Today we will get the latest reading on inflation as the Fed tapering QE in November seems to be a foregone conclusion by the markets. At this point, today’s CPI report, tomorrow’s PPI release, and other inflation data, along with continuing improvement in the labor markets are key factors for investors to watch. It is these economic stats that will help guide the Fed’s pace of reducing QE. JOLTS information, discussed below, provides more evidence the labor market is healing nicely.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Oct. 8 (-6.9% during prior week)

- 8:30 a.m. ET: Consumer price index, month-over-month, September (0.3% expected, 0.3% during prior month)

- 8:30 a.m. ET: CPI excluding food and energy, month-over-month, September (0.2% expected, 0.1% during prior month)

- 8:30 a.m. ET: CPI year-over-year, September (5.3% expected, 5.3% during prior month)

- 8:30 a.m. ET: CPI excluding food and energy, year-over-year, September (4.0% expected, 4.0% during prior month)

- 8:30 a.m. ET: Real Average Hourly earnings, year-over-year, September (-1.1% during prior month)

- 8:30 a.m. ET: Real Average Weekly earnings, year-over-year, September (-1.4% during prior month)

- 2:00 p.m. ET: FOMC meeting minutes

Earnings

- 6:15 a.m. ET: BlackRock (BLK) is expected to report adjusted earnings of $9.39 per share on revenue of $4.84 billion

- 7:00 a.m. ET: JPMorgan Chase (JPM) is expected to report adjusted earnings of $2.97 per share on revenue of $29.86 billion

- 7:00 a.m. ET: First Republic Bank (FRC) is expected to report adjusted earnings of $1.84 per share on revenue of $1.27 billion

- 8:25 a.m. ET: Delta Air Lines (DAL) is expected to report adjusted earnings of 17 cents per share on revenue of $8.45 billion

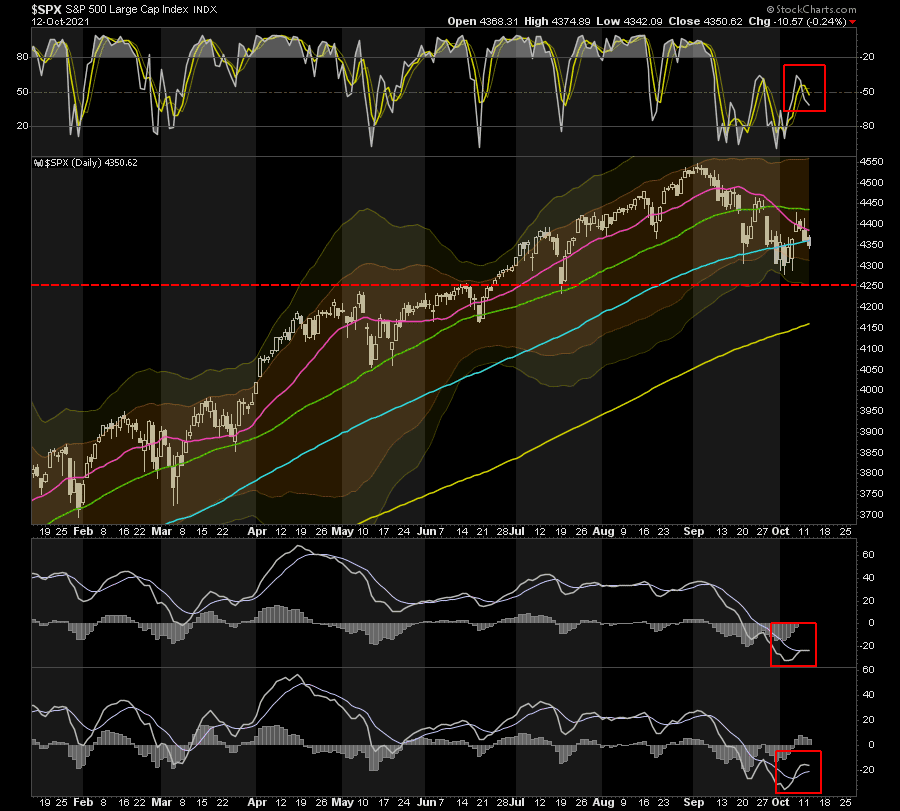

Market Loses Support Yesterday On Weak Trading

Yesterday, the market traded sloppily all day eventually losing the support at the 100-dma. Such keeps the market at risk of a retest of recent lows. As noted yesterday, with weekly and monthly “sell signals” in place, a longer, and potentially deeper, correction period is possible.

If the market is going to maintain its bullish bias, it needs to hold support at the recent lows and rally back above current resistance by next week. A failure to do so, and we will likely see the recent lows taken out and a test of the 200-dma becomes a high probability event.

Some caution is advised until we get through “options expiration” this Friday.

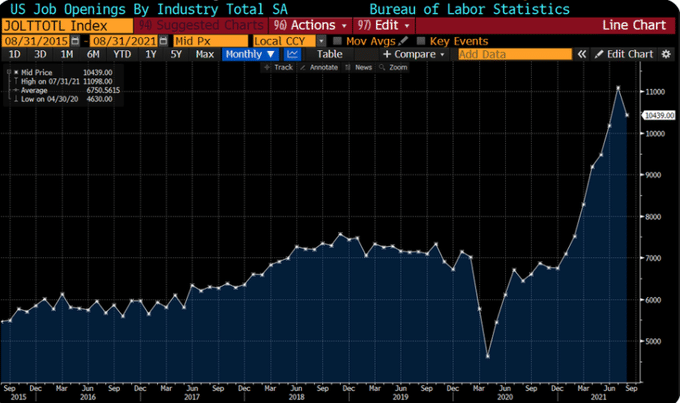

JOLTs

Per the JOLTs report, the number of job openings fell for the first time since April. The number of openings in August was 10.43 million versus expectations of over 11 million. This may be a signal the labor market is getting better, or at least less bad, at matching workers with openings. The quits rate rose to a record 2.9% of the workforce. Typically workers quit jobs when they have confidence in finding a better, higher-paying job. Prior to Covid, the quit rate was around 2.2%.

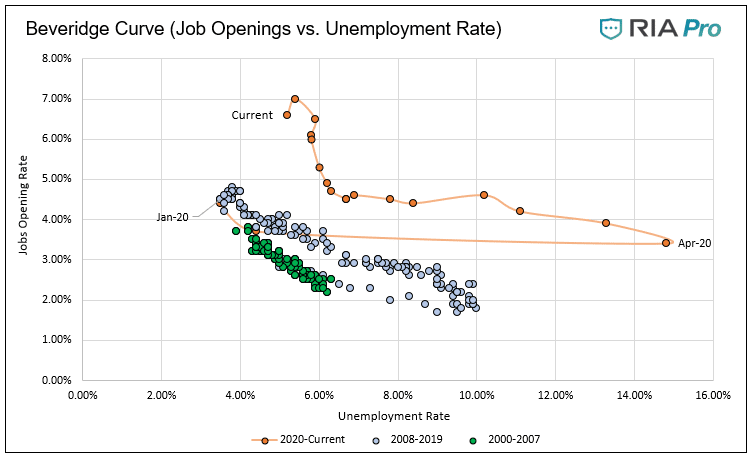

As shown below the number of openings is still well above normal levels. The second graph below, the Beveridge Curve, highlights the anomaly. At the current unemployment rate of 5.2%, we should expect a job openings rate of about half of what it is. The million-dollar question is whether employers truly have as many job openings as advertised or are there too many unemployed workers either not trained for certain jobs or not willing to accept offered wages.

Can Markets Maintain Support?

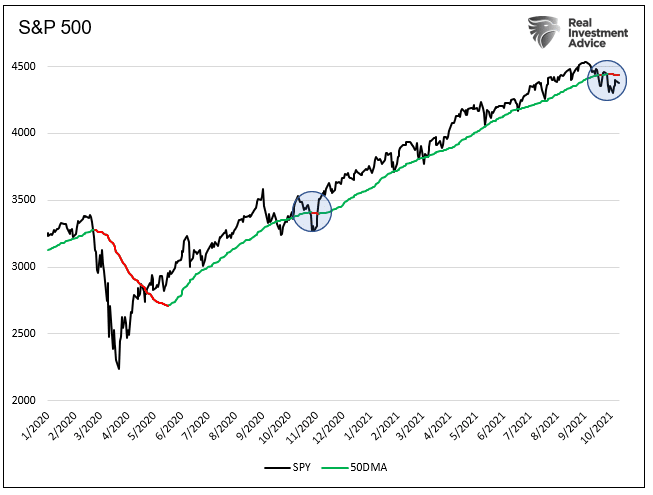

Is The 50DMA Trying To Tell Us Something?

As we show below circled in red, the 50dma is turning lower for only the second time since the market rebounded in April of 2020. In late October and early November of last year, the 50dma turned lower for six days on a relatively steep 7.5% decline. The current market decline causing the 50dma to fall is only a 4% decline but its duration is almost twice as long as the prior one.

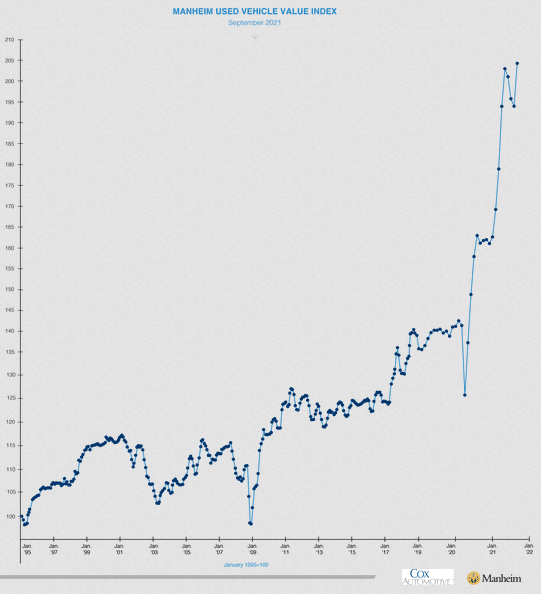

Used Car Prices En Fuego

After a brief rest bit, used car prices rose again in September back to all-time highs as shown in the Manheim Used Vehicle Value Index below. The accompanying report notes: “According to Cox Automotive estimates, total used vehicle sales were down 13% year-over-year in September.” Prices rising with sales falling clearly points to a lack of supply.

Per the report: “Using a rolling seven-day estimate of used retail days’ supply based on vAuto data, we see that used retail supply peaked at 114 days on April 8, 2020. Normal used retail supply is about 44 days’ supply. It ended September at 37 days, which is below normal levels. We estimate that wholesale supply peaked at 149 days on April 9, 2020, when normal supply is 23. It ended September at 18 days.”

Also Read