On Monday, shares of Apple surged on a report Google could pay Apple roughly $15 billion this year to retain its place as the default search option on iOS, according to Bernstein analyst Toni Sacconaghi. That’s up from an estimated $10 billion in 2020.

Sacconaghi posits that the deal with Google will boost Apple’s services revenue growth by 8.5 percentage points — and account for as much as 9% of the iPhone maker’s gross profits in fiscal 2021.

Of course, it is hard to suggest such isn’t already priced into the shares. Yesterday, Apple’s valuation surpassed $2.5 Trillion. To put this into context, Apple’s valuation is now roughly 10% of the entire U.S. economy.

Click HERE to receive our daily market commentary in your email every morning.

What To Watch Today

Economy

- 9:00 a.m. ET: FHFA Home Price index, month-over-month, June (1.9% expected, 1.7% in May)

- 9:00 a.m. ET: S&P CoreLogic Case-Shiller 20-City index, month-over-month, June (1.80% expected, 1.81% in May)

- 9:00 a.m. ET: S&P CoreLogic Case-Shiller 20-City index, year-over-year, June (18.60% expected, 16.99% in May)

- 9:45 a.m. ET: MNI Chicago PMI, August (68.0 expected, 73.4 in July)

- 10:00 a.m. ET: Conference Board Consumer Confidence, August (123.0 expected, 129.1 in July)

Earnings

- 4:05 p.m. ET: Crowdstrike (CRWD) is expected to report adjusted earnings of 8 cents per share on revenue of $322.78 million

Politics

- President Biden will address the nation at 1:30 p.m. ET on the end of the war in Afghanistan. Biden says he’ll look back at evacuating over 120,000 people and his “decision not to extend our presence.”

- The Social Security and Medicare Trustees is scheduled to release its annual report. The report — the first to take the COVID-19 pandemic into account — should give a window into how soon the programs will face insolvency.

Now, August Is A Great Month For Stocks

“When August began, investors were warned that history has not been kind to the stock market during the summer’s final full month.

This is an annual tradition in markets commentary.

Over the last 10- and 20-year periods, the S&P 500 Index’s (^GSPC) average return during August has been negative — a distinction only matched by September’s similarly poor performance. And in years that follow a presidential election, only February has been less kind to investors.

And with concerns that include the Federal Reserve tapering its asset purchase program, the spread of the Delta variant and worries over expired unemployment insurance benefits, August 2021 seemed full of potential pitfalls for markets.

Almost none of which have been borne out.

With the S&P 500 closing at a record on Monday, the benchmark index has now made 13 record highs this month. Any advance on Tuesday will mark yet another record for the index. Through Monday’s close, the S&P 500 is up more than 3% so far this month, and on track for its best monthly gain since April.” – Yahoo

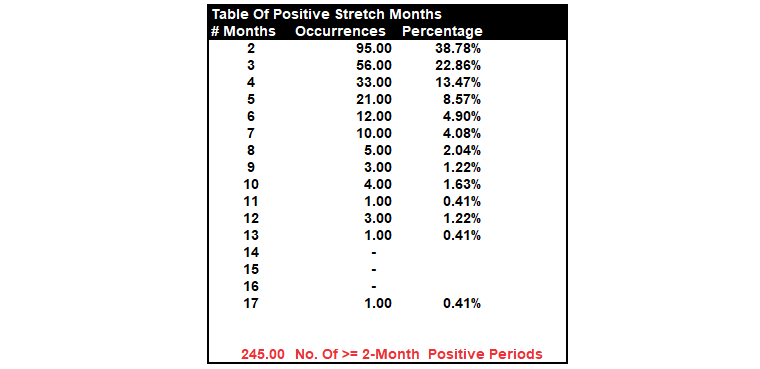

A Rare Occurrence

How often does the market have 7-postive months in a row? Not often. As we discussed recently, the table below shows all periods where there were 2-months or more of consecutive positive returns.

The table shows that nearly 40% of the time, two months of positive performance gets followed by at least one month of negative performance. Conversely, three consecutive positive months occur 23% of the time, and only 14% of occurrences stretch to 4-months.

Since 1871, there have only been 12-occurrences of 6-month or greater stretches of positive returns before a negative month appeared. In total, there are just 40 occurrences; out of 245 periods of 2-months or more, the market ran 6-months or longer without a correction.

However, the run ended in at least a negative return month in every period, but the vast majority ended with much deeper corrections.

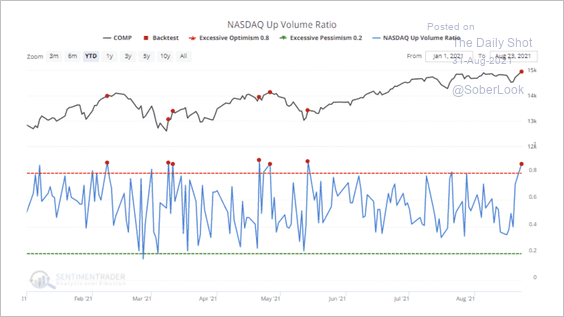

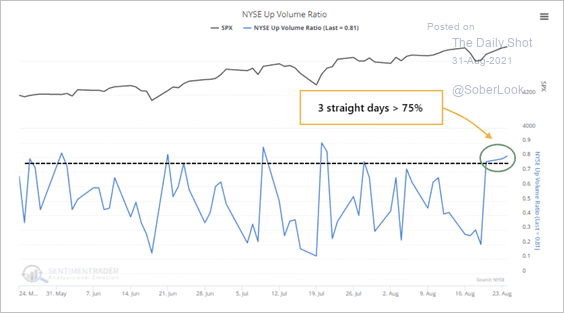

Internals Remain Very Weak

Sentiment Trader had a couple of interesting points on market internals yesterday.

Currently, more than 87% of the volume on the Nasdaq exchange flowed into advancing stocks, which typically precedes a pullback two weeks later.

And more than 75% of volume on the NYSE flowed into advancing stocks for three straight days last week.

More Divergence

In the aftermath of Powell’s speech last Friday, investors are clearly favoring Apple and other large-cap growth stocks. The S&P and NASDAQ closed up by .44% and 1.13% respectively, while the Dow is slightly lower and Russell 2000 off by .50%. Given Powell’s dovish tone, we suspected cyclical sectors and small caps would trade better. Market breadth remains poor as the generals are leading the way higher. Apple is up 3% and Facebook and Amazon are up over 2%. There were more declining stocks on the NYSE than advancers.

Atlanta Fed-GDP Now

The Atlanta Fed revised its GDP-Now forecast from 5.7% to 5.1% in large part due to slowing personal consumption. The Delta variant is resulting in weaker dining and hotel spending but that is not the only problem. The recent torrid pace of spending is unsustainable and normalization is inevitable. The economic headwinds in addition to Delta, in our opinion, are as follows:

- Pent-up demand is fading quickly

- Inflation concerns are dampening consumption

- Stimulus is running out quickly.

- Weakening consumer confidence

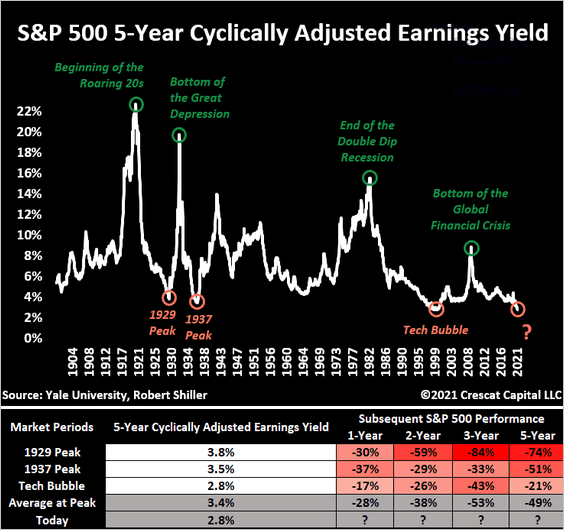

First Signs of Market Correction

Earnings Yield Warning

The graph below from Tavi Costa, charts the ratio of earnings over price. As he shows, investors are paying quite a premium for earnings. Most likely in the future, either earnings grow sharply or prices correct. As Tavi shows, the last four instances with similar yields were not market-friendly. Maybe this time will be different?

Watching The Paint Dry

Normally those Wall Street traders not sunning in the Hamptons watch the paint dry in trading rooms during the week preceding labor day. With the Fed providing more clarity on taper, that should be the case this year as well. However, the ADP and BLS employment reports come out Wednesday and Friday respectively. Given many Fed speakers are making it clear continued improvement in employment is the key to start tapering, we might see some fireworks this week. After a relatively weak report last month, ADP is expected to rise from 330k to 500k. Economists expect the BLS to show 650k more jobs in the workforce. With many unemployed people losing federal and state unemployment benefits, the incentive to find a job is higher which may lead to larger than expected additions to the workforce.

Also of interest this week will be the reaction of Fed speakers to Powell’s vague comments involving a taper timetable. We suspect dissension in the ranks will become more vocal over the coming weeks.

Also Read