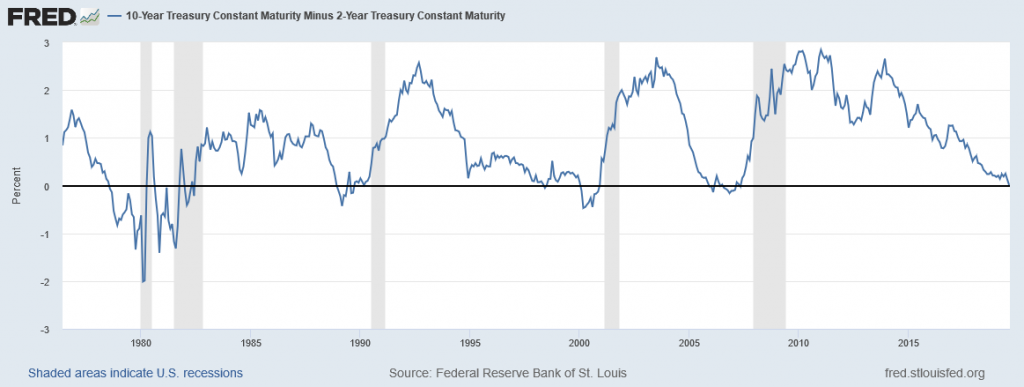

Since August of 1978, there have been seven instances where the yields on ten-year Treasury Notes were lower than those on two-year Treasury Notes, commonly referred to as “yield curve inversion.” That count includes the current episode which only just occurred. In all six prior instances a recession followed, although in some cases with a lag of up to two years.

Given the yield curve’s impeccable 30+ year track record of signaling recessions, we think it is appropriate to compare the current inversion to those of the past. In doing so, we can further refine our economic and market expectations.

Bull or Bear Flattening

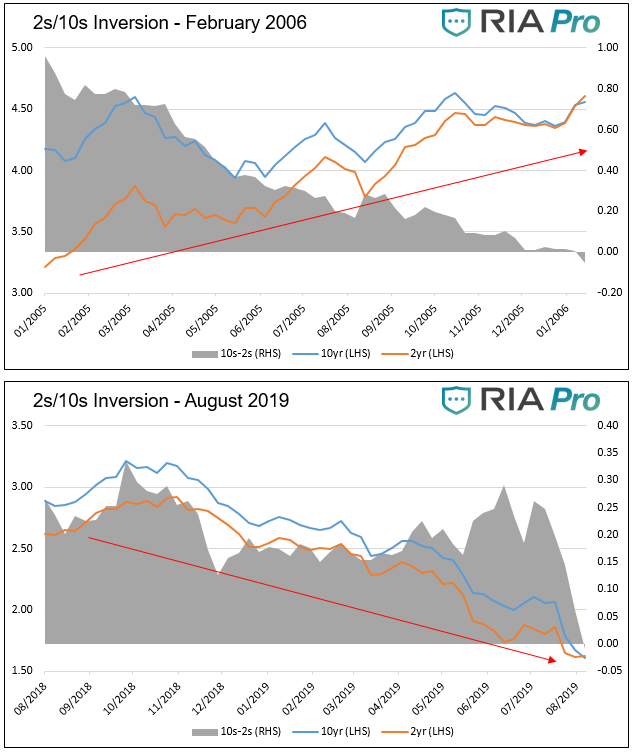

In this section, we graph the seven yield curve inversions since 1978, showing how ten-year U.S. Treasuries (UST), two-year UST and the 10-year/2 year curve performed in the year before the inversion.

Before progressing, it is worth defining some bond trading lingo:

- Steepener- Describes a situation in which the difference between the yield on the 10-year UST and the yield on the 2y-year UST is increasing. Steepeners can occur when both securities are trending up or down in yield or when the 2-year yield declines while the 10-year yield increases.

- Flattener- A flattener is the opposite of a steepener, and the difference between yields is declining. As shown in the graph above, the slope of the curve has been in a flattening trend for the last five years.

- Bullish/Bearish- The terms steepener and flattener are typically preceded with the descriptor bullish or bearish. Bullish means yields are declining (bond prices are rising) while bearish means yields are rising (bond prices are falling). For instance, a bullish flattener means that both 2s and 10s are declining in yield but 10s are declining at a quicker pace. A bearish flattener implies that yields for 2s and 10s are rising with 2s increasing at a faster pace. Currently, we are witnessing a bullish flattener. All inversions, by definition, are preceded by a flattening trend.

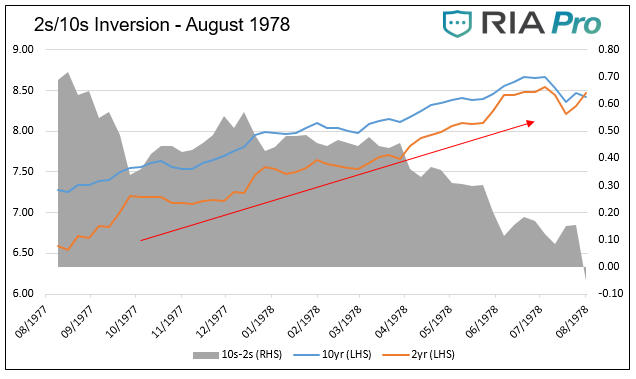

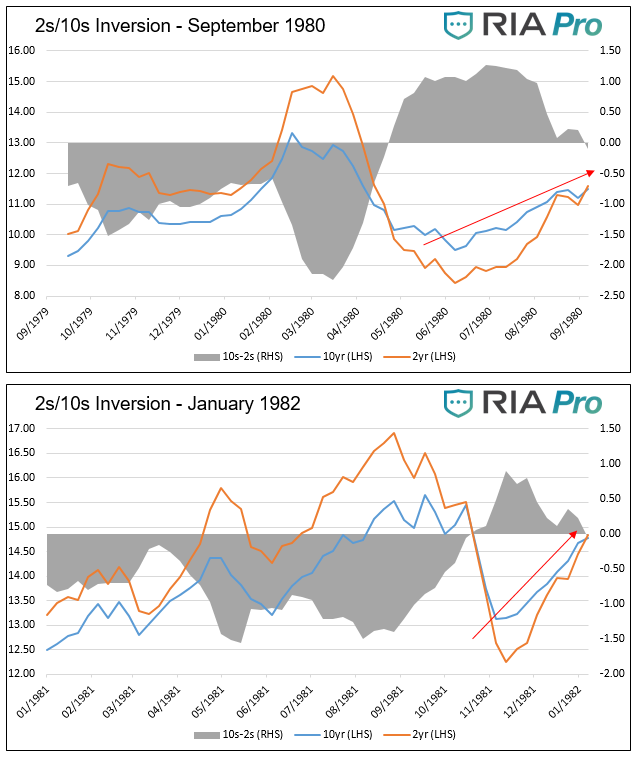

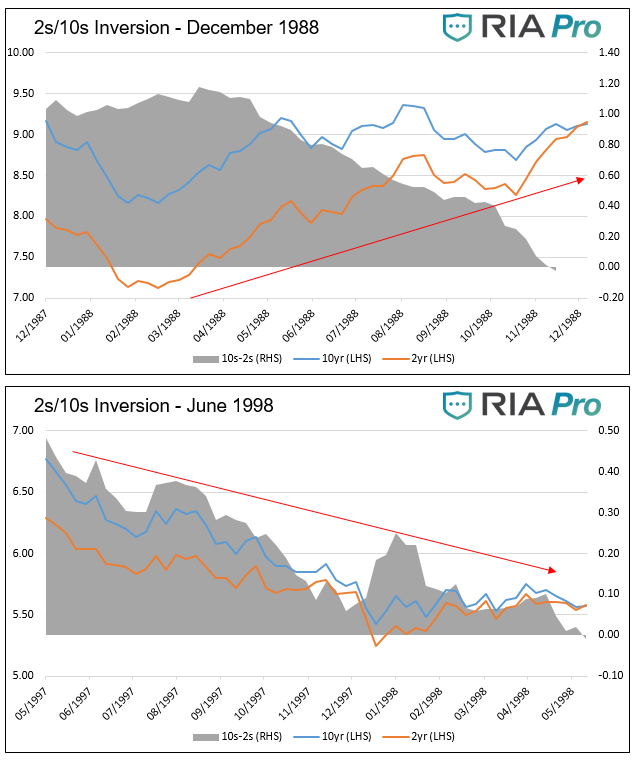

As shown in the seven graphs below, there are two distinct patterns, bullish flatteners and bearish flatteners, which emerged before each of the last seven inversions. The red arrows highlight the general trend of yields during the year leading up to the curve inversion.

Data for all graphs courtesy St. Louis Federal Reserve

Five of the seven instances exhibited a bearish flattening before inversion. In other words, yields rose for both two and ten year Treasuries and two year yields were rising more than tens. The exceptions are 1998 and the current period. These two instances were/are bullish flatteners.

Bearish Flattener

As the amount of debt outstanding outpaces growth in the economy, the reliance on debt and the level of interest rates becomes a larger factor driving economic activity and monetary and fiscal policy decisions. In five of the seven instances graphed, interest rates rose as economic growth accelerated and consumer prices perked up. While the seven periods are different in many ways, higher interest rates were a key factor leading to recession. Higher interest rates reduce the incentive to borrow, ultimately slowing growth and in these cases resulted in a recession.

Bullish Insurance Flattener

As noted, the current period and 1998 are different from the other periods shown. Today, as in 1998, yields are falling as the 10-year Treasury yield drops faster than the 2-year Treasury yield. The curve thus flattens and ultimately inverts.

Seven years into the economic expansion, during the fall of 1998, the Fed cut rates in three 25 basis point increments. Deemed “insurance cuts,” the purpose was to counteract concerns about sluggish growth overseas and financial market concerns stemming from the Asian crisis, Russian default, and the failure of hedge fund giant Long Term Capital. The yield curve inversion was another factor driving the Fed. The domestic economy during the period was strong, with real GDP staying above 4%, well above the natural growth rate.

The current period is somewhat similar. The U.S. economy, while not nearly as strong as the ’98 experience, has registered above-trend economic growth for the last two years. Also similar to 1998, there are exogenous factors that are concerning for the Fed. At the top of the list are the trade war and sharply slowing economic activity in Europe and China. Like in 1998, we can add the newly inverted yield curve to the list.

The Fed reduced rates by 25 basis points on July 31, 2019. Chairman Powell characterized the cut as a “mid-cycle adjustment” designed to ensure solid economic growth and support the record-long expansion. Some Fed members are describing the cuts as an insurance measure, similar to the language employed in 1998.

If 1998-like “insurance” measures are the Fed’s game plan to counteract recessionary pressures, we must ask if the periods are similar enough to ascertain what may happen this time.

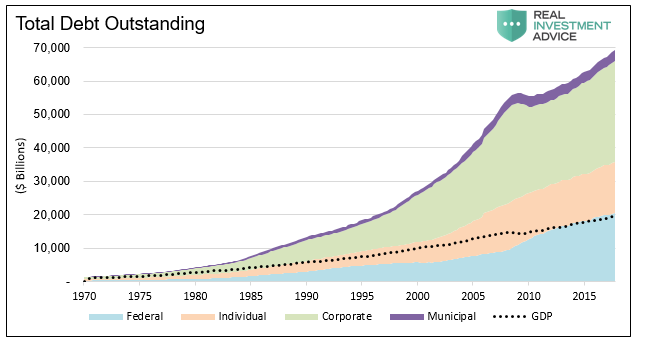

A key differentiating factor between today and the late 1990s is not only the amount of debt but the dependence on it. Over the last 20 years, the amount of total debt as a ratio to GDP increased from 2.5x to over 3.5x.

Data Courtesy St. Louis Federal Reserve

In 1998, believe it or not, the U.S. government ran a fiscal surplus and Treasury debt issuance was declining. Today, the reliance on debt for new economic activity and the burden of servicing old debt has never been greater in the United States. Because rates are already at or near 300-year lows, unlike 1998, the marginal benefits from borrowing and spending as a result of lower rates are much less economically significant currently.

In 1998, the internet was in its infancy and its productive benefits were just being discovered. Productivity, an essential element for economic growth, was booming. By comparison, current productivity growth has been lifeless for well over the last decade.

Demographics, the other key factor driving economic activity, was also a significant component of economic growth. Twenty years ago, the baby boomers were in their spending and investing prime. Today they are retiring at a rate of 10,000 per day, reducing their consumption and drawing down their investment accounts.

The key point is that lower rates are far less likely to spur economic activity today than in 1998. Additionally, the natural rate of economic growth is lower today, so the economy is more susceptible to recession given a smaller decline in economic activity than it was in 1998.

The 1998 rate cuts led to an explosion of speculative behavior primarily in the tech sectors. From October of 1998 when the Fed first cut rates, to the market peak in March of 2000, the NASDAQ index rose over 300%. Many equity valuation ratios from the period set records.

We have witnessed a similar but broader-based speculative fervor over the last five years. Valuations in some cases have exceeded those of the late 1990s and in other cases stand right below them. While the economic, productivity, and demographic backdrops are not the same, we cannot rule out that Fed cuts might fuel another explosive rally. If this were to occur, it will further reduce expected returns and could lead to a crushing decline in the years following as occurred in the early 2000s.

Summary

A yield curve inversion is the bond market’s way of telegraphing concern that economic growth will slow in the coming months. Markets do not offer guarantees, but the 2s-10s yield curve has been right every time in the last 30 years it voiced this concern. As the book of Ecclesiastes reminds us, “the race does not always go to the swift nor the battle to the strong…”, but that’s the way to bet.

Insurance rate cuts may buy the record-long economic expansion another year or two as they did 20 years ago, but the marginal benefit of lower rates is not nearly as powerful today as it was in 1998.

Whether the Fed combats a recession in the months ahead as the bond market warns or in a couple of years, they are very limited in their abilities. In 2000 and 2001, the Fed cut rates by a total of 575 basis points, leaving the Fed Funds rate at 1.00%. This time around, the Fed can only cut rates by 225 basis points until it reaches zero percent. When we reach that point, and historical precedence argues it will be quicker than many assume, we must then ask how negative rates, QE, or both will affect the economy and markets. For this there is no prescriptive answer.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read