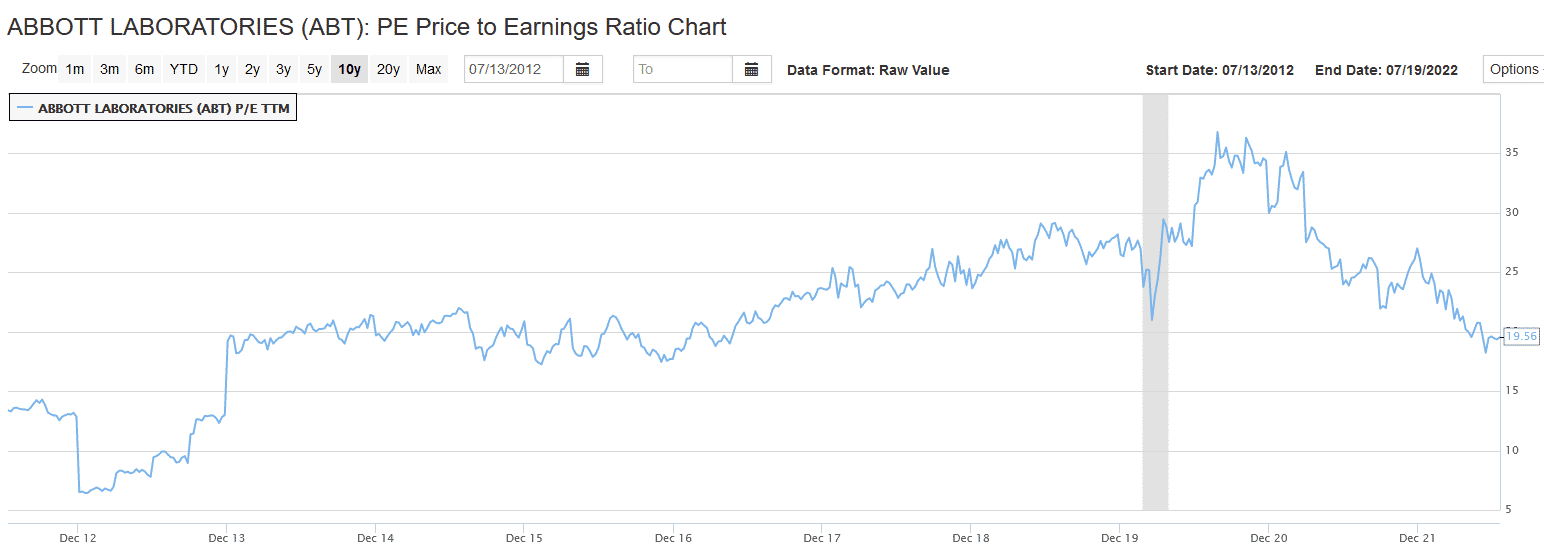

Abbot Labs Beat Expectations But Its Stock Falls

Abbot Labs (ABT) easily beat earnings forecasts, earning $1.43 per share versus expectations of $1.10. Sales also beat estimates by 10%, or nearly $1 billion. The company raised its earnings guidance for the year. Helping boost its performance, ABT shipped as many covid tests in the first six months of 2022 as they did in all of 2021. The only negatives we uncovered are the unfavorable impact of the stronger dollar and the change in guidance, while higher, was below what many analysts thought it would be. The first graph shows that ABT is down about 25% this year. The second graph shows that its P/E at 19.5 is well off late 2020 highs and back at the low end of its 10-year range.

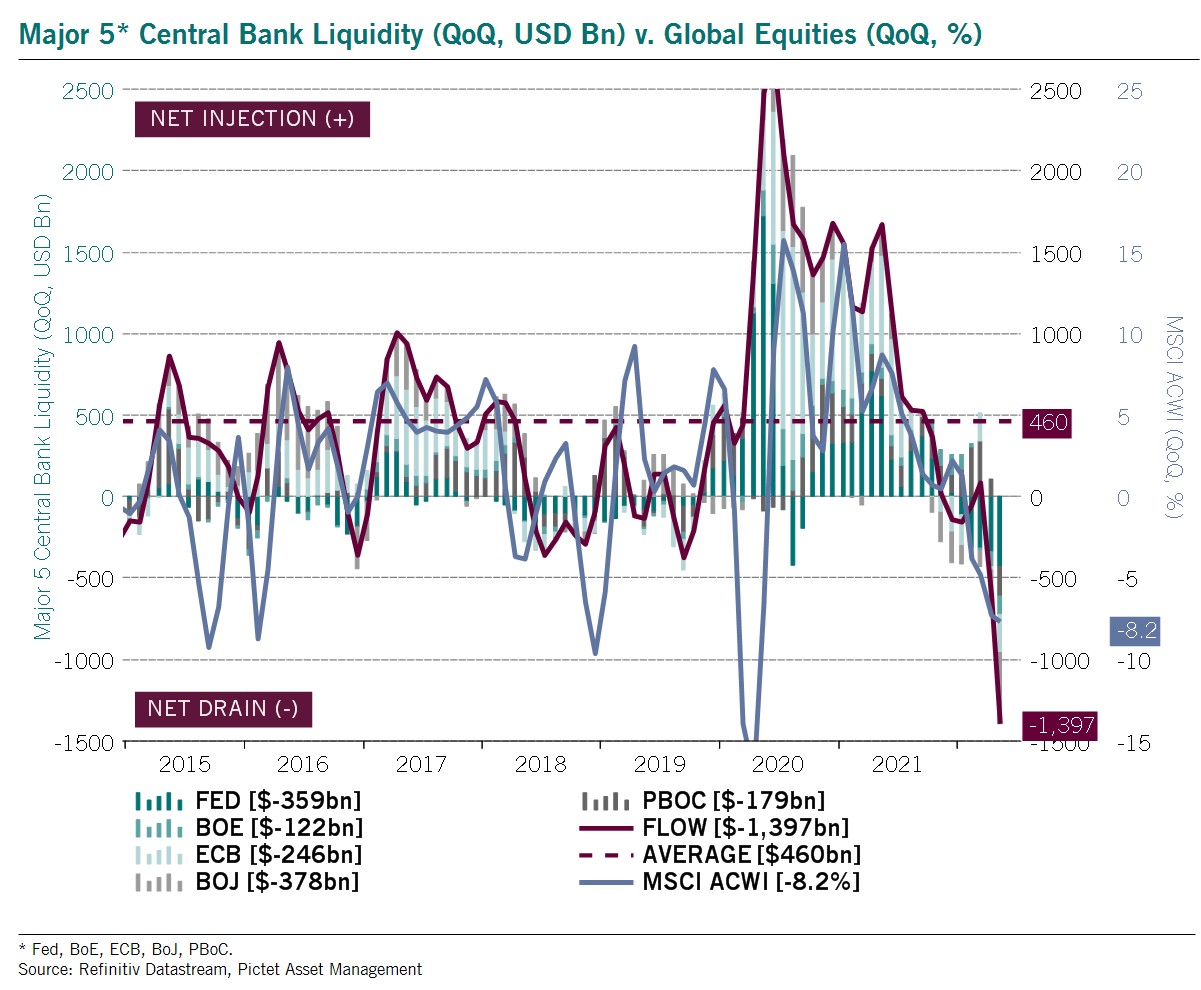

It’s All About Liquidity

The graph below expands on the four domestic liquidity graphs we shared yesterday. As we discussed, the Fed and Treasury are draining liquidity from the system. The Pictet Asset Management graph expands on the analysis, showing the strong correlation between global liquidity furnished by the world’s five major central banks and the MSCI global equity index. The current global quarterly liquidity drain is $1.397bn. Given high rates of inflation around the world and the actions of most central banks, we suspect liquidity will continue to fall. The graph only furthers our longer-term thoughts that Fed tightening will be a big headwind for markets. As we recently wrote in Liquidity and Valuations- The Cornerstones of Investing:

Current liquidity conditions dictate conservatism. The Fed is aggressively raising interest rates and reducing its balance sheet. Further, fiscal spending is falling well short of that in the prior two years. As a result, liquidity is exiting the financial markets, which augurs a bearish trend.

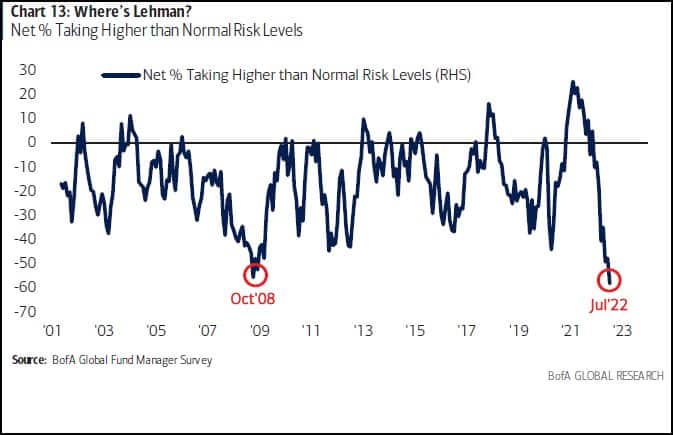

Is Market Bracing for a Lehman Moment?

Liz Young (@lizyoungstrat) from SoFi writes the following about the graph below:

BofA’s Fund Manager Survey indicates more risk-off positioning now than in the midst of the global financial crisis. Is inflation scarier than what happened in 2008? No right or wrong answer, but this would suggest it is.

There are a couple of things worth considering in her statement. The graph just shows that institutional investors are not taking “higher than normal” amounts of risk. The 60+% that are not taking higher than normal risk may just be taking average amounts of risk. She also assumes risk tolerance is down because of inflation. Might it not be inflation risks but recession risks? As we will share in a forthcoming article, specific sectors’ price performance strongly signals that recession risks are now a more significant concern for investors than inflation.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read