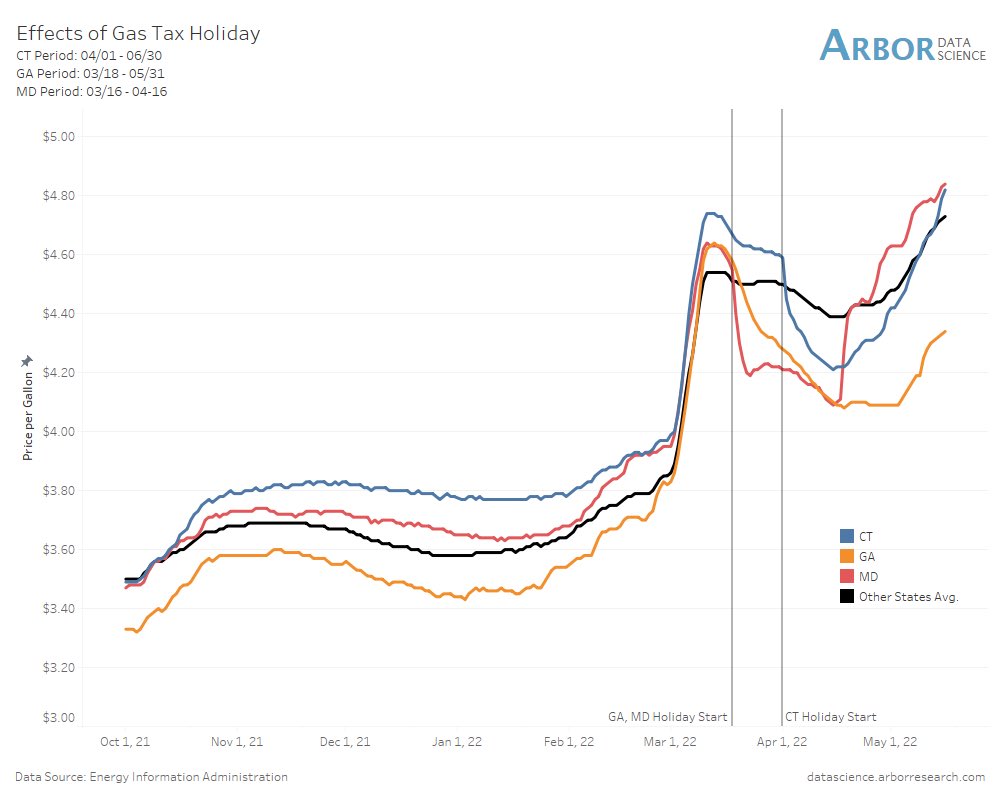

As we roll into the Fourth of July holiday, we thought we would discuss another type of holiday. Connecticut, Georgia, and Maryland implemented state tax holidays on gasoline sales to reduce gas prices. Other states are contemplating gas tax holidays or suspending taxes on food and other goods. Do they work?

The answer is yes, no, and maybe. The graph below shows the price of gas in the three aforementioned states before, during, and in the case of Maryland and Georgia, after the tax holiday. In all three states, prices fell more than the national average following the start of the gas tax holiday. While in effect in Maryland, gas prices were lower but they shot higher once it ended. In Connecticut, the plan worked for a while, but prices then rose sharply while still in the gas tax holiday. The jury is still out on Georgia. As you consider the data, its important to realize that tax holidays may bring prices down. However, they also create more demand on the margin. The net effect is not always the intended effect.

What To Watch Today

Economy

- S&P Global U.S. Manufacturing PMI, June final (52.4 expected, 52.4 prior)

- Construction Spending, month-over-month, May (0.4% expected, 0.2% prior)

- ISM Manufacturing, June (54.7 expected, 56.1 prior)

- ISM Prices Paid, June (80.0 expected, 82.2 prior)

- ISM New Orders, June (55.1 prior)

- ISM Employment, June (49.6 prior)

- Wards Total Vehicle Sales, June (13.40 million, 12.68 prior)

Earnings

- No notable companies are expected to report.

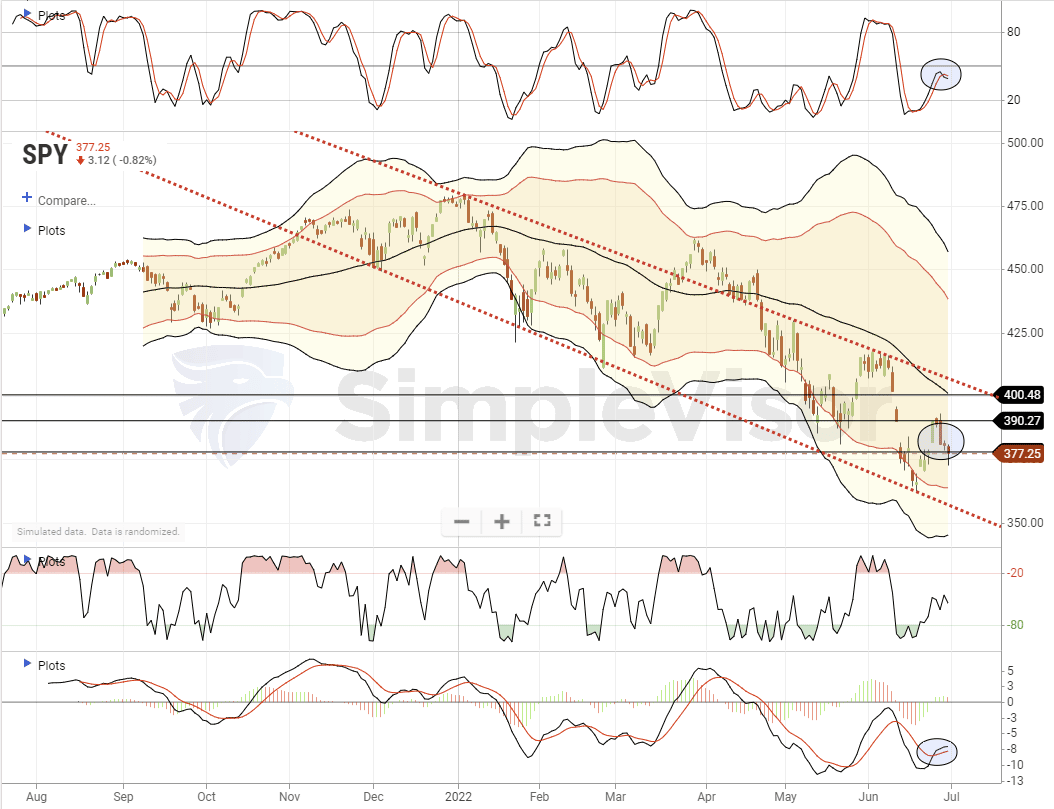

Market Trading Update – Markets Hold Support Again As Quarter Ends

Yesterday, as the end of the second quarter came to an end, stocks rallied mid-day but gave up the gains by the day’s end. However, the good news is the market is still holding onto the support, but just barely. With the market having been under more severe selling pressure over the last week, a rally for a day or two should not be surprising. Furthermore, July tends to be a stronger performance month before the seasonally weak months of August and September. We are keeping a close stop on positions but giving them a little wiggle room for the next couple of trading days.

Could We Have A Summer Rally?

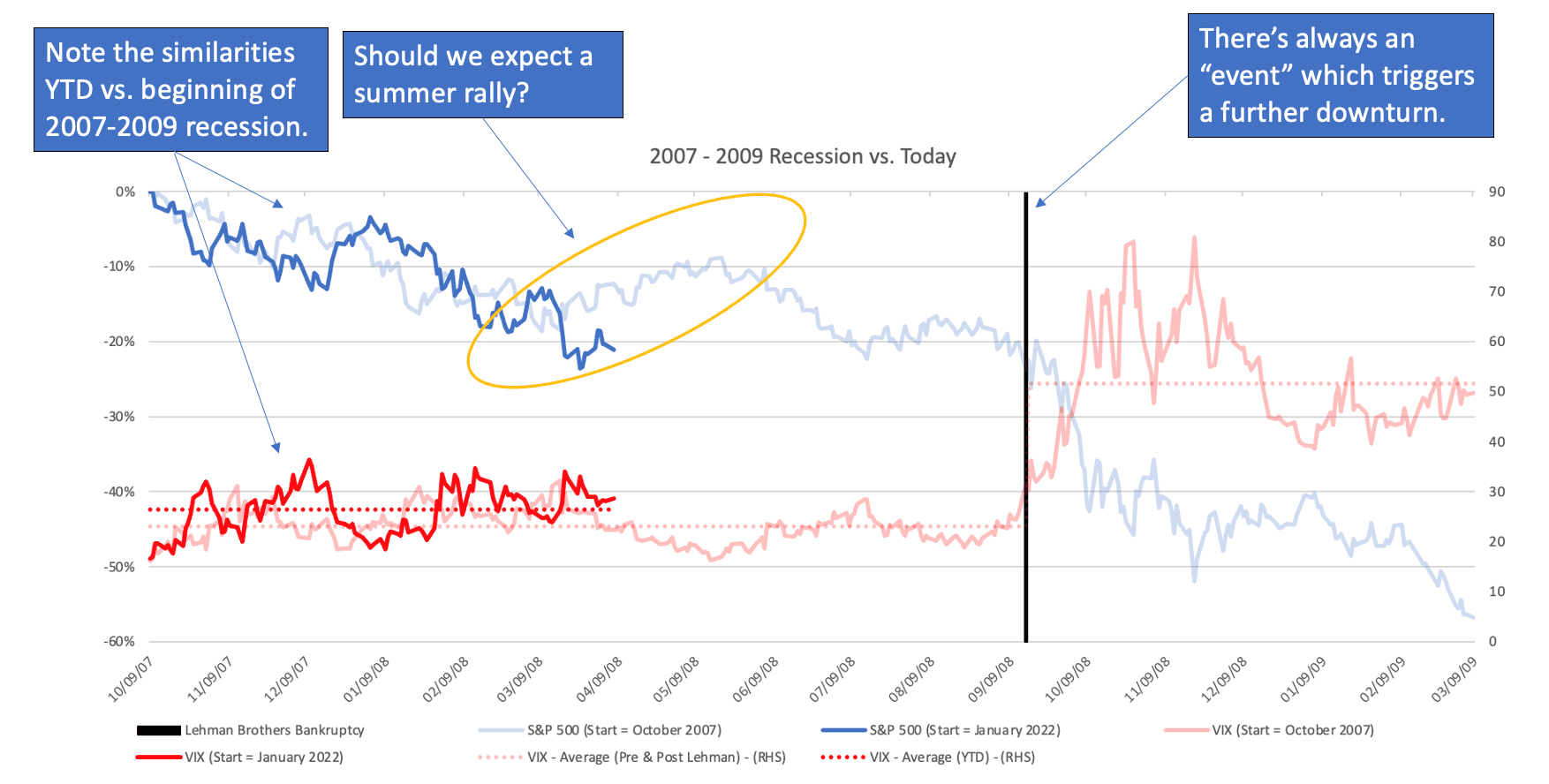

“The S&P 500 finished the first half of 2022 with a return of -20.6%. This is the worst first half of a year since 1970 when the S&P 500 fell by just over -21%. Interestingly, is the similarity between the first half of 2022 and the beginning of the 2007 – 2009 recession. The chart below shows the S&P 500 starting from the market peak on October 9, 2007 through the market bottom on March 9, 2009. We then compare this to how the S&P 500 has performed from the more recent market peak of January 3, 2022 through June 30, 2022. Note the similarities between how both the S&P 500 and VIX have performed YTD vs. the period beginning October 9, 2007.

On a positive note, if this analog continues to play out, it may be reasonable to expect a rally this summer. The circled area in the chart highlights the S&P 500 during the period from March 10, 2008 to May 19, 2008 when the market rallied by just over 12% over that two month period. Is it possible that the recent low on June 16, 2022 was the beginning of a “summertime rally”? It’s certainly possible and only time will tell.

We will end with a more cautionary note. If this analog does continue to play out, it would suggest that we may be in for a more difficult Fall and early 2023. Thus far, the YTD decline has been very orderly as evidenced by an average VIX value of 26.4. However, if we are moving directionally towards a recession in the US, history would suggest that there’s often an “event” which leads the market to capitulate.”

As the old saying goes: “An ounce of prevention is worth a pound of cure.” – Jim Colquit, Armor ETFs

PCE Consumption and Price Data

One of the most important data points for the Fed provided mixed news. PCE (consumption) rose by 0.2% versus 0.9% last month and expectations for a gain of 0.5%. Real, after inflation, consumption fell by 0.4%. Given personal consumption is about two-thirds of GDP, the data bodes poorly for economic growth.

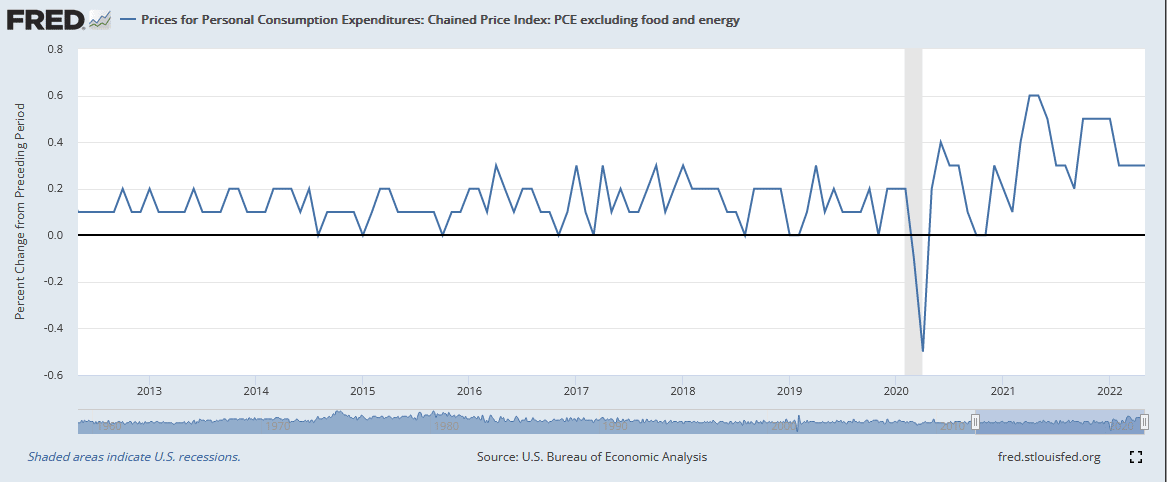

The good news is the Core PCE Price Index rose by 0.3%, lower than 0.4% expectations. Further, the year-over-year Core PCE figure fell from 4.9% to 4.7%. It was the third straight monthly decline. The Fed tends to rely heavily on this price series as they believe it more accurately tracks lasting inflation and strips out some of the more volatile components in other inflation figures. Shown below is the monthly change in Core PCE Prices. The monthly level has fallen from recent highs, but is still above the 0-.2% run rate existing before Covid.

Restoration Hardware Warns Again

In our Daily Commentary at the end of the first quarter, we shared the following news about Restoration Hardware (RH):

To this point, Restoration Hardware executives warn they have seen a 10-12% slowdown in demand over the past couple of weeks. Consider the following statement from its CEO- “Our business changed just a few weeks ago. We’re reporting later, so we are seeing the trends now. There’s been a broader slowdown in our industry, and it has to be in other industries too. I’d be surprised if others aren’t seeing the same thing. Maybe we’re the only ones?”

Once again, it is quarter-end, and RH is back with concerning news. On Wednesday, they updated their fiscal 2022 outlook. Their outlook continues to deteriorate. Keep in mind the prior forecast mentioned in the statement below was from June 2nd. Per CEO Gary Friedman:

“The deteriorating macro-economic environment has resulted in lower than expected demand since our prior forecast, and we are updating our outlook, particularly for the second half of the year.”

As we highlight below, RH stock, after rising twofold in 2020 and 2021, now sits below the pre-pandemic highs.

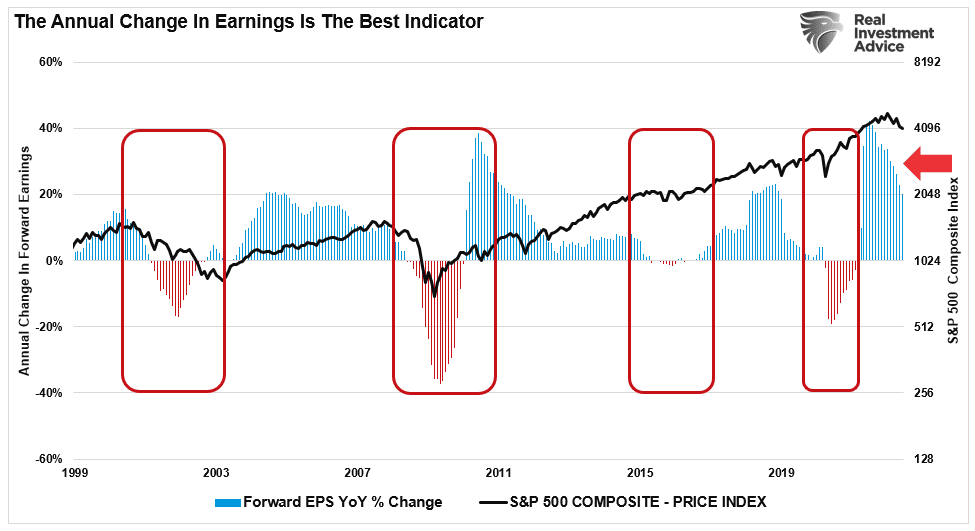

Earnings Are Still Overly Optimistic

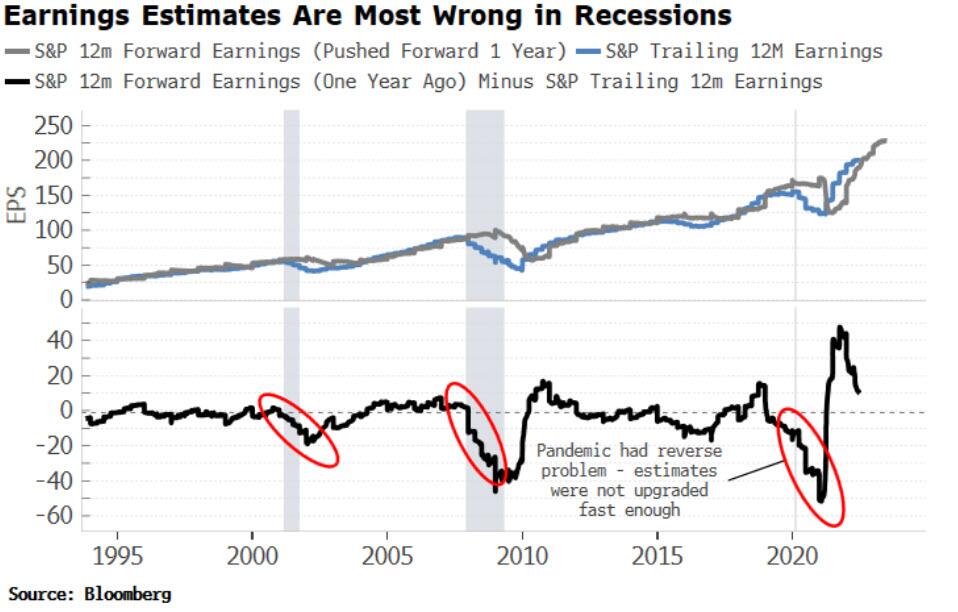

Currently, earnings estimates for stocks are not accounting for much slower economic activity. While the “P” in the valuations (P/E) calculation has declined, the “E” has not. During a recession, earnings tend to fall quite significantly, as noted by Bloomberg:

“Outside of recessions, the black line in the chart doesn’t stray too far from zero. But during recessions, we see that actual earnings are considerably worse than expected ones.“

This is a problem not only confined to equities. Economic data is typically wrong at major turning points such as recessions. Ironically, though, this is when you need the most clarity. As shown below, forward earnings for the S&P have fallen this year, but if the past is a guide, they are still likely to be too optimistic.

We Told You So

The following headline from a Jerome Powell speech hit the wires on Wednesday:

POWELL: WE UNDERSTAND BETTER HOW LITTLE WE UNDERSTAND INFLATION

Throughout 2021 speculative activities flourished, economic activity was brisk, and inflation was rising. Many including ourselves, warned that the Fed needs to quickly pull back on the monetary policy reins. Despite stimulus-driven demand and significant supply line problems, the Fed kept interest rates at zero and was buying $120 billion per month via QE. Had they understood inflation better, they may have also understood that they should have taken action earlier. The point in sharing this is not to belittle the Fed. Instead, we must realize the market is largely driven by confidence in the Fed and its actions. If investor confidence in the Fed wanes, the risk of market volatility increases.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read