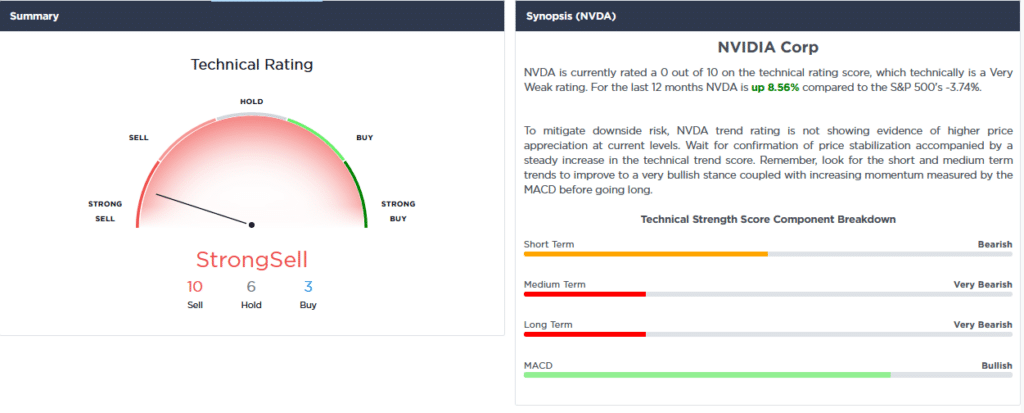

Nvidia (NVDA) joins a long list of companies that reported decent earnings but reduced their future earnings guidance. Many of these companies saw their stocks fall sharply. After reporting earnings on Wednesday night, Nvidia appeared to be another on that list. Nvidia beat earnings and sales estimates, but they reduced forward sales guidance by approximately $400 million due to China’s covid lockdowns and the Russian conflict. Initially,

Nvidia stock fell by over 10%. However, unlike most other companies in similar shoes, Nvidia rebounded and finished up by over 5%. Nvidia. Maybe investors realize that Nvidia’s earnings were good and the short-term revenue warning is temporary. It is more likely that investors have priced in worse scenarios than are occurring. The market’s reaction to Nvidia’s earnings may signal a change in sentiment and possibly a durable market bounce.

U.S. markets will be closed on Monday for the Memorial Day holiday.

What To Watch Today

Economy

- 8:30 a.m. ET: Advance Goods Trade Balance, April (-$114.8 billion expected, -$127.1 billion prior)

- 8:30 a.m. ET: Wholesale Inventories, month-over-month, April preliminary (2.0% expected, 2.3% prior)

- 8:30 a.m. ET: Personal Income, month-over-month, April (0.5% expected, 0.5% prior)

- 8:30 a.m. ET: Personal Spending, month-over-month, April (0.6% expected, 1.1% prior)

- 8:30 a.m. ET: Real Personal Spending, month-over-month, April (0.5% expected, 0.2% prior)

- 8:30 a.m. ET: Retail Inventories, month-over-month, April (2.0% prior)

- 8:30 a.m. ET: PCE Deflator, month-over-month, April (0.2% expected, 0.9% prior)

- 8:30 a.m. ET: PCE Deflator, year-over-year, April (6.2% expected, 6.6% prior)

- 8:30 a.m. ET: PCE Core Deflator, month-over-month, April (0.3% expected, 0.3% prior)

- 8:30 a.m. ET: PCE Core Deflator, year-over-year, April (4.9% expected, 5.2% prior)

- 10:00 a.m. ET: University of Michigan Sentiment, May final (59.1 expected, 59.1 prior)

Earnings

Pre-market

- Big Lots (BIG) to report adjusted earnings of 99 cents on revenue of $1.46 billion

- Pinduodo (PDD) to report adjusted earnings of 1.54 yuan on revenue of 20.74 billion yuan

Post-market

- No notable reports are scheduled for release

Market Rallies – Finally

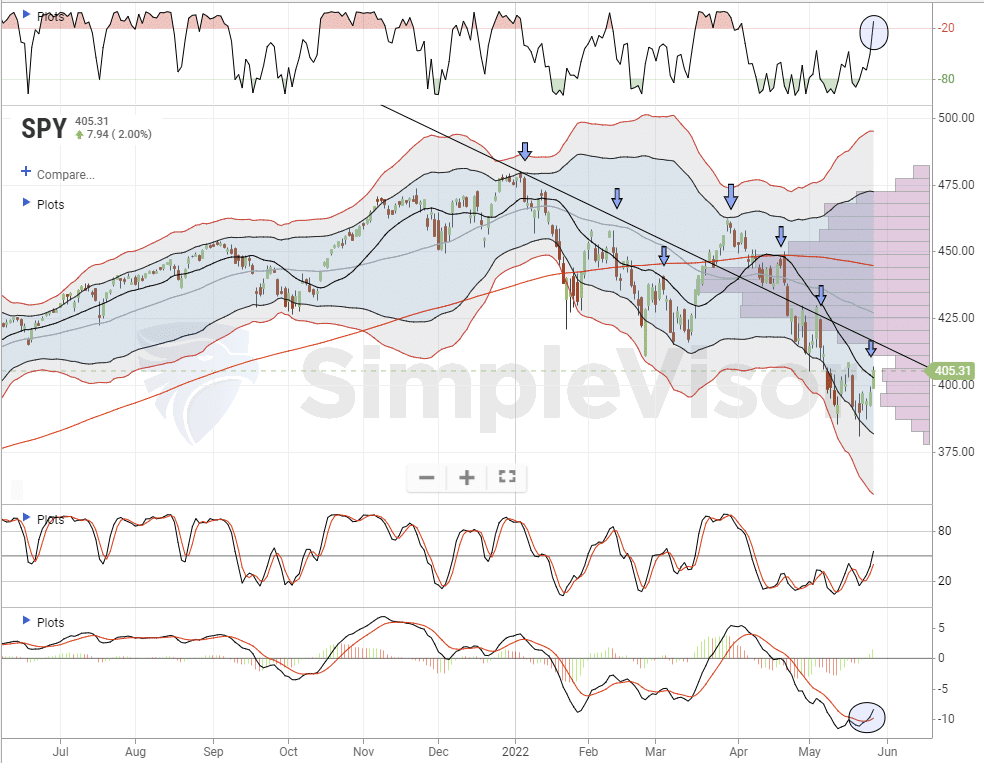

Yesterday, the market rallied and broke above the 20-dma. This is the first really bullish action we have seen in a while. The question, of course, is how long will it last? There are a LOT of trapped longs in the market, all looking for a rally to sell into. However, on the other side, there is a large short position that could fuel the rally further if the market can break above the downtrend line from the January peak. The MACD buy signal is firmly in place but the market is already moving back into overbought territory. Use the rally to sell into and reduce risk.

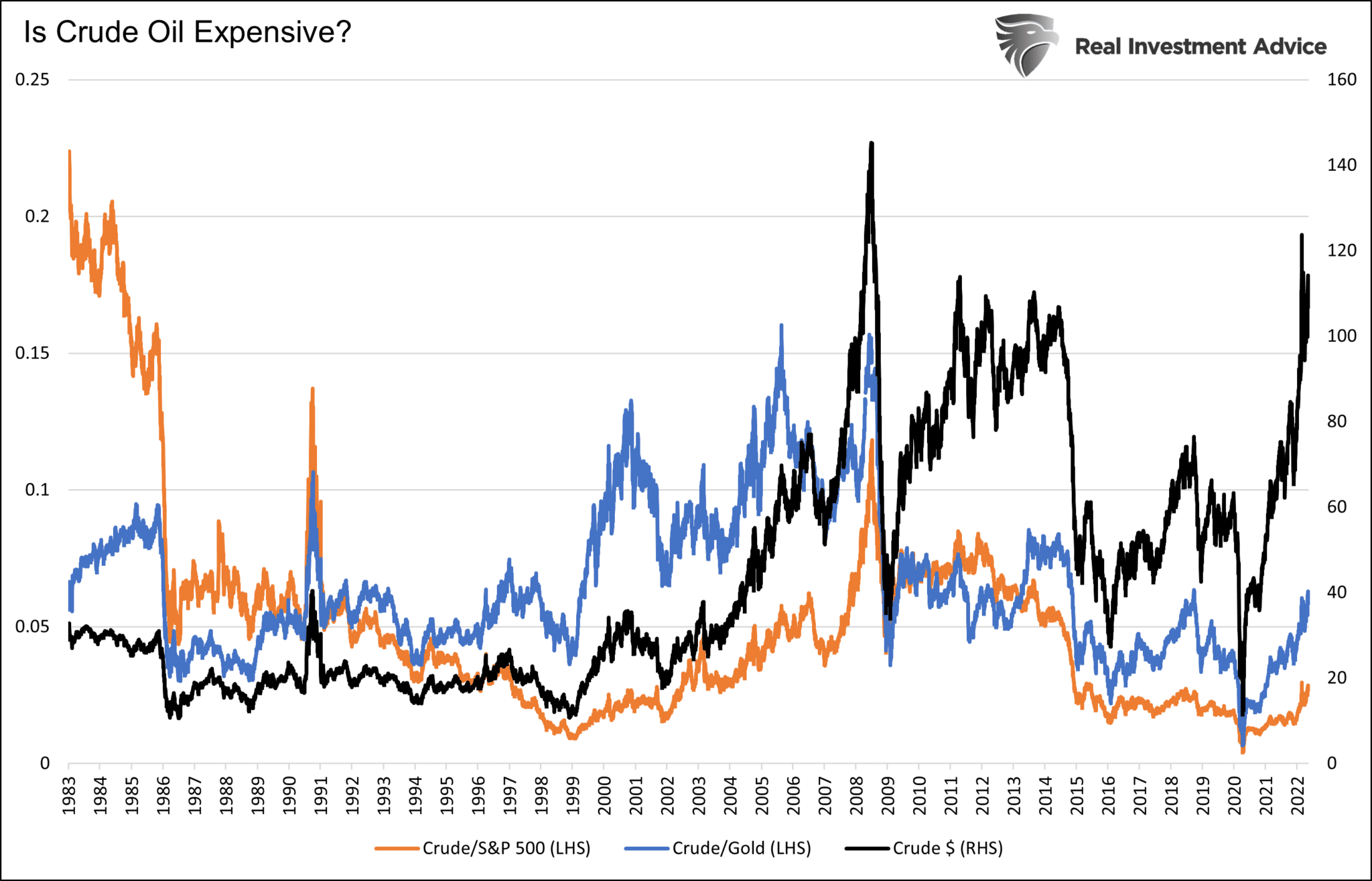

Are Oil Prices Expensive?

The easy answer to our question is YES! Since 1983, the price of crude oil has only been higher than current prices one percent of the time. However, looking at oil prices from different viewpoints can lead to other answers. The graph below shows the price of crude oil as measured in dollars (black). It also charts the ratio of the price of crude oil to the S&P 500 and gold. As we show below, the ratio of oil to stocks and gold is not very expensive. In fact, the ratio to the S&P 500 has been higher about two-thirds of the time since 1983. The ratio of oil to gold is at the midpoint of where it has traded over the last 40 years.

Using these metrics, one may argue crude is fairly priced. Instead, it might be the dollar’s declining purchasing power that makes oil seem expensive.

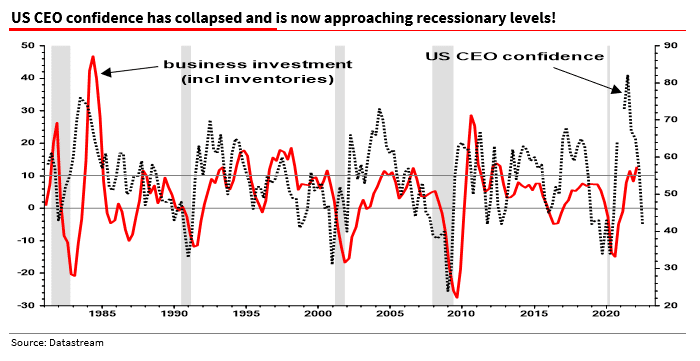

US CEO Confidence Has Collapsed

The FT’s Robert Armstrong, in his excellent daily note last Friday, really made me think. Robert wrote, “First-quarter earnings from two big American retailers scared the daylights out of markets this week. Walmart and Target are down 20 percent and 29 percent, respectively, since they reported. These two companies are very important for investors because — as nation‑spanning sellers of food, clothes, home goods, and much else — they provide a window into the health of the American consumer, who drives the American economy and the worlds. So it is not totally illogical that in the wake of the box stores’ poor results, all sorts of consumer staples companies, usually a safe haven in a storm, took a whipping.”

It wasn’t revenues that were the primary cause of the profit disappointment. Rather it was sharply declining margins that many then attributed to rising costs – especially labor costs. However, Armstrong points out that in fact, it was the cost of dealing with unwanted inventories that had squeezed margins. He wrote “At Walmart, sales were up 2% from last year’s first quarter. Inventories were up 32%. That is to say: there was $15bn in extra inventory sitting around at Walmart at the end of the quarter. At Target, it was 4% and 43% — $5bn in extra inventory. And what happens when you’ve ordered several billions worth more stuff than your customers want? You mark prices down to get rid of it all. And down go margins.” – see his note here.

Although inventory liquidation might be good news for taking the heat out of rampant inflation, it certainly isn’t good for future GDP growth as orders will need to be slashed. It got me thinking, if this is a more general problem maybe it helps explain why US CEO confidence has collapsed recently – something which normally precedes an investment downturn. Swings in inventories often dominate the business investment cycle and invariably cause recessions – Albert Edwards, Societe Generale

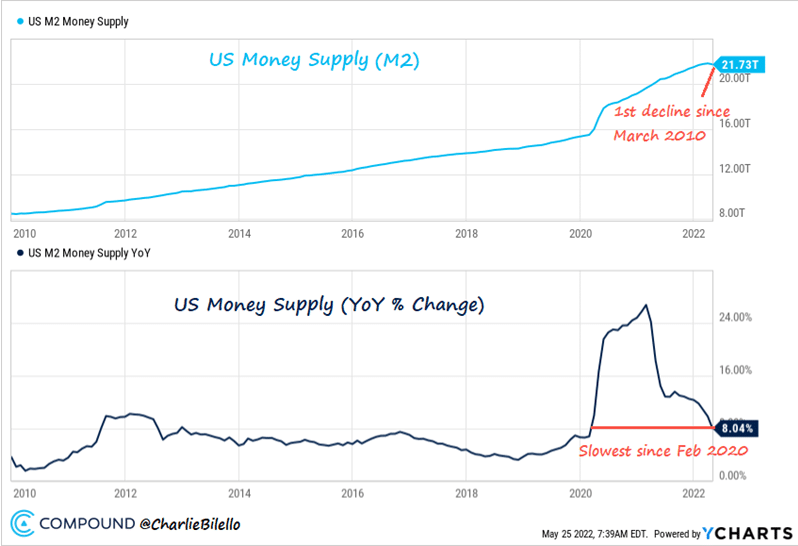

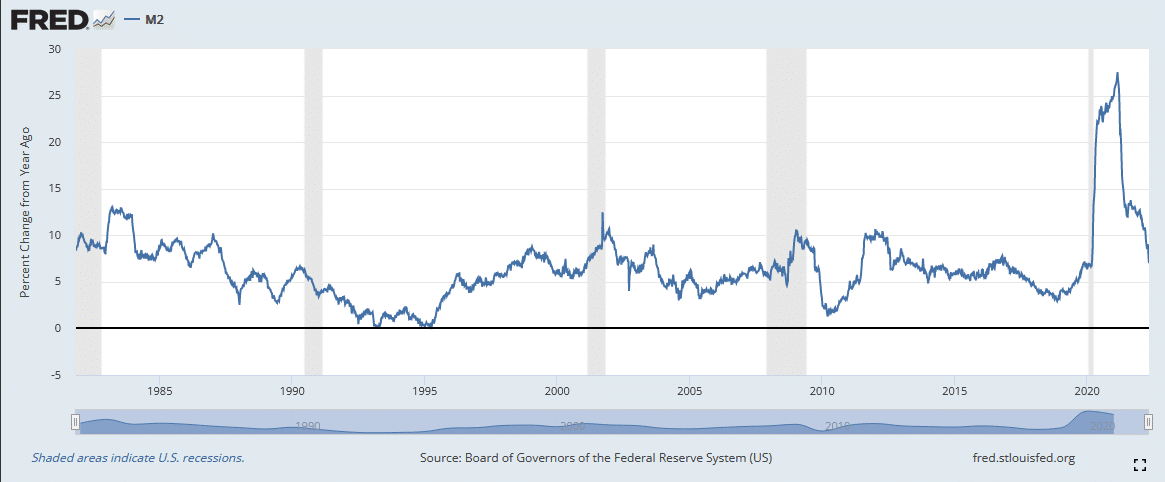

Money Supply in Decline

The first graph below shows that the money supply as measured by M2 declined for the first time in 12 years in March. The second graph shows that the annual change in M2 is falling rapidly. Assuming the Fed goes ahead with QT in June, as they claim, the year-over-year change in M2 could likely be negative. As shown in the third graph, that would be the first decline in annual M2 since at least 1980. Unless the velocity of M2 picks up, which it materially hasn’t yet, the combination of weak velocity and declining money supply should provide a deflationary push to prices.

Portfolio Yields Remain Too Low

Brian McAuley of Sitka Pacific Capital Management shares the following:

“In October 1929, the yield of a cyclically-adjusted 60/40 portfolio of U.S. stocks and bonds bottomed out at 3.20%, which was the lowest portfolio yield up to that point in time. As frenzied as the tech bubble was eight decades later, the cyclically-adjusted yield remained above its 1929 low in 2000, and bottomed out at 3.77%. These were the two worst times in history to be invested in U.S. risk assets…until the current cycle.”

The yield on a 60/40 stock/bond portfolio, including stock dividends and bond interest, is a meager 3.05%, as shown below. While recent declines in stock prices and higher bond yields have increased the portfolio’s yield by almost a full percent, they remain woefully low. If the yield is to normalize, there may be more pain ahead for stock and/or bond investors.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read