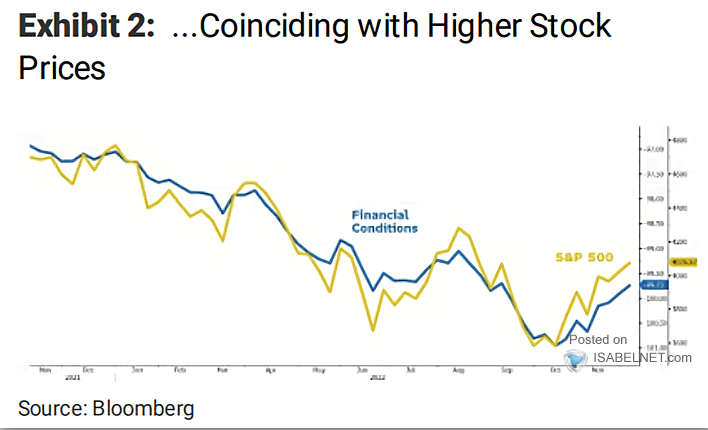

In Jerome Powell’s speech last week, which drove the markets 3% higher, he offered a warning that few investors picked up on. “Officials seek to reduce inflation by slowing the economy through tighter financial conditions—such as higher borrowing costs, lower stock prices, and a stronger dollar—which typically curb demand.” The graph below, courtesy of ISABEL.NET.com and Bloomberg, shows the strong correlation between financial conditions and the S&P 500. Powell’s speech, his last before next week’s Fed meeting, helped ease financial conditions via lower borrowing costs, higher stock prices, and a weaker dollar. We seriously doubt this was his intention. The Fed is in a media blackout period. Accordingly, as we noted in yesterday’s Commentary, they must resort to using WSJ reporter Nick Timiraos to speak for them. Not surprisingly, Timiraos said the Fed might be more aggressive than most investors expect.

The risk at next week’s meeting is a Fed determined to fight inflation via tighter financial conditions. Such includes using hawkish rhetoric to talk stock prices lower. Further, they likely want to erase a pivot out of investors’ forecasts for 2023. Will the markets price in the Fed’s desire for tighter financial conditions? Or will they look past Powell’s bluster and continue to dream of a mid-year pivot?

What To Watch Today

Economy

- MBA Mortgage Applications, the week ended Dec. 2 (-0.8% prior)

- Nonfarm Productivity, Q3 final (0.7% expected, 0.3% prior)

- Unit Labor Costs, Q3 final (3.0% expected, 3.5% prior)

- Consumer Credit, October ($28.000 billion expected, $24.976 prior)

Earnings

Market Trading Update

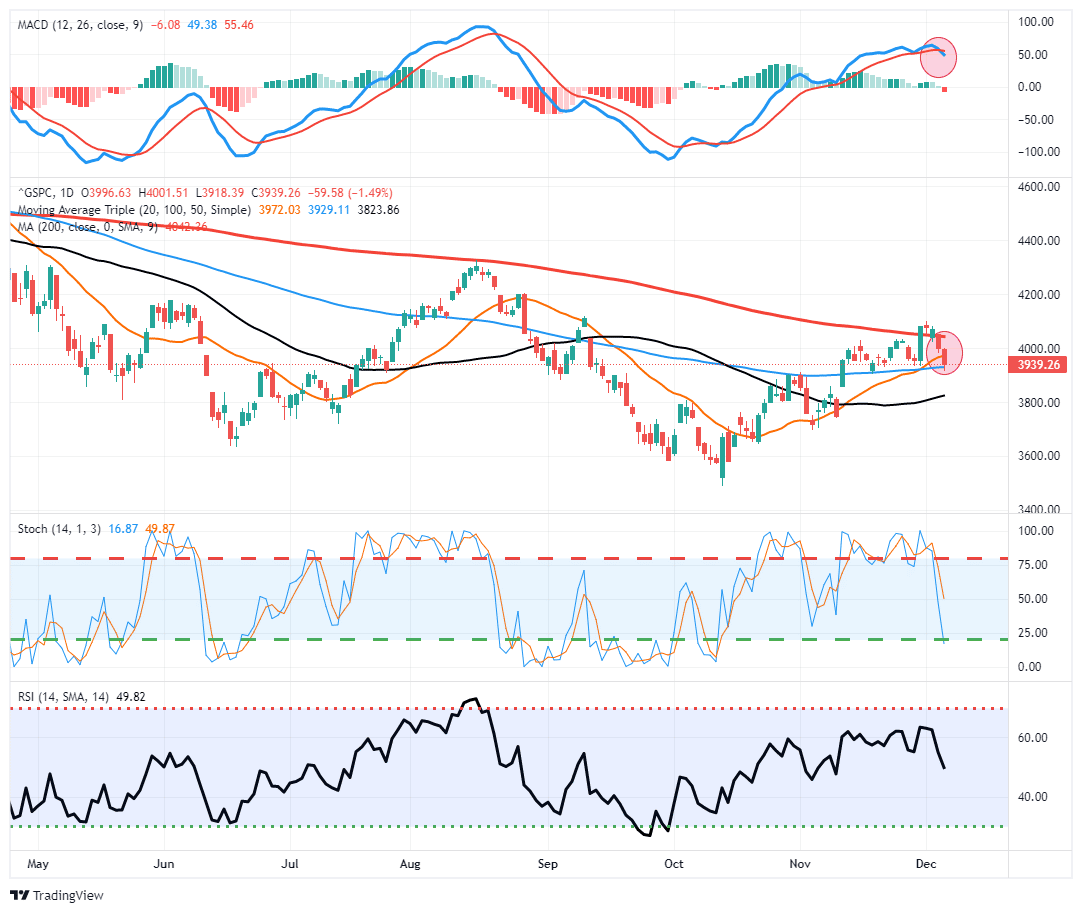

As discussed in yesterday’s commentary, the market sold off following the release of the WSJ’s commentary on the Federal Reserve’s stance on monetary policy remaining “hawkish.” After failing at the downtrend resistance line yesterday and violating the 200-dma, the “bears” regained market control. As I discussed in yesterday’s 3-minutes video, any sell-off yesterday would trigger the MACD “sell signal,” which has been a good indicator to reduce risk and raise cash. That signal did trigger yesterday.

So far, as indicated below, the market is trading within the consolidation range of the last 3-weeks. Also, the market did hold the 100-dma support level yesterday. However, if the market breaches that support, it is lower to the 50-dma. So far, the first 2-weeks of December are playing out as expected: “Sloppy Trade With A Chance Of Decline.” That action, barring an extremely hawkish post-FOMC speech from Jerome Powell next week, should set the market up for the year-end “Santa Rally.”

Recession Talk

Many economic prognosticators are forecasting a recession. This may be precisely what Jerome Powell wants in his efforts to tighten financial conditions and break inflation’s back. Is it possible that hawkish Fed actions and rhetoric, along with recession forecasts get economic activity to slow enough to stop inflation but not enough to generate a recession? Such a “soft landing” is the Fed’s ideal scenario. While we think the odds of a recession are high, a soft landing scenario is something we frequently discuss in our investment committee meetings as it potentially has big implications for our investment outlook. The following bit on CNBC is worth considering.

UNITED AIRLINES CEO: “If I didn’t watch @CNBC in the morning — which I do — the word ‘recession’ wouldn’t be in my vocabulary. You just can’t see it in our data.”

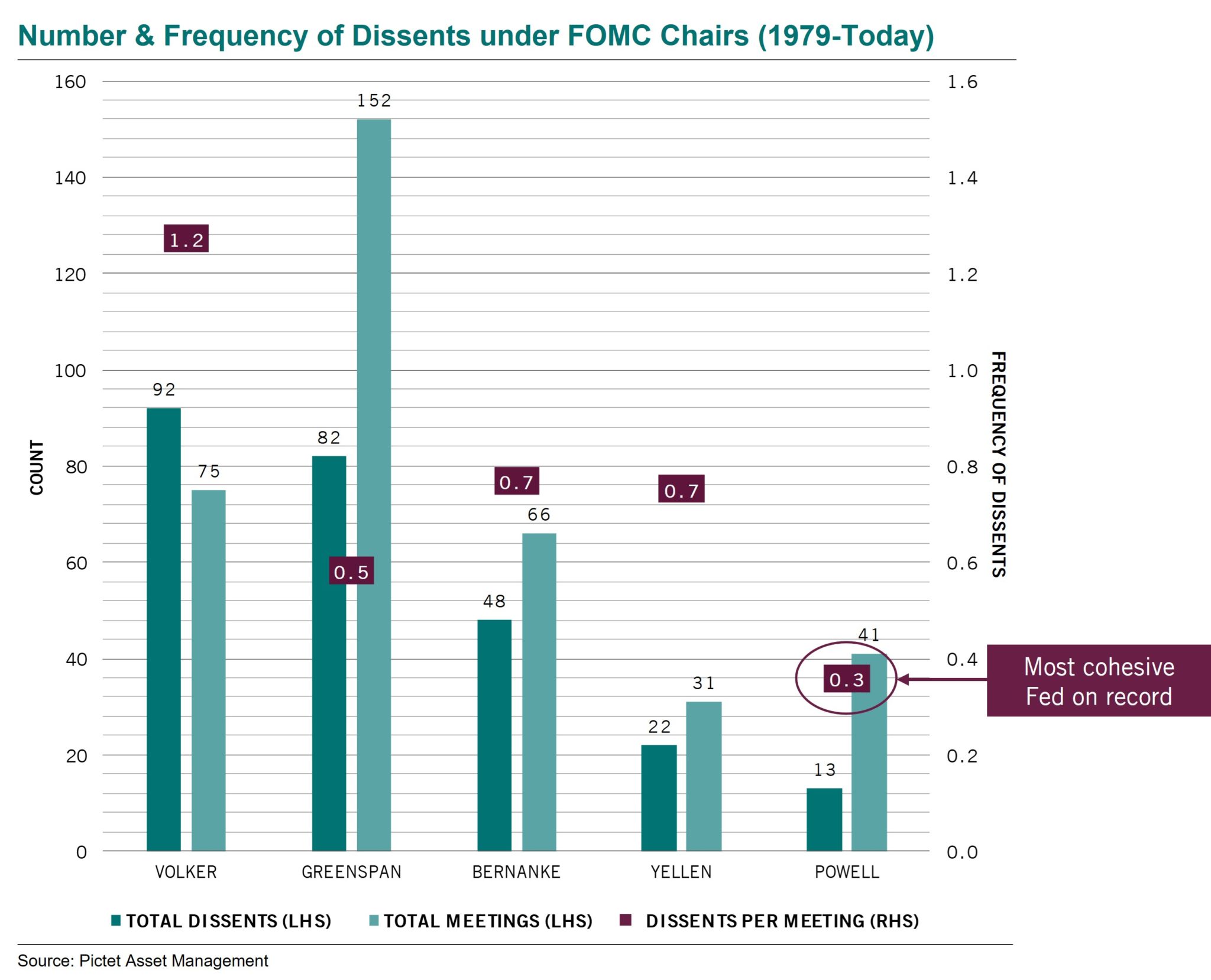

A Very Cohesive Fed

Jerome Powell seems to have formed a strong and unified front against inflation within the FOMC. As Pictet Asset Management shows below, on average, there is only one dissenting Fed member per three FOMC meetings under Powell’s tenure. However, keeping a cohesive hold on Fed members will become increasingly harder as rates near their terminal level and economic activity begins to fall off. The more dissents, the tougher the Fed’s job, especially if inflation doesn’t retreat as quickly as Powell wants it to. As such, 2023 may prove much harder for Powell than 2022.

S&P 500 Is in the Danger Zone

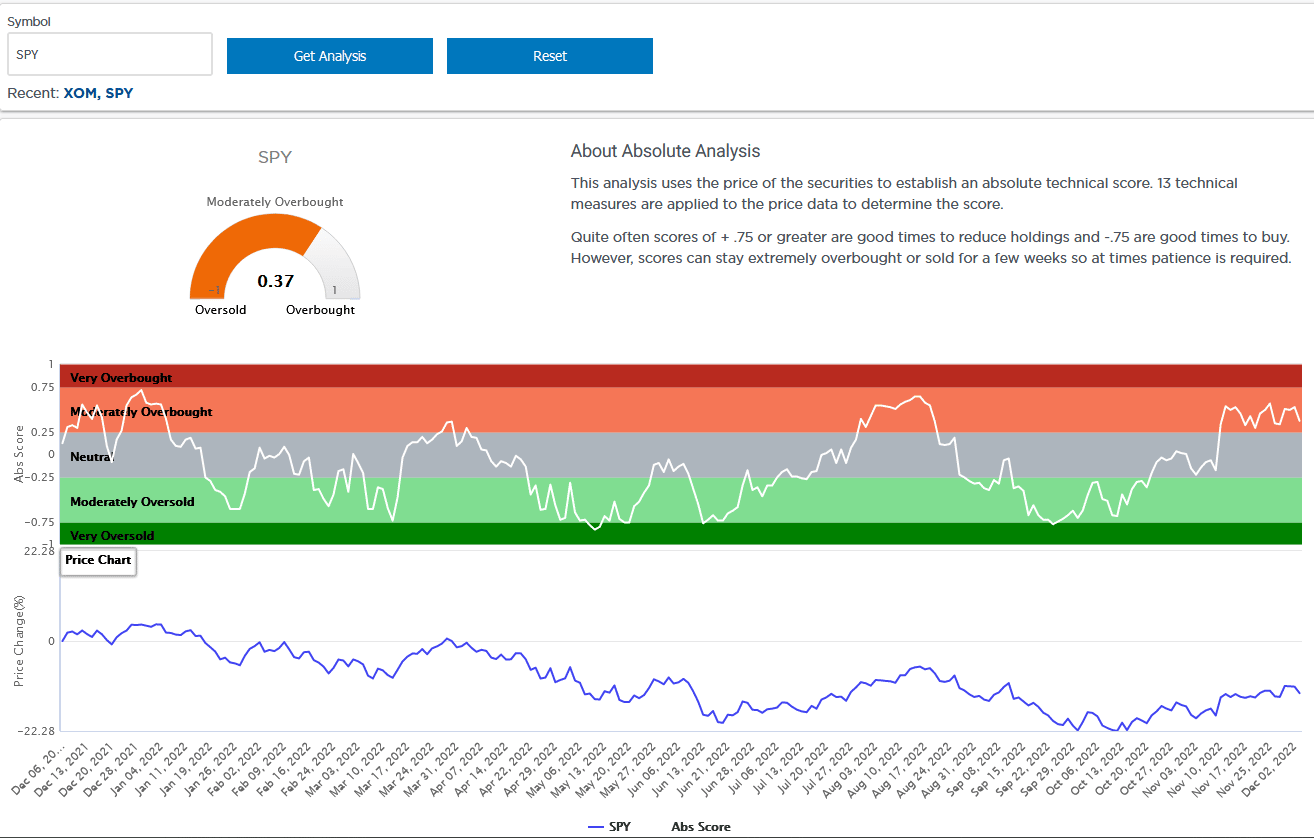

A few months ago, we added a new technical tool in SimpleVisor. The Relative Analysis tools allow SV users to perform technical relative analysis on any two tickers as well as all of the sectors versus the S&P 500. The analysis, using 13 technical analysis models, takes the ratio of the price of two tickers and scores the pair as fair value, overbought, or oversold. We are adding another similar tool. Users can now perform the same technical analysis on individual tickers, not pairs. For SV subscribers, the Absolute Analysis tool can be found under Ideas > Absolute Analysis.

The graph below shows the absolute analysis of SPY. SPY has been in moderately overbought (orange) territory, as it is today, three other times this year. All three instances accompanied a local peak in SPY. If the market rallies from current levels and breaks upward through key resistance, we expect this overbought condition will stay overbought. That said, we offer caution, as the market is clearly in a downward trend. Overbought conditions have proven great times for reducing equity exposure and managing risk.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read