Last Friday, the S&P 500 briefly dipped to 3810, marking a 20.5% decline from its January 3rd record high. Many investors consider a 20% decline to be a bear market. While we can debate whether the market is or isn’t in a bear market, our time is best spent honing in on expectations in case we are in a bear market. We can measure bear market expectations in terms of time and performance. The graph below compares the current “bear market” with other bear markets over the last 100 years. If we are in a bear market, we should have expectations for losses of 30-60%. The time window for said losses might be short, as we recently saw in 2020, or it could extend out 400 trading days.

We are not declaring a bear market has started. However, we advise forming expectations of what a bear market may entail. If we are entering a longer-term bear market with more significant declines, risk management and limiting losses are critical to preserving wealth and prospering when a true bottom occurs.

What To Watch Today

Economy

- 9:45 a.m. ET: S&P Global US Manufacturing PMI, May preliminary (57.7 expected, 59.2 during prior month)

- 9:45 a.m. ET: S&P Global US Services PMI, May preliminary (55.2 expected, 55.6 during prior month)

- 9:45 a.m. ET: S&P Global US Composite PMI, May preliminary (55.7 expected, 56.0 during prior month)

- 10:00 a.m. ET: Richmond Fed Manufacturing Index, May (12 expected, 14 during prior month)

- 10:00 a.m. ET: New Home Sales, April (750,000 expected, 763,000 during prior month)

- 10:00 a.m. ET: New Home Sales, month-over-month, April (-1.7%, -8.6% during prior month)

Earnings

Pre-market

- Abercrombie and Fitch (ANF) to report adjusted earnings of 7 cents on revenue of $800.13 million

- Autozone (AZO) to report adjusted earnings of $26.23 on revenue of $3.73 billion

- Best Buy (BBY) to report adjusted earnings of $1.60 on revenue of $10.41 billion

- Ralph Lauren (RL) to report adjusted earnings of 39 cents on revenue of $1.46 billion

- Petco (WOOF) to report adjusted earnings of 14 cents on revenue of $1.45 billion

Post-market

- Agilent Technologies (A) to report adjusted earnings of $1.12 on revenue of $1.62 billion

- Nordstrom (JWN) to report adjusted losses of 5 cents on revenue of $3.26 billion

- Toll Brothers (TOL) to report adjusted earnings of $1.50 on revenue of $2.10 billion

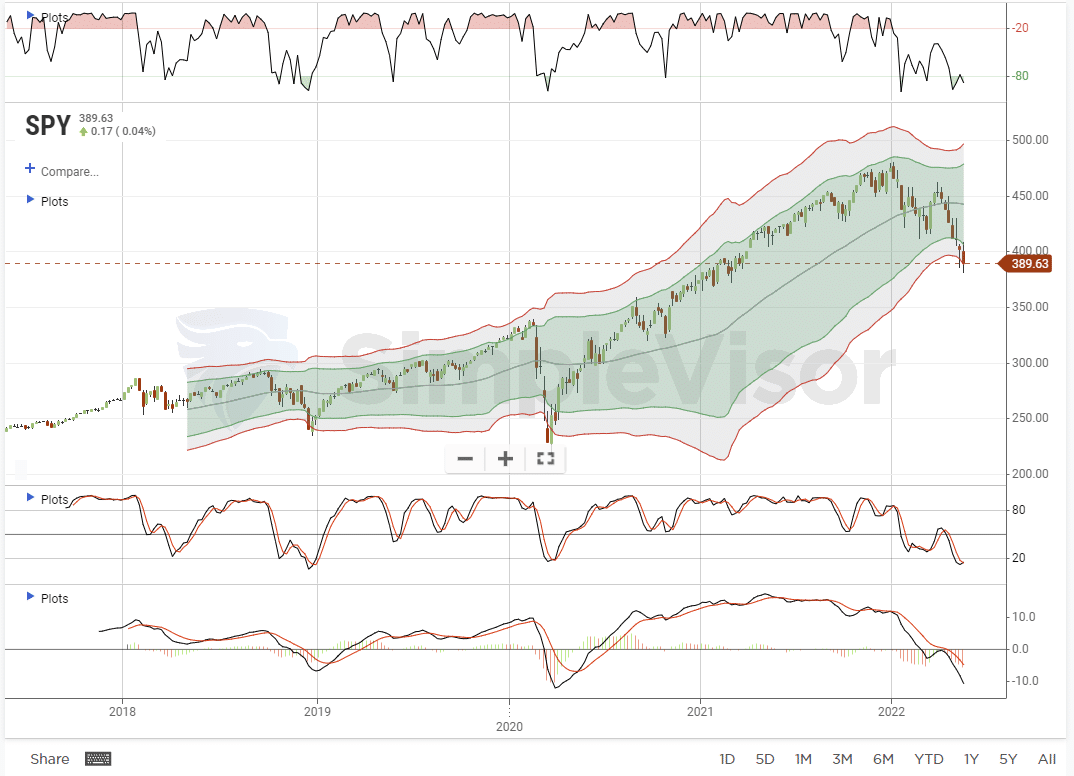

S&P 500 Technical Update

Every Monday, we share a series of technical charts with Simplevisor subscribers. Yesterday we presented technical analysis on the major stock indexes and U.S. Treasuries, Gold, Bitcoin, and Crude oil. As we note in Monday’s SimpleVisor post, the S&P 500 is very oversold, and a rally is entirely possible.

As we begin to manage bear market expectations, the big question many investors harbor is whether this potential rally signifies a bottom like March 2020 or is it a “sellable rally to reduce risk.” For more of our thoughts, see our notes below the graph.

For the entire report, visit us at SimpleVisor and see how it can improve your investment insight with a free 30-day trial.

- In the last 5-years, the only time the market was 3-standard deviations below the 1-year moving average was at the bottom of the market in 2018 and 2020.

- Currently, the market is on an intense sell signal (bottom panel) equal to March 2020

- The market is as oversold (top panel) as any previous market low.

- Short-Term Positioning: Sellable Rally To Reduce Risk

- Buy with a target of $430

- Stop-loss is currently $380

- Long-Term Positioning: Neutral / Bearish

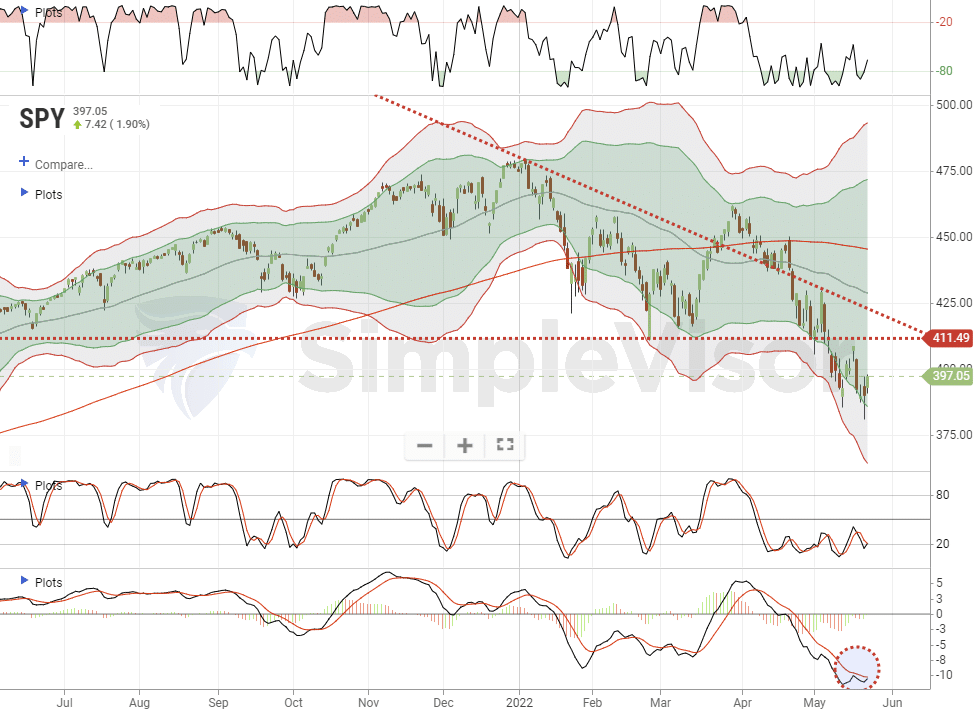

Market Rallies – Will Friday’s Retest Of Lows Hold?

On Monday, the market rallied following up on Friday’s intraday reversal that held the previous week’s lows. Unfortunately, over the last 2-months, the market has consisted of failed rallies that work to lower levels.

While the bounce off the lows is encouraging, there is strong resistance getting built at the intersection of the downtrend line from the market peak and the recent support lows taken out two weeks ago. Notably, the MACD buy trigger (lower panel) is close to turning positive which could give the markets a bit of lift short-term.

Use rallies from 411 to 425 (SPDR S&P 500 ETF – SPY) to reduce portfolio risk, raise cash and rebalance exposures accordingly.

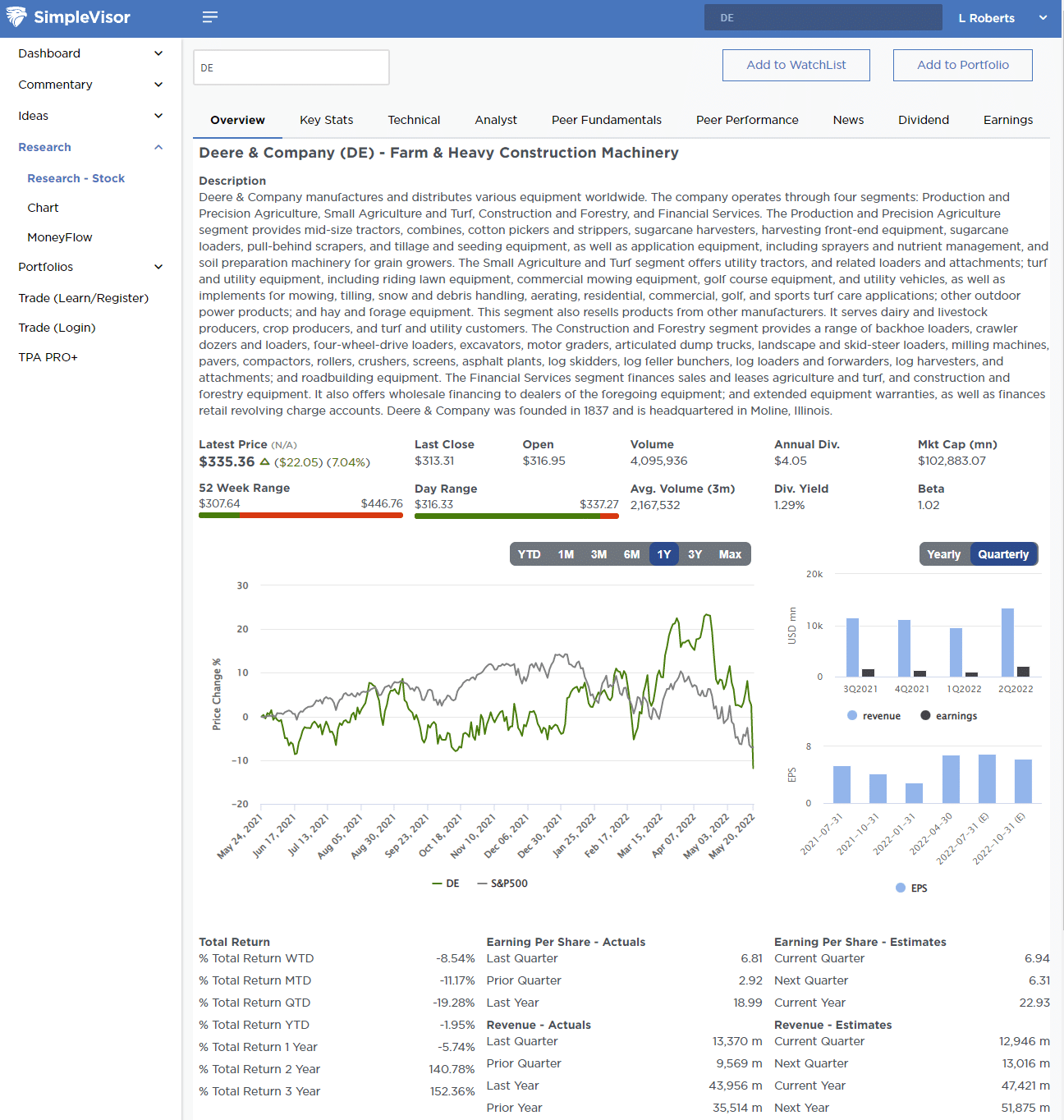

New Simple Visor Feature

We just released a new update to Simplevisor.com that provides a comprehensive look at individual corporate equities. From a complete corporate overview, shown below, to Key Stats, Technical Gauge, Analyst rankings, Peer Fundamentals, Performance, and more.

Subscribers will see the new feature under the Research Tab (Try the entire platform free for 30-days.)

Retail Exposure and High Valuations

The correlation between equity exposure for retail accounts and equity valuations is robust. Today, retail exposure is the highest on record, possibly portending a peak as valuations begin to normalize.

“The extent to which US households have put their money into equities rather than other financial assets is startlingly high. It implies that equities are at the top of the cycle.” – John Authers – Bloomberg

Inventory Build Up

Last week Walmart, Target, and other retailers warned investors that inventories are starting to accumulate, consumer behaviors are changing, and earnings are getting squeezed by inflation. We share a few key takeaways from Ayesha Tariq from her weekly commentary.

- The rate of inflation has been surprising. So it’s not just that there is a general level of inflation in the economy but the rate of increase and the persistence is what is causing a real problem.

- People are buying groceries but not merchandise. So the level of discretionary spending has dropped, and this is exactly what was expected.

- The problem with a decrease in spending on discretionary items is that it creates pressure on margins. General Merchandise tends to have higher margins vs. staples.

- While the average basket size has increased, the items per basket have decreased because the per-item cost has gone up. Purchasing power for consumers is decreasing and this doesn’t bode well for retailers as more and more people will move to lower-cost, low-margin items.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read