Areté’s Observations 9/26/20

Market observations

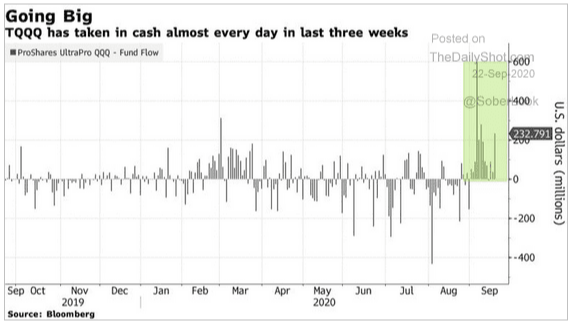

Although the market has trended down since early September, declines have been orderly and at least partly a consolidation of big gains over the summer. The graph below shows inflows for the 3x leveraged Nasdaq 100 ETF. Needless to say, the speculative urge is still rampant.

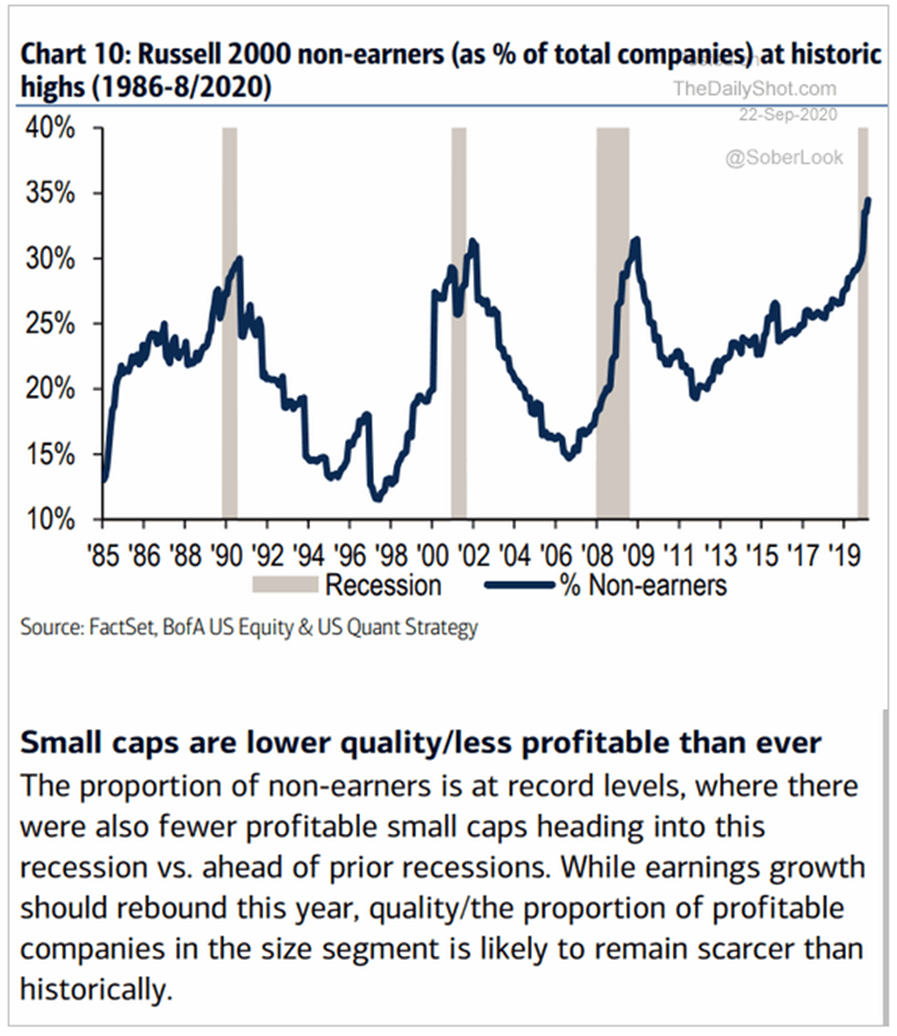

Another area where the speculative urge still seems rampant is with small cap stocks. More sensitive than large cap stocks, small caps can produce greater returns when stocks are working, but greater losses when they aren’t. The graph below shows the case for small caps is becoming more fraught by the day as the Russell 2000 index is increasingly comprised of companies that are unprofitable. Recent research suggests this is a particular problem for small caps.

“The regression results do imply that size adds significant value when used in conjunction with quality. Taking a closer look at this result, we find that it is entirely driven by the short side of quality portfolios and breaks down for the long side. In sum, the added value of size appears to be limited to investors who short US junk stocks.”

In other words, according to the paper, the best way to make money with small caps is to short the low-quality ones. This is the exact opposite of what many investors are actually doing when they buy the Russell 2000 index as a leveraged bet on stocks in general.

Economy

There continues to be two almost diametrically opposed perspectives on the economy. From one angle, the economy appears to be on the mend.

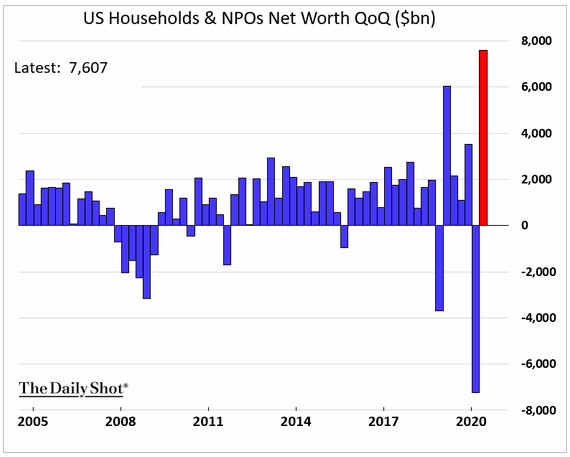

Household net worth in the US jumped last quarter and that was largely due to gains in the stock market. Not only can net worth solve a lot of problems, but it reflects positively on economic prospects as well.

By other measures, however, the economy is still extremely weak. I have mentioned the statistics on hunger before, not least of which is because it is a real, tangible indicator of economic condition.

A new era of hunger has hit the US

“Ms Babineaux-Fontenot provides some shocking numbers. ‘I hope I’m wrong, but if I’m not’, she says, an extra 17m people in the US could be ‘food insecure’ in 2020 as a result of the pandemic. That would make a total of 54m, according to Feeding America’s calculations, up from 37.2m before the crisis. And 18m, or one in four, of those hungry people will be children.”

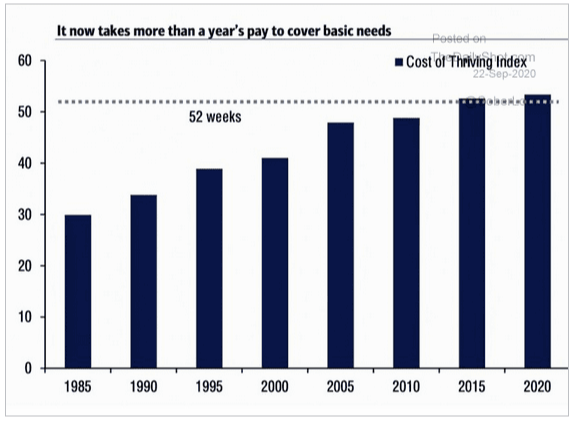

At very least, we can see how a focus on different measures can produce dramatically different perspectives of the economy. When the statistics on hunger are combined with the diminishing capacity of families to cover basic needs (graph below) it becomes evident there are structural problems in the economy that facilitate inequality. On one hand, overall net worth is rising rapidly; on the other, families can’t even afford to pay for basic needs on average.

Comments by the Fed chairman this week provide some important signals for investors on the subject.

Jay Powell warns recovery will suffer without stimulus

“Jay Powell, the chairman of the Federal Reserve, warned Congress that the US economic recovery would suffer if lawmakers failed to pass a new fiscal stimulus package, saying small businesses and lower-income households still needed government help.”

“’Many borrowers will benefit from these programmes, as will the overall economy, but for others, a loan that could be difficult to repay might not be the answer,’ Mr Powell said.”

By explicitly highlighting the importance of fiscal policy, Powell implicitly admitted the limits of monetary policy. That the market sold off after an uneventful Fed meeting last week points to the market’s dependence on the Fed’s largesse.

The comments were also notable for more directly addressing the issue of inequality. To date, the Fed has adamantly rejected any suggestion that it may be increasing inequality. This time, however, Powell as much as admitted that monetary policy has not been able to help small businesses or people with low incomes. By deduction then, monetary policy has provided a disproportionate benefit to owners of stocks and bonds.

We will have to see if Powell’s remarks are simply cheap words intended to mollify critics or if they represent a change in course. The test will be if stocks continue to fall. If they do, more action will be expected from the Fed. If the Fed ramps up interventions again, markets can rest assured the Fed still has their back. If the Fed doesn’t react to a continued selloff, investors will have to look for other reasons to continue believing in stocks. Regardless, it is interesting that the Fed is more directly addressing the issue of inequality.

Innovation

Cultural Innovation: The secret to building breakthrough businesses

“Procter & Gamble, for example, pursues what it calls constructive disruption. The company has designed its innovation process like a start-up’s, with a venture lab that pulls in tech entrepreneurs and a lean probe-and-learn prototyping process. That approach is not working.”

“Companies struggle because they put all their chips on one innovation paradigm—what I call better mousetraps … This is innovation as conceived by engineers and economists—a race to create the killer value proposition. It wins on functionality, convenience, reliability, price, or user experience.”

I introduced the notion of “fresh starts” in the 9/11/20 edition of Observations and since came across this article from HBR which applies slightly different language to the same concept. In short, some situations involve innovation that is linear and incremental. At other times, however, innovation involves a fundamental reimagining of what is valuable.

In a world of Covid restrictions this concept could hardly be timelier. As many of us are re-evaluating how much time we need to spend commuting, how often we need to wear business attire, where we should live, and a host of other things, what we are really doing is reflecting on what is most important to us.

“Better-mousetraps innovation is guided by quantitative ambitions: Outdo your competitors on existing notions of value. Cultural innovation operates according to qualitative ambitions: Change the understanding of what is considered valuable.”

As such, there is an enormous business opportunity to go beyond just building better mousetraps and instead to develop new goods and services that tap into some of the newly appreciated values. Since the approach by Proctor & Gamble and many other incumbent providers “is not working”, much of the opportunity is open to entrepreneurs and smaller companies. Although there will certainly also be difficulties and frictions along the way, there will also be opportunities for major breakthroughs.

Credit

Grant’s Interest Rate Observer, September 18,2020

“By intervening on an unprecedented scale, the Federal Reserve is supporting high-yield bond prices at a level that otherwise would be unimaginable in a recession, with commercial bankers wary of extending credit to all but the safest business borrowers.”

In a review of high-yield credit, Grants captured the above assessment from arguably the field’s pre-eminent authority, Marty Fridson, chief investment officer of Lehmann Livian Fridson Advisors, LLC. The comments elicit two thoughts. One relates to the artificial buoyancy of high-yield bonds. As Fridson himself acknowledges, such blessedness is fragile: “I’ve seen in the past that bonds just turn on a dime”.

Another thought is the increasing divergence between the “haves” and the “have nots” in the credit world. The difference is becoming less of a continuum and more of a distinct border. For instance, Grant’s notes that the median borrower among the 25% of least indebted companies saw leverage ratios decline last year.

Conversely, the median borrower among the 25% most indebted companies experienced leverage that almost doubled, “to 11 time Ebitda from 6.3 times last year”. For context, “an 11x net leverage number pretty much undermines a viable equity value for many HY companies …” Alas, such companies might be better labeled as “barely viable” than “high-yield”.

China

Several items regarding relations between the US and China have emerged over the last couple of weeks and none of them good. Signal, a newsletter by GZero Media, chronicled several of these including, “US jabs over Hong Kong”, “Action on forced labor in Xinjiang”, “US strikes China’s Belt and Road project”, “US ban on China’s TikTok and WeChat”, “New tensions over Taiwan”, and “China flashes a trade weapon”.

While it is interesting that tensions seem to be percolating just ahead of the presidential election, it is perhaps most interesting that this is also the time that Terry Branstad, US Ambassador to China, decided to step down. As Luke Gromen noted in his Tree Rings newsletter (September 18, 2020), this action is potentially a sign of “turbulence incoming”. I agree; this seems like more than just coincidence.

Currencies

One of the hotter topics through the summer months was the weakness of the US dollar (USD). The narrative was that with unrestrained money printing and an exploding budget deficit, there was no direction for USD to go but down.

While there are clearly flaws to this portrayal, the weakening USD serves other purposes. For one, the weaker USD provides some relief to emerging markets that are suffering a double whammy of weak economic growth and weak currencies. The weaker USD also (ostensibly) provides incremental incentive for foreign entities to purchase US Treasuries which are expensive when the dollar is strong. Finally, USD also serves as a risk indicator. When volatility is high, investors flock to USD. Therefore, a weak USD signals relative tranquility in the investment landscape.

The big question is, what now? Did a weakening USD simply buy some time before things get shaken up again? Or is the recent uptick simply a short-term deviation from a broader downward trend? While I certainly don’t want to get into the game of short-term currency trading, I think the most likely scenario in the intermediate term is that USD will bounce back and that will prove extremely inconvenient for many foreign entities.

Coronavirus

US Suffers Most New COVID-19 Cases In 5 Weeks As Doctors Warn Of “Apocalyptic” Fall: Live Updates

“With many schools planning to end their semesters at the November holiday, students will disperse across the country, and some will bring the disease with them.”

“’This is beyond our wildest nightmares,’ said Gavin Yamey, a physician who directs Duke University’s Center for Policy Impact in Global Health.”

In the 8/21/20 edition of Observations I pointed out the special challenge that students returning to college presented to the effort to control the spread of the coronavirus. The facts that “campuses make an excellent breeding ground for the virus” and that many high-risk geographies were also allowing the resumption of football games seemed to create a lot of potential for increased infections.

In hindsight, this was absolutely right. Colleges and universities have been experiencing substantial outbreaks of coronavirus infections. One takeaway is that whatever measures were put into place ahead of time were not nearly enough. It didn’t have to be this way, but it was. Experience has proven that people still are not taking the threat of coronavirus seriously enough and political leaders, in general, have not been able to formulate cohesive or effective policies. Until those things change, there is no reason to expect different results.

Another takeaway is that with fall flu season right on the threshold, there is a fairly high risk of a significant second wave of infections, and one that could easily be worse than the first wave. Indeed, this is now my base expectation and one that does not seem to be getting serious consideration elsewhere. Unfortunately, there is a good chance that this will happen just as turbulence around the election develops and the economic impact of lost unemployment benefits start hitting home.

Politics

The Welding Shut of the American Mind

“Freedom of the mind requires not only, or not even specially, the absence of legal constraints but the presence of alternative thoughts. The most successful tyranny is not the one that uses force to assure uniformity but the one that removes the awareness of other possibilities.”

“Yet if a student can – and this is most difficult and unusual – draw back, get a critical distance on what he clings to, come to doubt the ultimate value of what he loves, he has taken the first and most difficult step toward the philosophic conversion.”

This note from Ben Hunt at Epsilon Theory features a couple of quotes from Allan Bloom in his book, “The Closing of the American Mind”. Like many notes from Hunt, it can be challenging to read. Also, like other notes from Hunt, it reveals some of the most important dynamics occurring in society and politics today. If you have not reviewed the content at Epsilon Theory, I would strongly recommend doing so. The work there is invaluable for making sense of today’s crazy world.

This particular note, in one sense, speaks to the development of extreme partisanship. It is about more than partisanship, though. The note describes the process whereby minds eventually close to new and different ideas. These are important issues at about every level and remind me of Jonathan Haidt’s book, “The Righteous Mind”.

These ideas resonate with me for a couple of reasons. For one, the work consistently identifies the implications of a polarized political landscape to our roles as both investors and as citizens. In addition, the work consistently informs those of us who prefer to “seek the truth” rather than to embrace convenient narratives. Good stuff.

Inflation

The Solid Ground report by Russell Napier, 23rd July, 2020

“Savers must be in no doubt that the aim of MMT [Modern Monetary Theory] is to redistribute wealth in an economy without full democratic endorsement and, crucially, in an arbitrary form.”

“Her [Stephanie Kelton’s] goals can be met without resort to MMT but that would require overt political endorsement for a much more active fiscal policy …”

MMT has been making the rounds as a proposal to deal with excessive levels of debt. I haven’t discussed it much because I consider it to be an intellectually vacuous effort and one unworthy of serious consideration. Russell Napier’s scathing review of MMT and clinical dissection of its flaws corroborates that position.

That said, MMT is getting a lot of attention in the press and in policy circles. Napier’s analysis reveals a couple of elements of the theory that are relevant for investors. One is that the core policy aim is to “redistribute wealth … without full democratic endorsement”. The other is that this desperate measure is only being resorted to because of the lack of support for “overt political endorsement”. These are neither the makings of a benign investment environment nor a healthy democracy.

Implications for investment strategy

This creates a risk and an opportunity for long-term investors. The risk, of course, is getting sucked into a game of trying to make short-term profits at the expense of taking great risks. The opportunity is to step back, recognize, and prepare for a couple of big changes that are coming.

One of those changes will be with public policy. Sooner or later inflation will come and shortly after it, financial repression. These measures will make investing extremely challenging. Further, there will be very little warning; nothing will be officially announced. Napier’s warning that “there is something much more concerning – a complete refusal to discuss what impact MMT will have on savers,” is apt: These polices will arrive as Trojan horses. They will come quietly, through the back door, with nothing to suggest their risk. Investors need to get prepared – now.

I believe another change will involve cultural innovation in the field of investment services. Most services are predicated on incremental quantitative measures – slightly better performance or slightly less risk. All of these are fine when risk assets keep going up.

When the going gets a lot tougher for financial assets, however, reaching for slightly higher returns becomes a much less valuable service. In its stead, qualitative goals such as preserving one’s wealth and managing risk take on a whole new meaning. Above all else, trustworthiness will be crucial. These changes are coming – maybe not today, and maybe not this year, but well within the investment horizon of long-term investors.

Principles for Areté’s Observations

- All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

- One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

- One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

- Because most investment theses tend to be one-sided, it can be difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, Areté’s Takes are designed to show both sides of an argument and to express my opinion as to which side has the stronger case, and why.

- With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

Please direct comments or feedback to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization’s particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read